filmov

tv

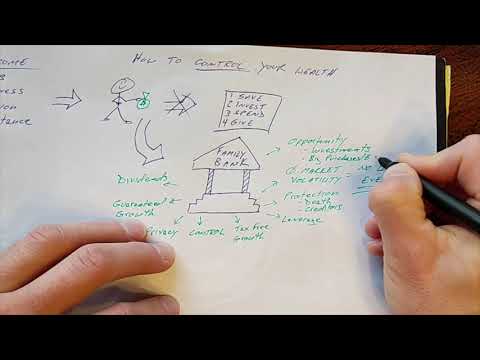

The Infinite Banking Concept Explained

Показать описание

What is infinite banking? It is often misunderstood and not easily comprehended. We’ll break down exactly what infinite banking is and how it works.

Bring confidence to your wealth building with simplified strategies from The Money Guy. Learn how to apply financial tactics that go beyond common sense and help you reach your money goals faster. Make your assets do the heavy lifting so you can quit worrying and start living a more fulfilled life.

Bring confidence to your wealth building with simplified strategies from The Money Guy. Learn how to apply financial tactics that go beyond common sense and help you reach your money goals faster. Make your assets do the heavy lifting so you can quit worrying and start living a more fulfilled life.

0:04:27

0:04:27

The Infinite Banking Concept explained

0:23:07

0:23:07

The Infinite Banking Concept EXPLAINED! And How To Get Started | Chris Naugle

0:06:45

0:06:45

The Infinite Banking Concept Explained

0:07:29

0:07:29

The Infinite Banking Concept Made Simple (with Illustrations)

0:21:22

0:21:22

The Infinite Banking System Explained (Full Breakdown!)

0:09:17

0:09:17

Why Infinite Banking is a SCAM!

0:27:02

0:27:02

Infinite Banking Concept Explained (Honest and Unbiased)

0:12:04

0:12:04

Infinite Banking Explained in 12 Minutes by a 'Recovering CPA'

0:59:26

0:59:26

Unlocking Financial Freedom: Expert Secrets from Michael Baker

1:02:06

1:02:06

This Is Nelson Nash: The Creator of The Infinite Banking Concept

0:05:38

0:05:38

Infinite Banking Concept: The Pros and Cons You Need to Know

0:09:09

0:09:09

The Infinite Banking Concept Explained (How to, Where to, When to) | Chris Naugle

0:05:15

0:05:15

What is the INFINITE BANKING Concept? #velocitybanking #IBC

2:22:21

2:22:21

Using The Infinite Banking Concept To Pay Off Debt, Buy Cars, & Plan For Retirement

0:19:23

0:19:23

How The Infinite Banking Concept Works

0:24:50

0:24:50

Infinite Banking Concept Explained

0:00:16

0:00:16

The Infinite Banking Concept, Explained

0:21:18

0:21:18

Infinite Banking Simplified | Explain the IBC To A 10 Year Old

0:19:55

0:19:55

The Infinite Banking Concept - Short Explanation

0:19:43

0:19:43

The Infinite Banking Concept - Short Explanation

0:12:50

0:12:50

Infinite Banking For Beginners | Wealth Nation

0:50:29

0:50:29

Using The Infinite Banking Concept To Pay Off Debt, Buy Cars, & Plan For Retirement

0:40:28

0:40:28

How I lost $534,000 Through Infinite Banking - The Chris Naugle

0:09:34

0:09:34

Heated Debate Between Infinite Banker and Dave Ramsey

Комментарии