filmov

tv

Risk-neutral probabilities (FRM T5-07)

Показать описание

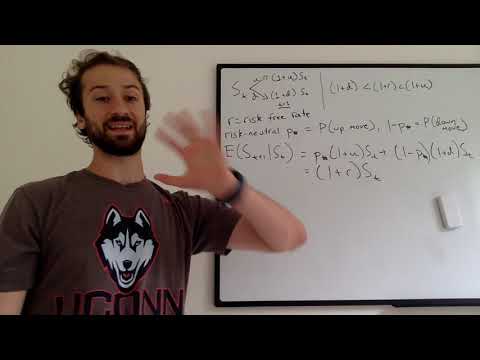

One of the harder ideas in fixed income is risk-neutral probabilities. In this video, I'd like to specifically illustrate, and define, what we mean by risk-neutral probabilities. I will do this in three steps. The first one is just a simple example of a coin toss, where my objective is to illustrate what we mean by risk-neutral probabilities. These are the probabilities that equate the expected discounted value to the market price of the instrument. Then, having defined the concept, in the second sheet I've replicated Bruce Tuckman's example in Chapter 7 where he retrieves the risk-neutral probabilities that are implied by a 1 year zero coupon bond. We'll take those risk-neutral probabilities and go to the third sheet and use them to price or value an option on that same bond so that's a contingent claim. Then we'll see why there is some magic to these risk-neutral probabilities because we're going to be able to use them to price the option and we'll get a price that's necessarily equal to the price if we were to value the option with a replicating portfolio, which is something of an unambiguous value that would be indifferent to our risk preferences. So, I look forward to that illustration of risk-neutral probabilities.

to be notified of future tutorials on expert finance and data science, including the Financial Risk Manager (FRM), the Chartered Financial Analyst (CFA), and R Programming!

For other videos in our Financial Risk Manager (FRM) series, visit these playlists:

Texas Instruments BA II+ Calculator

Risk Foundations (FRM Topic 1)

Quantitative Analysis (FRM Topic 2)

Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

Financial Markets and Products: Option Trading Strategies (FRM Topic 3, Hull Ch 10-12)

FM&P: Intro to Derivatives: Exotic options (FRM Topic 3)

Valuation and Risk Models (FRM Topic 4)

Market Risk (FRM Topic 5)

Coming Soon ....

Credit Risk (FRM Topic 6)

Operational Risk (FRM Topic 7)

Investment Risk (FRM Topic 8)

Current Issues (FRM Topic 9)

For videos in our Chartered Financial Analyst (CFA) series, visit these playlists:

Chartered Financial Analyst (CFA) Level 1 Volume 1

#bionicturtle #risk #financialriskmanager #FRM #finance #expertfinance

to be notified of future tutorials on expert finance and data science, including the Financial Risk Manager (FRM), the Chartered Financial Analyst (CFA), and R Programming!

For other videos in our Financial Risk Manager (FRM) series, visit these playlists:

Texas Instruments BA II+ Calculator

Risk Foundations (FRM Topic 1)

Quantitative Analysis (FRM Topic 2)

Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

Financial Markets and Products: Option Trading Strategies (FRM Topic 3, Hull Ch 10-12)

FM&P: Intro to Derivatives: Exotic options (FRM Topic 3)

Valuation and Risk Models (FRM Topic 4)

Market Risk (FRM Topic 5)

Coming Soon ....

Credit Risk (FRM Topic 6)

Operational Risk (FRM Topic 7)

Investment Risk (FRM Topic 8)

Current Issues (FRM Topic 9)

For videos in our Chartered Financial Analyst (CFA) series, visit these playlists:

Chartered Financial Analyst (CFA) Level 1 Volume 1

#bionicturtle #risk #financialriskmanager #FRM #finance #expertfinance

0:21:56

0:21:56

Risk-neutral probabilities (FRM T5-07)

0:10:12

0:10:12

Risk neutral probability measure simplified

0:08:34

0:08:34

5. Risk Neutral Probability

0:07:45

0:07:45

Pricing a Call Option using a Risk Neutral Tree Measure.

0:22:23

0:22:23

4 2 Risk neutral pricing Part 1

0:00:27

0:00:27

Risk Neutrality

0:15:30

0:15:30

6.4 from risk neutral measure to m-forward measure

0:01:58

0:01:58

What is Risk Neutral?

0:13:35

0:13:35

Risk Neutral Probability- Binomial Option Pricing Model

0:24:44

0:24:44

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

0:03:50

0:03:50

Risk Neutral Density: The Breeden-Litzenberger Formula

0:07:18

0:07:18

Risk-neutral measure

0:07:49

0:07:49

4 4 Risk neutral pricing Part 3

0:13:37

0:13:37

6 5 Risk neutral pricing Black Scholes Merton model Part 2

0:15:26

0:15:26

Risk Neutral Pricing of Call Options

0:06:17

0:06:17

One Step Binomial Tree - Risk Neutral Probability Derivation

0:29:49

0:29:49

Lecture 2022-1 (30): Numerical Methods: Excursus: Density of the Underlying of European Options

0:21:03

0:21:03

Risk Management in Finance: 7. Risk Neutral Valuation, Scenario Analysis

0:03:13

0:03:13

Risk neutral method part1

0:25:25

0:25:25

Binomial options pricing - Replicating portfolio and Risk neutral probability - 1

0:13:21

0:13:21

4 3 Risk neutral pricing Part 2

0:03:02

0:03:02

Binomial Trees and risk neutral valuation

0:05:41

0:05:41

Lecture 12 Part 4

0:29:29

0:29:29

Binomial options pricing - Replicating portfolio and Risk neutral probability - 2

Комментарии