filmov

tv

Basic Automotive Insurance Coverage Explained

Показать описание

While everyone that drives in this country has to have some form of auto insurance by law, many do not understand the basics of their policies. While we don't all have to be auto insurance experts, it is important to at least comprehend the major bricks that build our auto insurance policies.

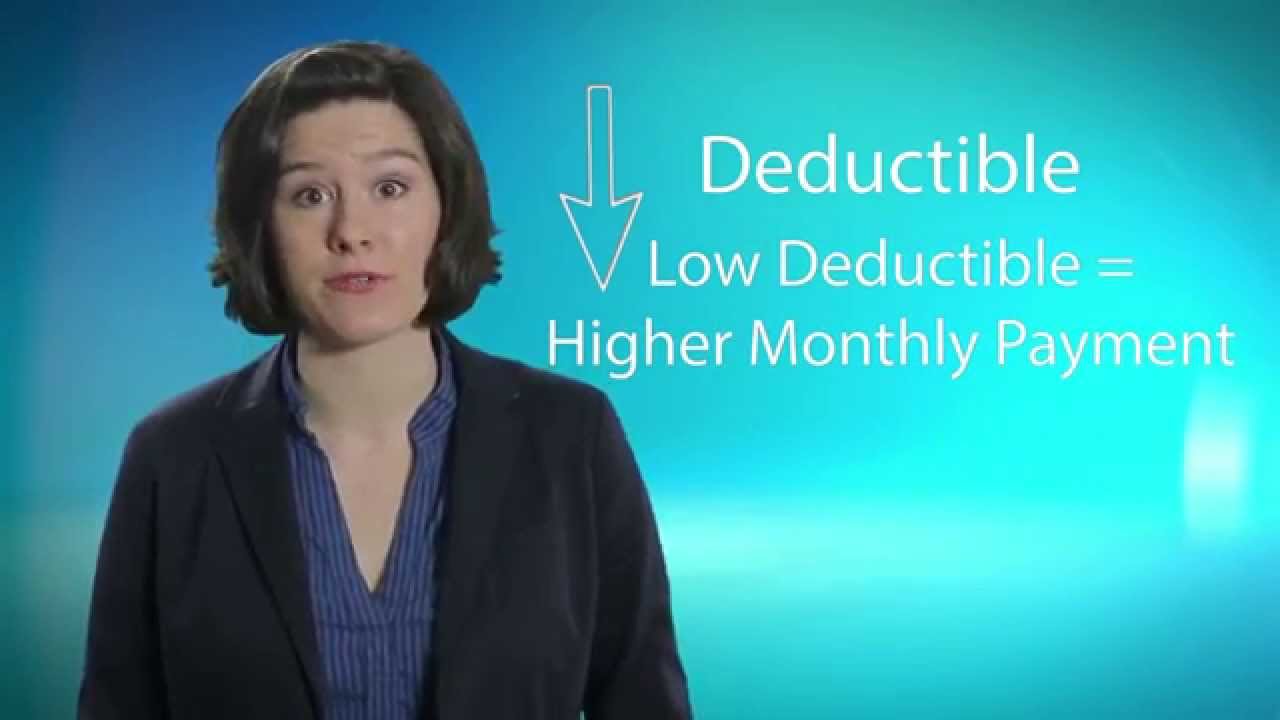

Collision Coverage.

This covers loss to your own auto caused by its collision with another vehicle or object. If you cause an accident, collision coverage will pay to repair your vehicle, and is normally the most expensive part of an auto insurance policy. You must choose a deductible, which is the amount you, the insured, must pay before the insurance company pays the remainder of each covered loss. The higher the deductible, the lower the premium costs. However, keep in mind that this is the amount you must pay (generally to the repair shop) if your vehicle is damaged, so deciding on your deductible, which directly affects your premium, can be a bit of a balancing act.

Comprehensive Coverage.

This covers damage to your vehicle caused by an event other than a collision or overturn. Examples include fire, theft, vandalism, and falling objects. This also comes with a deductible you select, which is how much you will pay before the insurance company pays the remainder.

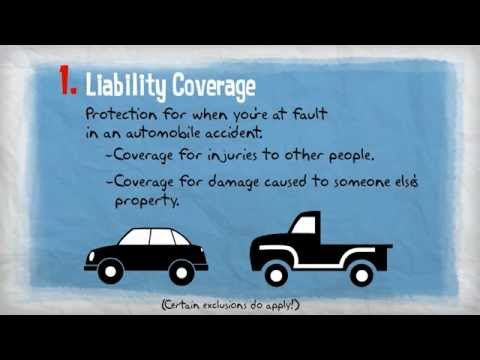

Liability.

The official definition of liability from the InsWeb glossary is: "That portion of the insurance contract which pays and renders service on behalf of an insured for a covered loss arising out of the insured's responsibility to others imposed by law or assumed by contract." In simpler terms, if you are at fault in an accident, liability insurance will pay to cover injuries and property damage costs caused to others in the accident (including your legal defense costs, if applicable). Bodily injury coverage pays for things like medical costs and lost salary to others; while property damage pays for repairs to other people's property you damaged in the accident (other than your own car). Liability coverage (which is the state mandated part of your policy) is the basic building block of any auto policy, and minimum liability limits vary from state to state.

Below are some common extra coverage items that are available to you:

Medical Payments

This pays you and your passengers for medical and funeral expenses incurred in an auto accident, regardless of fault. It will also cover injuries sustained by you while you're operating someone else's car (with their permission), in addition to injuries you or your family members incur when you are pedestrians.

Personal Injury Protection

This is the name usually given to no-fault benefits in states that have enacted mandatory or optional no-fault auto insurance laws. Personal Injury Protection (PIP) usually includes benefits for medical expenses, loss of income from work, essential services, accidental death, funeral expenses, and survivor benefits.

No-Fault Insurance

Many states have enacted auto accident compensation laws permitting auto accident victims to collect directly from their own insurance companies for medical and hospital expenses regardless of who was at fault in the accident. Although there are many legal variations of no-fault insurance, most states still allow people to sue the negligent party if the amount of damages exceeds a certain state-determined threshold.

Uninsured/Underinsured Motorists Coverage:

Uninsured Motorists Bodily Injury

Uninsured Motorists Bodily Injury (UMBI) covers you for all sums (up to your policy limits) if an accident occurs with an uninsured or hit-and-run motorist who is determined to be legally at fault.

Underinsured Motorists Bodily Injury

Underinsured Motorist Bodily Injury covers you for all sums (up to your policy limits) if an accident occurs with a motorist who is underinsured (i.e., they carry bodily injury limits less than your UMBI limits and less than the amount of the injuries).

Uninsured Motorists Property Damage

Uninsured Motorist Property Damage (UMPD) Liability coverage pays for property damages caused by uninsured drivers.

There are also other extra items, such as rental reimbursement and towing and labor charges in case of a breakdown. As mentioned above, please visit the Insweb Auto Insurance Glossary for further definitions.

Remember to keep yourself adequately covered; while having the bare minimums required by each state may keep you in compliance with state laws, they may not be enough to protect your assets if you have a major incident. Insurance experts recommend that you review your insurance policy often and thoroughly.

Collision Coverage.

This covers loss to your own auto caused by its collision with another vehicle or object. If you cause an accident, collision coverage will pay to repair your vehicle, and is normally the most expensive part of an auto insurance policy. You must choose a deductible, which is the amount you, the insured, must pay before the insurance company pays the remainder of each covered loss. The higher the deductible, the lower the premium costs. However, keep in mind that this is the amount you must pay (generally to the repair shop) if your vehicle is damaged, so deciding on your deductible, which directly affects your premium, can be a bit of a balancing act.

Comprehensive Coverage.

This covers damage to your vehicle caused by an event other than a collision or overturn. Examples include fire, theft, vandalism, and falling objects. This also comes with a deductible you select, which is how much you will pay before the insurance company pays the remainder.

Liability.

The official definition of liability from the InsWeb glossary is: "That portion of the insurance contract which pays and renders service on behalf of an insured for a covered loss arising out of the insured's responsibility to others imposed by law or assumed by contract." In simpler terms, if you are at fault in an accident, liability insurance will pay to cover injuries and property damage costs caused to others in the accident (including your legal defense costs, if applicable). Bodily injury coverage pays for things like medical costs and lost salary to others; while property damage pays for repairs to other people's property you damaged in the accident (other than your own car). Liability coverage (which is the state mandated part of your policy) is the basic building block of any auto policy, and minimum liability limits vary from state to state.

Below are some common extra coverage items that are available to you:

Medical Payments

This pays you and your passengers for medical and funeral expenses incurred in an auto accident, regardless of fault. It will also cover injuries sustained by you while you're operating someone else's car (with their permission), in addition to injuries you or your family members incur when you are pedestrians.

Personal Injury Protection

This is the name usually given to no-fault benefits in states that have enacted mandatory or optional no-fault auto insurance laws. Personal Injury Protection (PIP) usually includes benefits for medical expenses, loss of income from work, essential services, accidental death, funeral expenses, and survivor benefits.

No-Fault Insurance

Many states have enacted auto accident compensation laws permitting auto accident victims to collect directly from their own insurance companies for medical and hospital expenses regardless of who was at fault in the accident. Although there are many legal variations of no-fault insurance, most states still allow people to sue the negligent party if the amount of damages exceeds a certain state-determined threshold.

Uninsured/Underinsured Motorists Coverage:

Uninsured Motorists Bodily Injury

Uninsured Motorists Bodily Injury (UMBI) covers you for all sums (up to your policy limits) if an accident occurs with an uninsured or hit-and-run motorist who is determined to be legally at fault.

Underinsured Motorists Bodily Injury

Underinsured Motorist Bodily Injury covers you for all sums (up to your policy limits) if an accident occurs with a motorist who is underinsured (i.e., they carry bodily injury limits less than your UMBI limits and less than the amount of the injuries).

Uninsured Motorists Property Damage

Uninsured Motorist Property Damage (UMPD) Liability coverage pays for property damages caused by uninsured drivers.

There are also other extra items, such as rental reimbursement and towing and labor charges in case of a breakdown. As mentioned above, please visit the Insweb Auto Insurance Glossary for further definitions.

Remember to keep yourself adequately covered; while having the bare minimums required by each state may keep you in compliance with state laws, they may not be enough to protect your assets if you have a major incident. Insurance experts recommend that you review your insurance policy often and thoroughly.

0:05:02

0:05:02

Basic Automotive Insurance Coverage Explained

0:01:46

0:01:46

Understanding Auto Insurance: What’s ‘Full Coverage’ Car Insurance?

0:13:19

0:13:19

Car Insurance Explained - 101 | Everything you NEED to know!

0:03:00

0:03:00

Insurance 101 - Personal Auto Coverages

0:05:51

0:05:51

Liability Auto Insurance 101

0:02:14

0:02:14

Basic Automotive Insurance Coverage Explained

0:04:49

0:04:49

How Much Car Insurance Do I Actually Need?

0:00:57

0:00:57

Comprehensive Insurance Explained! | Car Insurance 101

0:00:25

0:00:25

Basic Automotive Insurance Coverage Explained|2016|

0:02:56

0:02:56

Auto Insurance Coverages Explained

0:10:42

0:10:42

Car Insurance Explained - Understanding the basics of Car Insurance

0:12:02

0:12:02

7 mistakes people make when purchasing car insurance

0:05:36

0:05:36

What Car Insurance Do I Need | How much Auto Insurance you need today - Basic

0:01:28

0:01:28

Understanding Auto Insurance: What To Expect During A Car Insurance Claim?

0:22:28

0:22:28

Understanding Car insurance - What you need to know 101

0:16:25

0:16:25

How Much Car Insurance Do You Need | 4 EASY STEPS

0:00:50

0:00:50

Understanding Auto Insurance: Collision Coverage

0:04:05

0:04:05

Car Insurance explained - Comprehensive Insurance

0:04:08

0:04:08

Simplified: Vehicle Insurance | Types of Vehicle Insurance - Explained | PowerDrift

0:03:18

0:03:18

“Full Coverage” Car Insurance Explained

0:00:44

0:00:44

Understanding Auto Insurance: Comprehensive Coverage

0:00:44

0:00:44

Understanding Auto Insurance: Bodily Injury Coverage

0:08:49

0:08:49

Car Insurance Explained: A Guide That Covers Everything

0:02:42

0:02:42

Insurance 101 - Personal Auto Limits

Комментарии