filmov

tv

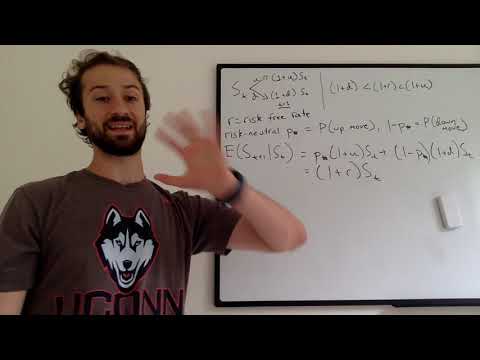

Risk neutral probability measure simplified

Показать описание

#research #review #learning

0:10:12

0:10:12

Risk neutral probability measure simplified

0:08:34

0:08:34

5. Risk Neutral Probability

0:27:25

0:27:25

Simplified: Change of Probability Measure, and Risk Neutral Valuation

0:15:30

0:15:30

6.4 from risk neutral measure to m-forward measure

0:07:45

0:07:45

Pricing a Call Option using a Risk Neutral Tree Measure.

0:24:44

0:24:44

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

0:01:48

0:01:48

Understanding Risk Neutral Measures

0:03:47

0:03:47

CFA Level 1 | Derivatives: Deriving the Risk Neutral Probability

0:01:58

0:01:58

What is Risk Neutral?

0:21:56

0:21:56

Risk-neutral probabilities (FRM T5-07)

0:22:23

0:22:23

4 2 Risk neutral pricing Part 1

0:11:26

0:11:26

Binomial Option Pricing Model (Risk Neutral Valuation Approach) | FRM Part 1

0:49:52

0:49:52

19. Black-Scholes Formula, Risk-neutral Valuation

0:07:37

0:07:37

Two State Replication & Risk Neutral Probability - Actuarial Derivative Pricing #4

0:00:27

0:00:27

Risk Neutrality

0:00:52

0:00:52

Risk Neutral Valuation

0:03:50

0:03:50

Risk Neutral Density: The Breeden-Litzenberger Formula

0:27:14

0:27:14

Risk Neutral Pricing of Weather Derivatives

0:09:49

0:09:49

Real World Vs Risk Neutral Default Probabilities (FRM Part 2, Book 2, Credit Risk)

0:07:18

0:07:18

Risk-neutral measure

0:05:52

0:05:52

The Black-Scholes Formula Explained

0:13:35

0:13:35

Risk Neutral Probability- Binomial Option Pricing Model

0:04:07

0:04:07

Risk Averse, Risk Seeker & Risk neutral

0:16:35

0:16:35

6 4 Risk neutral pricing Black Scholes Merton model Part 1

Комментарии