filmov

tv

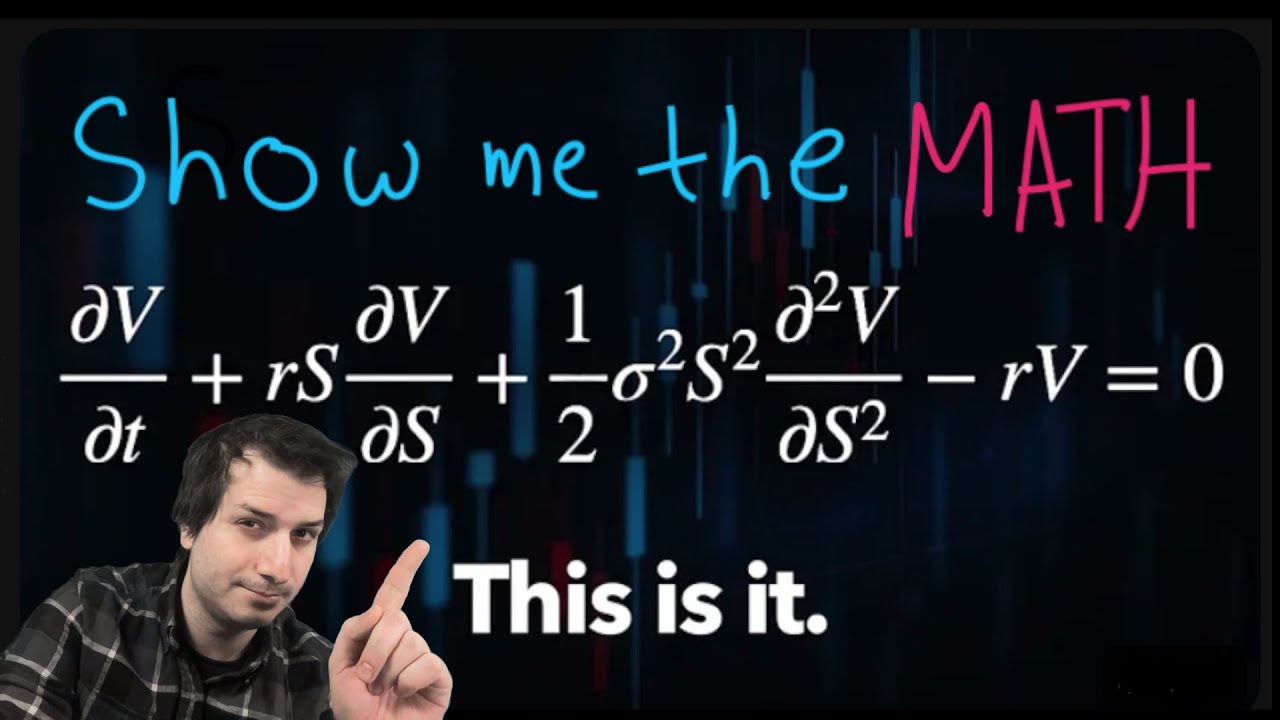

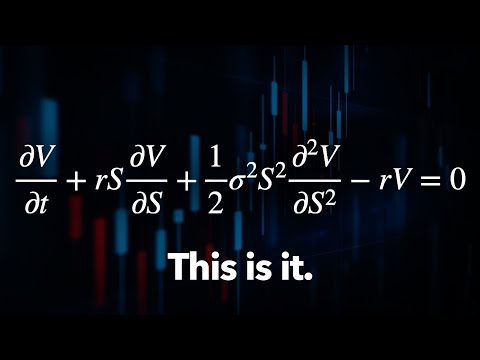

The Math of 'The Trillion Dollar Equation'

Показать описание

Here are my notes from I was a PhD student on this stuff (we were allowed to bring in short notes to the exam)

0:00 The Trillion Dollar Equation

0:18 Veritasium's Example of the Call Option

2:13 The function v(s t) for the value of the option

3:29 Veritasium's Delta hedged portfolio

4:19 Veritasium's slide by derivation

5:24 Derivation of the Black-Scholes equation from scratch

8:26 Change in portfolio value d Pi t

9:47 Approximate changes by derivatives of v a la Taylor series

15:08 Model for the stock price S t Geometric Brownian Motion

19:42 d S t squared is just a dt a la Itos Lemma

25:44 Set delta to di v di s to perfectly hedge

27:23 Equate to the risk free interest rate equation

29:10 But isnt delta a function of time? Why does this work?

0:31:22

0:31:22

The Trillion Dollar Equation

0:30:15

0:30:15

The Math of 'The Trillion Dollar Equation'

0:07:55

0:07:55

The Trillion Dollar FLAW in Financial Market Trading

0:06:41

0:06:41

The Trillion dollar mathematical equation.

0:01:01

0:01:01

man vs machine: 1 TRILLION math problems

0:01:12

0:01:12

Million, Billion, Trillion, Lakhs, Crores?😕 - Part 1 | Fun Math | Don't Memorise

0:22:09

0:22:09

The Simplest Math Problem No One Can Solve - Collatz Conjecture

0:00:39

0:00:39

👉 Million / Billion / Trillion / Arab / Kharab / Nil 🤔 !! #maths #kharab #arab #million #shorts...

0:00:15

0:00:15

Million, Billion, Trillion

0:00:24

0:00:24

One Trillion Dollars (In Seconds) Interesting Math & Money Breakdown

0:00:33

0:00:33

Meaning of Million, Billion,Trillion | Number System #shorts #maths #million #trillion #numbers

0:00:10

0:00:10

#million #billion #trillion #quadrillion#maths#important

0:00:40

0:00:40

Hey siri what’s 1 Trillion to the 10th power…💀#viral #shorts

0:00:05

0:00:05

million billion trillion conversion of number

0:00:23

0:00:23

Compounding example_ $1 in 1776 to over $5 trillion in 2021 #shorts #maths #trillion

0:09:52

0:09:52

1 Million Vs 1 Billion Vs 1 Trillion Vs 1 Quadrillion | What is a Centillion? | Epic Powers of 10

0:00:49

0:00:49

#shorts 😎How Many Zeros Are in All Numbers, Million, Billion, Trillion, Sextillion? #mathematics

0:00:57

0:00:57

Exploring Big Numbers like Billion, Trillion, Decilion. #billion #trillion #googol #math #maths

0:01:56

0:01:56

Doubles Addition Facts Song

0:00:22

0:00:22

NumberBlock from ONE to TRILLION FAST! #shorts #numberblocks #minecraft #trillion #fast

0:00:28

0:00:28

How Many Zero Are In a Trillion!#maths #youtubeshorts #shortsvideo #ytshorts #yt #mathsfact #youtube

0:05:29

0:05:29

What if you had a Trillion Dollars? + more videos | #aumsum #kids #science #education #children

0:00:05

0:00:05

Meaning of Million, Billion, Trillion #shorts #counting

0:00:08

0:00:08

Million Billion Trillion quadrillion... #mathstricks #shorts #basicmaths

Комментарии