filmov

tv

Statement of Cash Flows (Direct Method)

Показать описание

This video provides an overview of the Direct Method for preparing the Statement of Cash Flows.

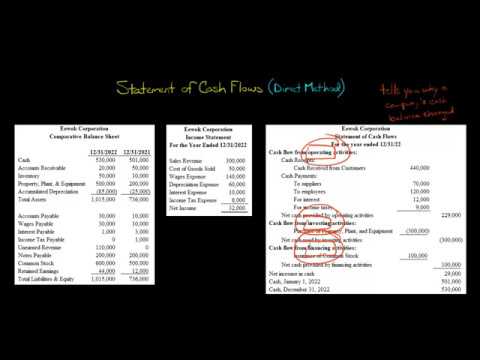

The Statement of Cash Flows has three sections: the operating section, the investing section, and the financing section. This is true whether the direct or indirect method is used. The investing section lists the cash flows for the period that pertained to the purchase and sell of productive assets (e.g., property, plant, and equipment or long-term investments). The financing section lists the cash flows that pertained to transactions with the company's owners (issuing stock, repurchasing stock, paying dividends) or creditors (borrowing money, repaying loans). The investing section and financing section are identical regardless of whether the direct method or indirect method is used.

With the direct method, the operating section is prepared by taking the company's Income Statement and converting it to a cash-basis. The Income Statement was prepared using accrual accounting (e.g., credit sales were included in sales revenue) so to create the operating section you go line-by-line through the Income Statement and convert each line item to cash basis (e.g., sales revenue becomes cash received from customers). Non-cash charges that appear in the Income Statement (e.g., depreciation expense, amortization expense) are not included in the operating section per the Direct Method because they are non-cash charges.

Thus, the operating section prepared according to the direct method presents the company's cash receipts (e.g., cash received from customers, cash received from interest) minus the company's cash payments (e.g., cash paid to suppliers, cash paid for interest, cash paid for income taxes) to arrive at the net cash provided (or used) by operating activities (which is what Net Income would have been had the Income Statement been prepared on a cash-basis instead of an accrual-basis).—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

The Statement of Cash Flows has three sections: the operating section, the investing section, and the financing section. This is true whether the direct or indirect method is used. The investing section lists the cash flows for the period that pertained to the purchase and sell of productive assets (e.g., property, plant, and equipment or long-term investments). The financing section lists the cash flows that pertained to transactions with the company's owners (issuing stock, repurchasing stock, paying dividends) or creditors (borrowing money, repaying loans). The investing section and financing section are identical regardless of whether the direct method or indirect method is used.

With the direct method, the operating section is prepared by taking the company's Income Statement and converting it to a cash-basis. The Income Statement was prepared using accrual accounting (e.g., credit sales were included in sales revenue) so to create the operating section you go line-by-line through the Income Statement and convert each line item to cash basis (e.g., sales revenue becomes cash received from customers). Non-cash charges that appear in the Income Statement (e.g., depreciation expense, amortization expense) are not included in the operating section per the Direct Method because they are non-cash charges.

Thus, the operating section prepared according to the direct method presents the company's cash receipts (e.g., cash received from customers, cash received from interest) minus the company's cash payments (e.g., cash paid to suppliers, cash paid for interest, cash paid for income taxes) to arrive at the net cash provided (or used) by operating activities (which is what Net Income would have been had the Income Statement been prepared on a cash-basis instead of an accrual-basis).—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

Statement of Cash Flows (Direct Method)

0:18:13

0:18:13

Prepare A Cash Flow Statement | Direct Method

0:12:12

0:12:12

Intro to Cash Flow Statements | Direct Method

0:21:21

0:21:21

FA 46 - Statement of Cash Flows Example - Direct Method

0:05:57

0:05:57

Direct vs. Indirect Method Statement of Cash Flows

0:06:50

0:06:50

Statement of Cash Flows Direct Method

0:04:47

0:04:47

Cash flow statement direct vs indirect method

0:14:44

0:14:44

Direct Method Statement of Cash Flows

0:21:20

0:21:20

#11 Cash Flow Statements - Problem 13 - MAY 2024 Question - By Saheb Academy

0:05:43

0:05:43

Statement of Cash Flows: Direct Method - Lesson 1

0:15:10

0:15:10

The CASH FLOW STATEMENT for BEGINNERS

0:05:17

0:05:17

Statement of Cash Flows: Direct Method - Lesson 2

0:21:06

0:21:06

Statement of Cash Flows- Direct Method (Part 2)

0:29:38

0:29:38

Cash Flow Statement | Direct Method | Full Example

0:14:39

0:14:39

Statement of Cash flow - Direct Method 12 min

0:11:15

0:11:15

Prepare A Cash Flow Statement | Indirect Method

0:05:02

0:05:02

Statement of Cash Flows: Direct Method - Lesson 3

0:25:12

0:25:12

Statement of cash Flow: Direct Method. Intermediate Accounting

0:55:56

0:55:56

IAS 7 - STATEMENT OF CASHFLOWS (PART 1)

0:13:26

0:13:26

Cash Flow Statement Basics Explained

0:21:15

0:21:15

Cash flows from operating activities - direct method (for the @CFA Level 1 exam)

0:06:50

0:06:50

Cashflow Statement | Direct Method Format | CA CMA Inter | CARAJACLASSES

0:10:21

0:10:21

FA 45 - Statement of Cash Flows Explained

0:24:23

0:24:23

1/2 | CAHAYA |DIRECT METHOD | STATEMENT OF CASH FLOWS - TUTORIAL : STEP BY STEP | FAR210

Комментарии