filmov

tv

Derivation Of the Black-Scholes Equation (SDE)

Показать описание

This video is part of the Quantitative Finance series.

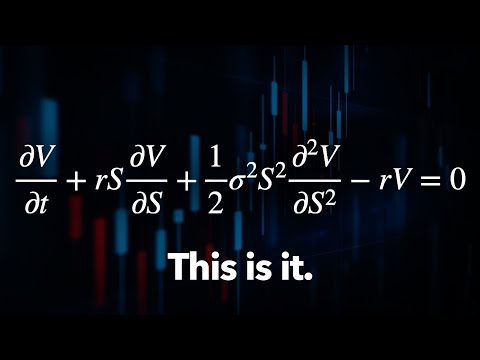

The Black-Scholes model is one of the most basic models in derivative pricing in quantitative finance. There are a few ways to derive the Black-Scholes SDE. Here I'm following the original Black-Scholes argument and describe one derivation with portfolio replication.

The Black-Scholes model is one of the most basic models in derivative pricing in quantitative finance. There are a few ways to derive the Black-Scholes SDE. Here I'm following the original Black-Scholes argument and describe one derivation with portfolio replication.

0:09:53

0:09:53

The Easiest Way to Derive the Black-Scholes Model

0:10:24

0:10:24

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

0:15:04

0:15:04

Derivation of the Black-Scholes equation

0:27:31

0:27:31

A simple derivation of the Black-Scholes equation

0:04:30

0:04:30

Black-Scholes PDE Derivation in 4 minutes

0:31:22

0:31:22

The Trillion Dollar Equation

0:15:54

0:15:54

Warren Buffett: Black-Scholes Formula Is Total Nonsense

0:00:12

0:00:12

Derivation of Black-Scholes Equation |FULL|

0:14:03

0:14:03

Black Scholes Explained - A Mathematical Breakdown

0:13:34

0:13:34

Deriving the Black Scholes Call Formula

0:17:24

0:17:24

Deriving Black Scholes

0:03:40

0:03:40

Black Scholes Formula explained simply

0:16:55

0:16:55

Black Scholes Derivation

0:49:52

0:49:52

19. Black-Scholes Formula, Risk-neutral Valuation

0:03:24

0:03:24

Derivation Of the Black-Scholes Equation (SDE)

0:30:15

0:30:15

The Math of 'The Trillion Dollar Equation'

0:07:40

0:07:40

Black-Scholes Equation from Ito's Lemma

0:05:59

0:05:59

Black-Scholes Equation (Financial Engineering)

0:10:41

0:10:41

Deriving the Black-Scholes Pricing Equation

0:11:33

0:11:33

Black Scholes Option Pricing Model and Ito Calculus: The Concepts Behind the Equation

0:00:59

0:00:59

Mastering the Black-Scholes Model: Essential Knowledge for Options Traders

0:03:58

0:03:58

Derivation of the Black-Scholes PDE

0:10:40

0:10:40

The Black-Scholes Model EXPLAINED

0:00:12

0:00:12

Deriving Black-Scholes Theorem on Live

Комментарии