filmov

tv

Statement of Cash Flows: Direct Method - Lesson 1

Показать описание

In this video, 25.03 – Statement of Cash Flows: Direct Method – Lesson 1, Roger Philipp, CPA, CGMA, first compares and contrasts the two methods for calculating operating activities cash flows.

The direct method requires directly analyzing each item on the income statement and converting it from accrual to cash. The indirect method involves starting with net income and indirectly reconciling back to the ending balance on the statement of cash flows via a series of analysis and adjustments.

Roger then moves from theory to application by setting up a statement of cash flows example for teaching the direct method.

Video Transcript Sneak Peek:

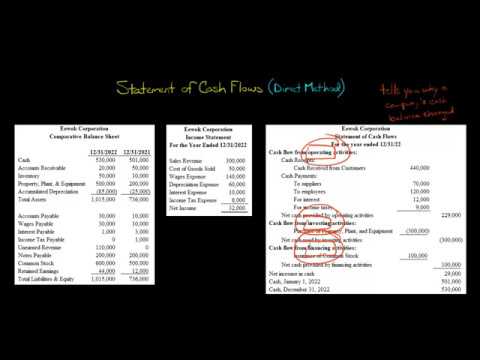

Ok, let's move on to operating activity section. Now remember we talked about the statement and cash flows, we said three main areas. Which are what? It's called operating, investing, and financing, then we have our net change, and so on. The thing is, there are two ways to do the operating activity section. So when we talked about net cash provided by operating activities, we ended up with this number here, which was $135.

The direct method requires directly analyzing each item on the income statement and converting it from accrual to cash. The indirect method involves starting with net income and indirectly reconciling back to the ending balance on the statement of cash flows via a series of analysis and adjustments.

Roger then moves from theory to application by setting up a statement of cash flows example for teaching the direct method.

Video Transcript Sneak Peek:

Ok, let's move on to operating activity section. Now remember we talked about the statement and cash flows, we said three main areas. Which are what? It's called operating, investing, and financing, then we have our net change, and so on. The thing is, there are two ways to do the operating activity section. So when we talked about net cash provided by operating activities, we ended up with this number here, which was $135.

0:12:12

0:12:12

Intro to Cash Flow Statements | Direct Method

0:18:13

0:18:13

Prepare A Cash Flow Statement | Direct Method

0:08:09

0:08:09

Statement of Cash Flows (Direct Method)

0:29:38

0:29:38

Cash Flow Statement | Direct Method | Full Example

0:21:21

0:21:21

FA 46 - Statement of Cash Flows Example - Direct Method

0:05:57

0:05:57

Direct vs. Indirect Method Statement of Cash Flows

0:06:50

0:06:50

Statement of Cash Flows Direct Method

0:04:47

0:04:47

Cash flow statement direct vs indirect method

0:27:10

0:27:10

6# Financial statements in Kannada. Profit and Loss A/C. I PUC Karnataka class 11

0:05:17

0:05:17

Statement of Cash Flows: Direct Method - Lesson 2

0:05:43

0:05:43

Statement of Cash Flows: Direct Method - Lesson 1

0:21:15

0:21:15

Cash flows from operating activities - direct method (for the @CFA Level 1 exam)

0:06:00

0:06:00

Cash flow statement direct method

0:15:10

0:15:10

The CASH FLOW STATEMENT for BEGINNERS

0:14:44

0:14:44

Direct Method Statement of Cash Flows

0:55:56

0:55:56

IAS 7 - STATEMENT OF CASHFLOWS (PART 1)

0:13:26

0:13:26

Cash Flow Statement Basics Explained

0:14:39

0:14:39

Statement of Cash flow - Direct Method 12 min

0:11:15

0:11:15

Prepare A Cash Flow Statement | Indirect Method

0:06:58

0:06:58

Cash flow direct method example

0:25:12

0:25:12

Statement of cash Flow: Direct Method. Intermediate Accounting

0:09:16

0:09:16

CFA Level I FRA - Cash Flow Statements Direct vs Indirect methods

0:05:02

0:05:02

Statement of Cash Flows: Direct Method - Lesson 3

0:16:57

0:16:57

Accounting Basics 9.1a: Cash Flow Statement - Direct Method Example

Комментарии