filmov

tv

Understanding Risk Neutral Measures

Показать описание

Explain : Risk Neutral Measures

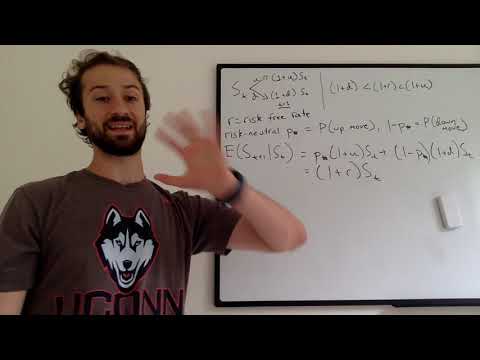

A risk neutral measure is a probability measure used in mathematical finance to aid in pricing derivatives and other financial assets. Risk neutral measures give investors a mathematical interpretation of the overall market’s risk averseness to a particular asset, which must be taken into account in order to estimate the correct price for that asset.

A risk neutral measure is also known as an equilibrium measure or equivalent martingale measure.

A risk neutral measure is a probability measure used in mathematical finance to aid in pricing derivatives and other financial assets. Risk neutral measures give investors a mathematical interpretation of the overall market’s risk averseness to a particular asset, which must be taken into account in order to estimate the correct price for that asset.

A risk neutral measure is also known as an equilibrium measure or equivalent martingale measure.

0:10:12

0:10:12

0:01:48

0:01:48

0:08:34

0:08:34

0:24:44

0:24:44

0:15:30

0:15:30

0:22:23

0:22:23

0:11:42

0:11:42

0:07:45

0:07:45

3:00:32

3:00:32

0:21:56

0:21:56

0:01:58

0:01:58

0:07:18

0:07:18

0:36:18

0:36:18

0:16:35

0:16:35

0:08:20

0:08:20

0:03:56

0:03:56

0:00:31

0:00:31

0:27:14

0:27:14

0:00:27

0:00:27

0:07:30

0:07:30

1:20:34

1:20:34

0:13:35

0:13:35

0:13:21

0:13:21

0:19:25

0:19:25