filmov

tv

Deriving the Black-Scholes Pricing Equation

Показать описание

This video is part of my series on the Black-Scholes model.

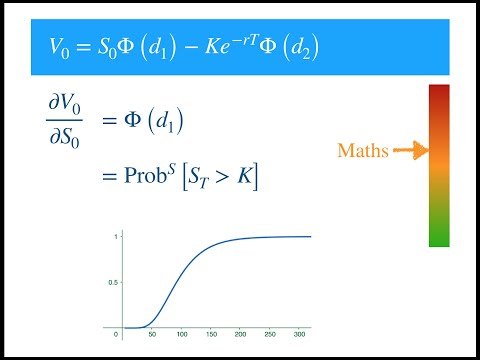

Disclaimer: I do not know, why we use the normal pdf - shouldn't we use the lognormal pdf as the random variable is lognormal? If anybody knows, please leave me a comment.

Disclaimer: I do not know, why we use the normal pdf - shouldn't we use the lognormal pdf as the random variable is lognormal? If anybody knows, please leave me a comment.

0:10:24

0:10:24

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

0:10:41

0:10:41

Deriving the Black-Scholes Pricing Equation

0:09:53

0:09:53

The Easiest Way to Derive the Black-Scholes Model

0:15:54

0:15:54

Warren Buffett: Black-Scholes Formula Is Total Nonsense

0:13:34

0:13:34

Deriving the Black Scholes Call Formula

0:04:30

0:04:30

Black-Scholes PDE Derivation in 4 minutes

0:14:03

0:14:03

Black Scholes Explained - A Mathematical Breakdown

0:00:12

0:00:12

Derivation of Black-Scholes Equation |FULL|

0:49:52

0:49:52

19. Black-Scholes Formula, Risk-neutral Valuation

0:03:40

0:03:40

Black Scholes Formula explained simply

0:05:44

0:05:44

Measure change approach to the derivation of Black Scholes

0:17:24

0:17:24

Deriving Black Scholes

0:00:12

0:00:12

Deriving Black-Scholes Theorem on Live

0:15:04

0:15:04

Derivation of the Black-Scholes equation

0:16:55

0:16:55

Black Scholes Derivation

0:00:39

0:00:39

Charlie Munger on Black–Scholes

0:00:59

0:00:59

Unlocking the Black-Scholes Model: Visualizing the Power of Options Trading in 60 Seconds

0:05:48

0:05:48

An intuitive explanation the Black Scholes' formula

0:09:23

0:09:23

Black Scholes Option Pricing Model Explained In Excel

0:08:33

0:08:33

Gamma of Black Scholes Price: Derivation and Intuitive Explanation

0:00:59

0:00:59

Mastering the Black-Scholes Model: Essential Knowledge for Options Traders

0:11:38

0:11:38

Delta of Black Scholes Price: Derivation and Intuitive Explanation

0:40:22

0:40:22

Options Pricing Full Derivation (European call and put using Black Scholes formula)

0:03:24

0:03:24

Derivation Of the Black-Scholes Equation (SDE)

Комментарии