filmov

tv

Why Infinite Banking is Scam: The Honest Insurance Guy

Показать описание

"The Honest Insurance Guy" series was created simply to bring full information to the table and scrutinize some of the statements being put out there by insurance agents and financial professionals. Subscribe for more content, and more truth!

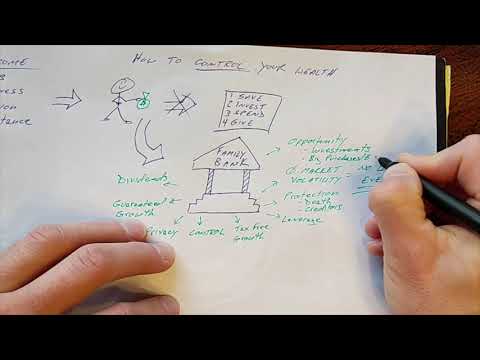

Infinite banking is essentially the act of putting your money into an insurance policy to "borrow" from the insurance company and create cash flow. This is a redundant step, this video is not intended to start beef nor drama but to bring full disclosure to what could be a poor mistake. That is I'm doing bringing full information to the table so we can make informed decisions. As an insurance producer myself I have full incentive to also practice this thing but a believer I truly feel that this is a half truth lie designed to have individuals buy unnecessary amount of insurance enriching many insurance agents and companies along the way.

Psalms 112: 5

Proverbs 12: 22

#wealthnation #infinitebanking #Insurance # LifeInsurance #Scam #daveramsey #daveramsey #debtfreecommunity #debtfreejourney #debtfree #budgeting #financialfreedom #budget #daveramseybabysteps #babystep #personalfinance #babysteps #financialpeace #debtfreeliving #debtisdumb #money #financialindependence #debtsnowball #debt #debtfreegoals #frugal #frugalliving #cashenvelopes #debtfreedom #cashisking #goals #savemoney #dfc #financialliteracy #finance #bhfyp #finance #business #money #investing #investment #entrepreneur #financialfreedom #wealth #success #stocks #trading #stockmarket #invest #bitcoin #motivation #forex #realestate #investor #accounting #cryptocurrency #covid #wallstreet #personalfinance #entrepreneurship #marketing #financialliteracy #smallbusiness #crypto #credit #bhfyp

Infinite banking is essentially the act of putting your money into an insurance policy to "borrow" from the insurance company and create cash flow. This is a redundant step, this video is not intended to start beef nor drama but to bring full disclosure to what could be a poor mistake. That is I'm doing bringing full information to the table so we can make informed decisions. As an insurance producer myself I have full incentive to also practice this thing but a believer I truly feel that this is a half truth lie designed to have individuals buy unnecessary amount of insurance enriching many insurance agents and companies along the way.

Psalms 112: 5

Proverbs 12: 22

#wealthnation #infinitebanking #Insurance # LifeInsurance #Scam #daveramsey #daveramsey #debtfreecommunity #debtfreejourney #debtfree #budgeting #financialfreedom #budget #daveramseybabysteps #babystep #personalfinance #babysteps #financialpeace #debtfreeliving #debtisdumb #money #financialindependence #debtsnowball #debt #debtfreegoals #frugal #frugalliving #cashenvelopes #debtfreedom #cashisking #goals #savemoney #dfc #financialliteracy #finance #bhfyp #finance #business #money #investing #investment #entrepreneur #financialfreedom #wealth #success #stocks #trading #stockmarket #invest #bitcoin #motivation #forex #realestate #investor #accounting #cryptocurrency #covid #wallstreet #personalfinance #entrepreneurship #marketing #financialliteracy #smallbusiness #crypto #credit #bhfyp

0:09:17

0:09:17

Why Infinite Banking is a SCAM!

0:05:26

0:05:26

The TRUTH About Infinite Banking! (Is It a Scam?)

0:20:18

0:20:18

Infinite Banking Is A Scam | Response To Dave Ramsey

0:38:20

0:38:20

Our Response To Dave Ramsey's 'Why Infinite Banking Is A Scam' | IBC Global

0:09:34

0:09:34

Heated Debate Between Infinite Banker and Dave Ramsey

0:05:36

0:05:36

Is Infinite Banking Really a Scam?

0:11:18

0:11:18

Why Infinite Banking is Scam: The Honest Insurance Guy

0:00:58

0:00:58

Why Infinite Banking Is A SCAM!

0:13:22

0:13:22

Is Infinite Banking a Scam?

0:27:02

0:27:02

Infinite Banking Concept Explained (Honest and Unbiased)

0:31:55

0:31:55

Insurance Companies Are Lying to You (Infinite Banking Exposed!)

0:40:28

0:40:28

How I lost $534,000 Through Infinite Banking - The Chris Naugle

0:13:29

0:13:29

WATCH OUT! INFINITE BANKING SCAM

0:04:55

0:04:55

Is Infinite Banking a SCAM? The Honest Truth From An Expert

0:03:53

0:03:53

Infinite Banking Scam

0:19:02

0:19:02

How The Mega Rich Invest | Infinite Banking Scam?

0:27:07

0:27:07

The 5 Biggest Negatives of Infinite Banking

0:13:04

0:13:04

The Infinite Banking Concept Episode 4 – Infinite Banking is a scam.

0:36:52

0:36:52

Why Infinite Banking is a SCAM! | Reaction to Dave Ramsey’s Video | Wealth Nation

0:06:45

0:06:45

The Infinite Banking Concept Explained

0:05:55

0:05:55

Why Most People Get Infinite Banking Wrong!

0:26:50

0:26:50

Dave Ramsey's HEATED Debate with Infinite Banker - My Response

1:06:09

1:06:09

Is Infinite Banking a SCAM? Dave Ramsey Says So

0:04:27

0:04:27

The Infinite Banking Concept explained

Комментарии