filmov

tv

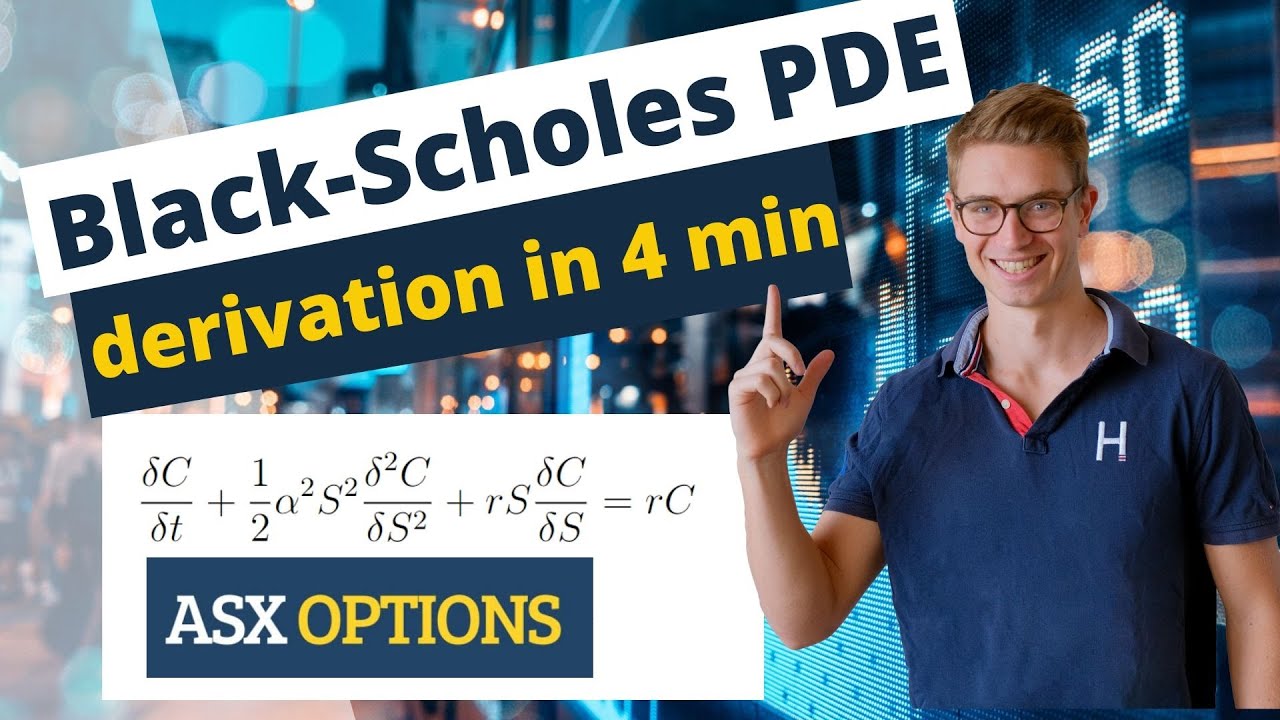

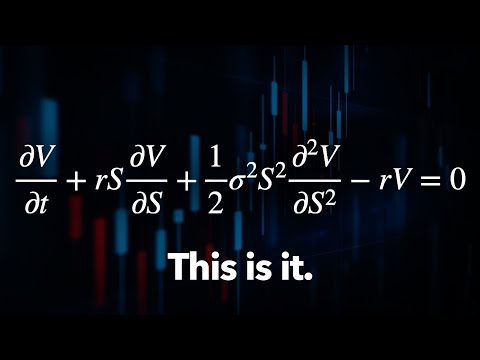

Black-Scholes PDE Derivation in 4 minutes

Показать описание

In this video we derive the famous Black-Scholes Partial Differential Equation from scratch! There will be several videos following this tutorial, to break down some financial concepts in more depth.

★ ★ QuantPy GitHub ★ ★

★ ★ Discord Community ★ ★

★ ★ Support our Patreon Community ★ ★

Get access to Jupyter Notebooks that can run in the browser without downloading python.

★ ★ ThetaData API ★ ★

ThetaData's API provides both realtime and historical options data for end-of-day, and intraday trades and quotes. Use coupon 'QPY1' to receive 20% off on your first month.

★ ★ Online Quant Tutorials ★ ★

★ ★ Contact Us ★ ★

Disclaimer: All ideas, opinions, recommendations and/or forecasts, expressed or implied in this content, are for informational and educational purposes only and should not be construed as financial product advice or an inducement or instruction to invest, trade, and/or speculate in the markets. Any action or refraining from action; investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied in this content, are committed at your own risk an consequence, financial or otherwise. As an affiliate of ThetaData, QuantPy Pty Ltd is compensated for any purchases made through the link provided in this description.

★ ★ QuantPy GitHub ★ ★

★ ★ Discord Community ★ ★

★ ★ Support our Patreon Community ★ ★

Get access to Jupyter Notebooks that can run in the browser without downloading python.

★ ★ ThetaData API ★ ★

ThetaData's API provides both realtime and historical options data for end-of-day, and intraday trades and quotes. Use coupon 'QPY1' to receive 20% off on your first month.

★ ★ Online Quant Tutorials ★ ★

★ ★ Contact Us ★ ★

Disclaimer: All ideas, opinions, recommendations and/or forecasts, expressed or implied in this content, are for informational and educational purposes only and should not be construed as financial product advice or an inducement or instruction to invest, trade, and/or speculate in the markets. Any action or refraining from action; investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied in this content, are committed at your own risk an consequence, financial or otherwise. As an affiliate of ThetaData, QuantPy Pty Ltd is compensated for any purchases made through the link provided in this description.

0:04:30

0:04:30

Black-Scholes PDE Derivation in 4 minutes

0:05:56

0:05:56

The Black Scholes PDE

0:09:53

0:09:53

The Easiest Way to Derive the Black-Scholes Model

0:12:45

0:12:45

Black Scholes PDE Derivation using Delta Hedging

0:03:58

0:03:58

Derivation of the Black-Scholes PDE

0:09:38

0:09:38

Transformation of Black Scholes PDE to Heat Equation

0:00:12

0:00:12

Derivation of Black-Scholes Equation |FULL|

0:05:07

0:05:07

The Black-Scholes Model

0:31:22

0:31:22

The Trillion Dollar Equation

0:30:15

0:30:15

The Math of 'The Trillion Dollar Equation'

0:10:24

0:10:24

Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

0:08:21

0:08:21

Black Scholes Derivation from Heat Equation/ Diffusion Equation v2

0:27:31

0:27:31

A simple derivation of the Black-Scholes equation

0:05:48

0:05:48

Introduction to Finite Difference Methods for Option Pricing

0:00:59

0:00:59

Mastering the Black-Scholes Model: Essential Knowledge for Options Traders

0:15:04

0:15:04

Derivation of the Black-Scholes equation

0:05:59

0:05:59

Black-Scholes Equation (Financial Engineering)

0:38:44

0:38:44

1. Black Scholes - Deriving the PDE

0:17:39

0:17:39

But what is a partial differential equation? | DE2

0:06:22

0:06:22

Black Scholes for Call Options

0:49:52

0:49:52

19. Black-Scholes Formula, Risk-neutral Valuation

2:10:01

2:10:01

Financial Option Theory with Mathematica -- Black/Scholes PDE and Heat Equation

0:34:59

0:34:59

Lecture 59: Path Integral Solution Of Black Scholes PDE

0:03:40

0:03:40

Black Scholes Formula explained simply

Комментарии