filmov

tv

19. Black-Scholes Formula, Risk-neutral Valuation

Показать описание

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013

Instructor: Vasily Strela

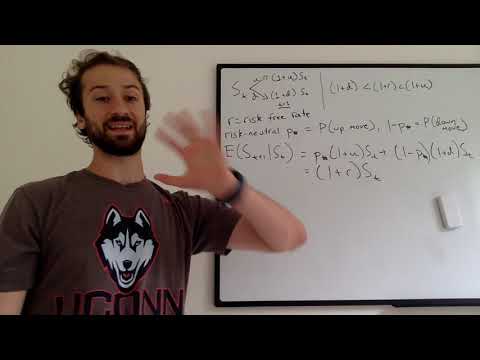

This is a lecture on risk-neutral pricing, featuring the Black-Scholes formula and risk-neutral valuation.

License: Creative Commons BY-NC-SA

Instructor: Vasily Strela

This is a lecture on risk-neutral pricing, featuring the Black-Scholes formula and risk-neutral valuation.

License: Creative Commons BY-NC-SA

0:49:52

0:49:52

19. Black-Scholes Formula, Risk-neutral Valuation

0:10:24

0:10:24

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

0:16:35

0:16:35

6 4 Risk neutral pricing Black Scholes Merton model Part 1

0:15:54

0:15:54

Warren Buffett: Black-Scholes Formula Is Total Nonsense

0:10:12

0:10:12

Risk neutral probability measure simplified

0:24:44

0:24:44

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

0:09:53

0:09:53

The Easiest Way to Derive the Black-Scholes Model

0:00:52

0:00:52

Risk Neutral Valuation

0:02:58

0:02:58

Black-Scholes Model of Option Pricing Explained - NY Institute of Finance

0:18:12

0:18:12

Black Scholes Formula Risk Neutral Derivation

0:09:23

0:09:23

Black Scholes Option Pricing Model Explained In Excel

0:05:52

0:05:52

The Black-Scholes Formula Explained

0:32:33

0:32:33

Black Scholes Formula I

0:00:59

0:00:59

Mastering the Black-Scholes Model: Essential Knowledge for Options Traders

0:14:12

0:14:12

How to interpret N(d1) and N(d2) in Black Scholes Merton (FRM T4-12)

0:22:23

0:22:23

4 2 Risk neutral pricing Part 1

0:07:46

0:07:46

Dynamics of Black Scholes’ Stock Price under the Risk Neutral and Stock Measure (Numeraire)

0:07:45

0:07:45

Pricing a Call Option using a Risk Neutral Tree Measure.

0:03:40

0:03:40

Black Scholes Formula explained simply

0:10:40

0:10:40

The Black-Scholes Model EXPLAINED

0:08:34

0:08:34

5. Risk Neutral Probability

0:11:19

0:11:19

Risk Neutral Valuation under Black-Scholes

1:20:34

1:20:34

Lecture 15 (Part 1) - Understanding Black Scholes using Risk Neutral Method (CA; CFA L2 and FRM P1)

0:09:51

0:09:51

Pricing Options Using the Binomial Tree (Risk Neutral Valuation Approach)

Комментарии