filmov

tv

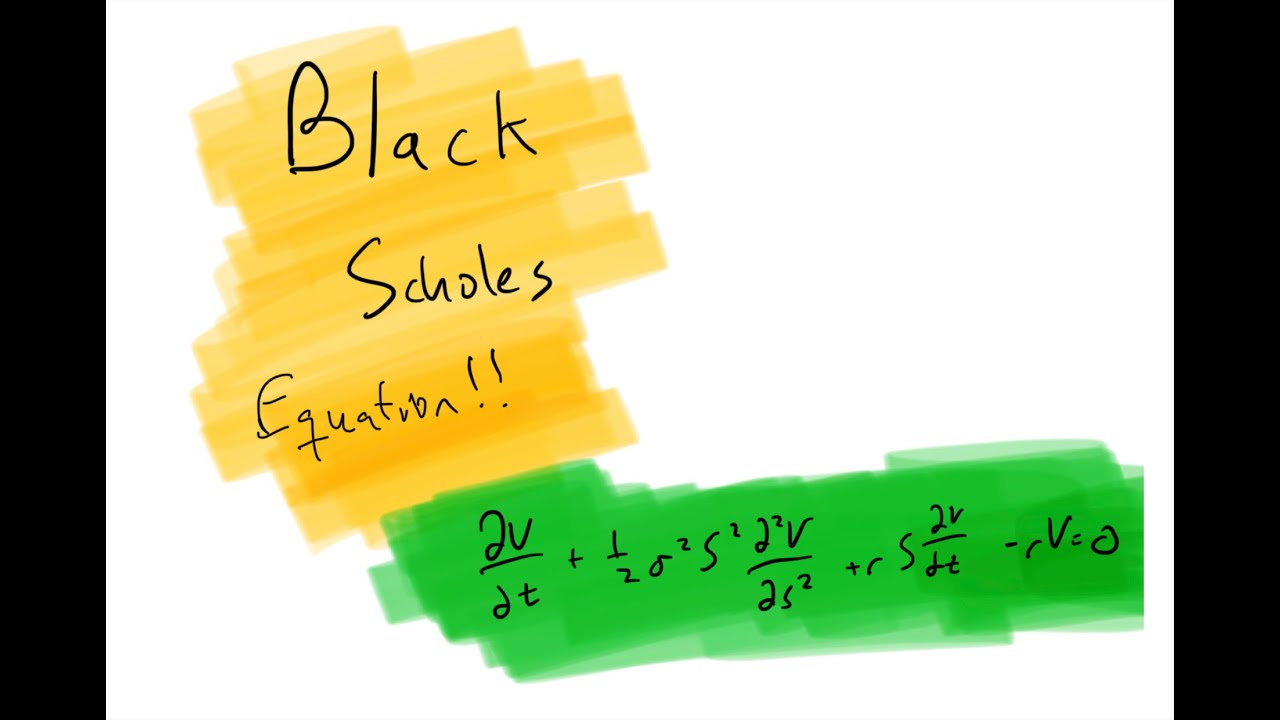

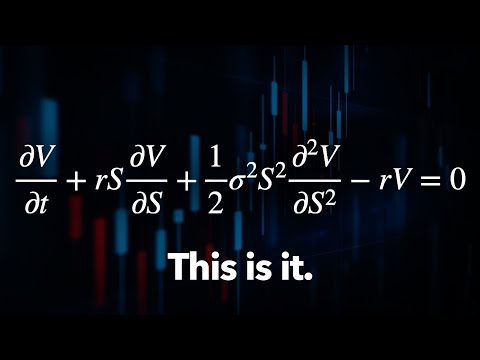

Deriving Black Scholes

Показать описание

In this video, we derive the famous Black-Scholes Equation, the basis of all option pricing. I tried not to skip any steps, and tried to explain everything I was doing, so the derivation ought to be easy to follow. Let me know if I failed!

For this video, we need to know Ito's Lemma, and we need to work with Geometric Brownian motion, so it is highly advised that you go through those videos first!

Ito's Lemma:

Geometric Brownian Motion:

If you learn something, please click the Like button.

If you want to keep learning, go ahead an subscribe!

For this video, we need to know Ito's Lemma, and we need to work with Geometric Brownian motion, so it is highly advised that you go through those videos first!

Ito's Lemma:

Geometric Brownian Motion:

If you learn something, please click the Like button.

If you want to keep learning, go ahead an subscribe!

0:09:53

0:09:53

The Easiest Way to Derive the Black-Scholes Model

0:10:24

0:10:24

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

0:04:30

0:04:30

Black-Scholes PDE Derivation in 4 minutes

0:17:24

0:17:24

Deriving Black Scholes

0:15:04

0:15:04

Derivation of the Black-Scholes equation

0:16:55

0:16:55

Black Scholes Derivation

0:15:54

0:15:54

Warren Buffett: Black-Scholes Formula Is Total Nonsense

0:27:31

0:27:31

A simple derivation of the Black-Scholes equation

0:13:34

0:13:34

Deriving the Black Scholes Call Formula

0:10:41

0:10:41

Deriving the Black-Scholes Pricing Equation

0:49:52

0:49:52

19. Black-Scholes Formula, Risk-neutral Valuation

0:00:12

0:00:12

Derivation of Black-Scholes Equation |FULL|

0:31:22

0:31:22

The Trillion Dollar Equation

0:03:40

0:03:40

Black Scholes Formula explained simply

0:00:12

0:00:12

Deriving Black-Scholes Theorem on Live

0:14:03

0:14:03

Black Scholes Explained - A Mathematical Breakdown

0:21:06

0:21:06

Deriving Black-Scholes Using Ito's Lemma

0:05:59

0:05:59

Black-Scholes Equation (Financial Engineering)

0:00:39

0:00:39

Charlie Munger on Black–Scholes

0:05:44

0:05:44

Measure change approach to the derivation of Black Scholes

0:00:59

0:00:59

Unlocking the Black-Scholes Model: Visualizing the Power of Options Trading in 60 Seconds

0:30:15

0:30:15

The Math of 'The Trillion Dollar Equation'

0:03:58

0:03:58

Derivation of the Black-Scholes PDE

0:05:48

0:05:48

An intuitive explanation the Black Scholes' formula

Комментарии