filmov

tv

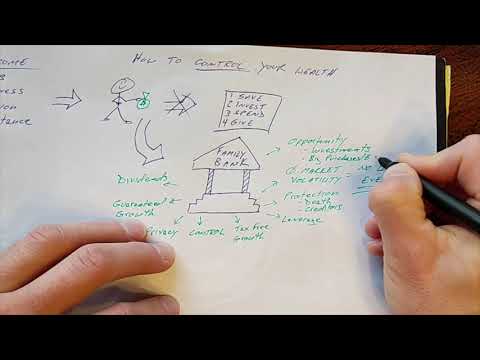

Infinite Banking Is A Scam | Response To Dave Ramsey

Показать описание

My response to Dave Ramsey calling whole life insurance and infinite banking a scam.

#lifeinsurance #daveramsey #infinitebanking

=================================

=========================

Caleb Guilliams

====================

*This video is for entertainment purposes only and is not financial or legal advice.

Financial Advice Disclaimer: All content on this channel is for education, discussion and illustrative purposes only and should not be construed as professional financial advice or recommendation. Should you need such advice, consult a licensed financial or tax advisor. No guarantee is given regarding the accuracy of information on this channel. Neither host or guests can be held responsible for any direct or incidental loss incurred by applying any of the information offered.

Affiliate Disclosure: Some of the links on this channel and in video descriptions are affiliate links. At no additional cost to you, we receive a commission if a purchase is made after clicking the link.

#lifeinsurance #daveramsey #infinitebanking

=================================

=========================

Caleb Guilliams

====================

*This video is for entertainment purposes only and is not financial or legal advice.

Financial Advice Disclaimer: All content on this channel is for education, discussion and illustrative purposes only and should not be construed as professional financial advice or recommendation. Should you need such advice, consult a licensed financial or tax advisor. No guarantee is given regarding the accuracy of information on this channel. Neither host or guests can be held responsible for any direct or incidental loss incurred by applying any of the information offered.

Affiliate Disclosure: Some of the links on this channel and in video descriptions are affiliate links. At no additional cost to you, we receive a commission if a purchase is made after clicking the link.

0:09:17

0:09:17

Why Infinite Banking is a SCAM!

0:20:18

0:20:18

Infinite Banking Is A Scam | Response To Dave Ramsey

0:05:26

0:05:26

The TRUTH About Infinite Banking! (Is It a Scam?)

0:09:34

0:09:34

Heated Debate Between Infinite Banker and Dave Ramsey

0:05:36

0:05:36

Is Infinite Banking Really a Scam?

0:31:55

0:31:55

Insurance Companies Are Lying to You (Infinite Banking Exposed!)

0:38:20

0:38:20

Our Response To Dave Ramsey's 'Why Infinite Banking Is A Scam' | IBC Global

0:00:58

0:00:58

Why Infinite Banking Is A SCAM!

0:49:39

0:49:39

Top 9 Worst Infinite Banking Mistakes

0:11:18

0:11:18

Why Infinite Banking is Scam: The Honest Insurance Guy

0:40:28

0:40:28

How I lost $534,000 Through Infinite Banking - The Chris Naugle

0:19:02

0:19:02

How The Mega Rich Invest | Infinite Banking Scam?

0:04:55

0:04:55

Is Infinite Banking a SCAM? The Honest Truth From An Expert

0:27:02

0:27:02

Infinite Banking Concept Explained (Honest and Unbiased)

0:13:04

0:13:04

The Infinite Banking Concept Episode 4 – Infinite Banking is a scam.

0:13:29

0:13:29

WATCH OUT! INFINITE BANKING SCAM

0:27:07

0:27:07

The 5 Biggest Negatives of Infinite Banking

0:26:50

0:26:50

Dave Ramsey's HEATED Debate with Infinite Banker - My Response

0:04:27

0:04:27

The Infinite Banking Concept explained

0:36:52

0:36:52

Why Infinite Banking is a SCAM! | Reaction to Dave Ramsey’s Video | Wealth Nation

0:29:03

0:29:03

Why Dave Ramsey's Advice on Infinite Banking is a SCAM!

0:03:53

0:03:53

Infinite Banking Scam

1:06:09

1:06:09

Is Infinite Banking a SCAM? Dave Ramsey Says So

0:09:26

0:09:26

Is Infinite Banking a Scam | Infinite Banking with Chris Miles

Комментарии