filmov

tv

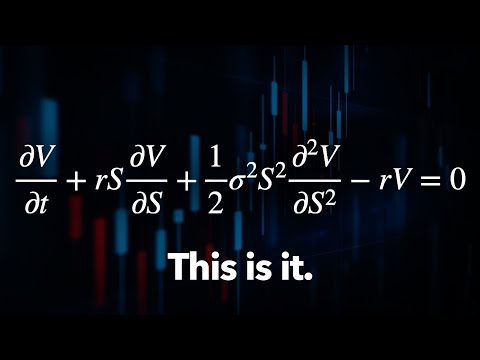

Black-Scholes Equation (Financial Engineering)

Показать описание

Hello everyone, this is a revision video of how to derive the Black-Scholes Equation ( a partial differential equation) for option pricing. Please let me know in the comments session any topics in financial Engineering you will like me to create. Also don’t forget to like, comment and subscribe if you are new to my channel. Please remember to click the post notification bell so you don’t miss any videos from me. Thank you very much.

0:31:22

0:31:22

The Trillion Dollar Equation

0:05:59

0:05:59

Black-Scholes Equation (Financial Engineering)

0:49:52

0:49:52

19. Black-Scholes Formula, Risk-neutral Valuation

0:08:29

0:08:29

Is the Black Scholes Actually Used in the Real World

1:20:29

1:20:29

20. Option Price and Probability Duality

0:23:15

0:23:15

Black Scholes Proof

0:23:04

0:23:04

Black Scholes Proof

1:23:38

1:23:38

Mathematical Finance L 11: Convergence to the Black-Scholes formula

0:02:44

0:02:44

Pricing Options with Mathematical Models | CaltechX on edX | Course About Video

0:07:01

0:07:01

Itos Lemma Explained

0:06:22

0:06:22

Black Scholes for Call Options

0:05:00

0:05:00

Financial Modeling: Black Scholes Model

0:07:13

0:07:13

Brownian Motion / Wiener Process Explained

0:19:02

0:19:02

Black Scholes Analysis for dummies - Understanding Nd2

0:03:24

0:03:24

Derivation Of the Black-Scholes Equation (SDE)

0:43:28

0:43:28

The Black–Scholes/Merton Derivatives Symposium: 46 Years and Counting: Real Options

1:11:24

1:11:24

Black Scholes PDEs in Computational Finance -Dr. Natesan Srinivasan

0:06:52

0:06:52

Heat Equation & The Black Scholes Model

0:15:55

0:15:55

Black-Scholes Option Pricing (How to Lead the Formula - Revealed)

0:20:29

0:20:29

Financial Engineering for EVERYONE! (Patreon Request) - Stefanica

0:05:37

0:05:37

What are the deficiencies of the Black-Scholes model? Why is the BS model still used?

0:08:58

0:08:58

Paul Wilmott on Quantitative Finance, Chapter 8, Black-Scholes with Borrowing

0:06:35

0:06:35

Black-Scholes Model: Merton Jump-Diffusion Call Option Pricing Formula and Implementation

0:00:56

0:00:56

Jeff Bezos Quit Being A Physicist

Комментарии