filmov

tv

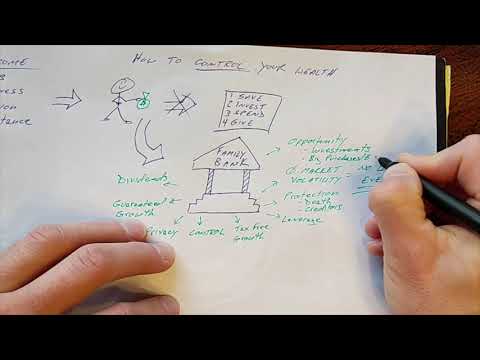

The TRUTH About Infinite Banking! (Is It a Scam?)

Показать описание

We know how infinite banking is pitched on social media: returns are guaranteed, there’s no risk, and you can access your money whenever you want. What is the TRUTH of infinite banking?

Bring confidence to your wealth building with simplified strategies from The Money Guy. Learn how to apply financial tactics that go beyond common sense and help you reach your money goals faster. Make your assets do the heavy lifting so you can quit worrying and start living a more fulfilled life.

Bring confidence to your wealth building with simplified strategies from The Money Guy. Learn how to apply financial tactics that go beyond common sense and help you reach your money goals faster. Make your assets do the heavy lifting so you can quit worrying and start living a more fulfilled life.

0:05:26

0:05:26

The TRUTH About Infinite Banking! (Is It a Scam?)

0:09:17

0:09:17

Why Infinite Banking is a SCAM!

0:04:27

0:04:27

The Infinite Banking Concept explained

0:27:02

0:27:02

Infinite Banking Concept Explained (Honest and Unbiased)

0:22:35

0:22:35

The Truth About Infinite Banking & Privatized Banking (What You Need To Know)

0:31:55

0:31:55

Insurance Companies Are Lying to You (Infinite Banking Exposed!)

0:18:13

0:18:13

The TRUTH About The Infinite Banking Concept EXPLAINED! | Wealth Nation

0:28:52

0:28:52

The TRUTH About The Infinite Banking Concept!

2:46:26

2:46:26

4 Ways to Level Up Your Money Game Using Infinite Banking

0:29:06

0:29:06

This Will Change Your Mind About Infinite Banking Concept

0:11:18

0:11:18

Why Infinite Banking is Scam: The Honest Insurance Guy

0:12:26

0:12:26

My Secrets - The Truth About the Infinite Banking System | Infinite Banking with Chris Naugle

0:51:29

0:51:29

The Truth About The Infinite Banking Concept

0:21:29

0:21:29

What Is Infinite Banking: The Truth About The Infinite Banking Concept

0:15:14

0:15:14

The Truth About Infinite Banking, Cash Flow Banking & Bank On Yourself (What You Need To Know)

0:09:34

0:09:34

Heated Debate Between Infinite Banker and Dave Ramsey

0:40:28

0:40:28

How I lost $534,000 Through Infinite Banking - The Chris Naugle

0:01:05

0:01:05

The TRUTH About The Infinite Banking Concept! Is IBC A Scam? (Canada)

0:27:07

0:27:07

The 5 Biggest Negatives of Infinite Banking

0:05:45

0:05:45

The Half-Truths Of Infinite Banking

0:20:18

0:20:18

Infinite Banking Is A Scam | Response To Dave Ramsey

0:13:43

0:13:43

The Good & Bad of The Infinite Banking Concept

0:03:51

0:03:51

The truth about infinite banking

0:44:52

0:44:52

What Is The Infinite Banking Concept? - Part 10: What Makes Infinite Banking INFINITE?

Комментарии