filmov

tv

Dynamic Delta Hedging Explained In Excel

Показать описание

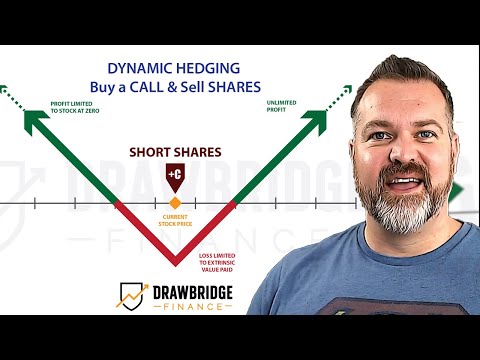

Explore the fundamentals of Dynamic Delta Hedging in this detailed tutorial, "Dynamic Delta Hedging Explained In Excel." Begin with an introduction to the delta hedging problem, and advance through practical steps such as time to maturity calculations and delta calculation using the Black Scholes model. Discover how to maintain a delta-neutral portfolio by adjusting your hedge weekly through trading shares, and understand how to calculate the costs associated with these strategies. This guide employs an example from John C. Hull's "Options, Futures, and Other Derivatives" to provide a clear application context in financial markets.

🎓 Tutor With Me: 1-On-1 Video Call Sessions Available

💾 Download Free Excel File:

📚 CFA Exam Prep Discount - AnalystPrep:

📘 FRM Exam Prep Discount - AnalystPrep:

Chapters:

0:00 - Dynamic Delta Hedging Problem Introduction

2:40 - Time to Maturity Calculations

3:19 - Calculate Delta Using Black Scholes

7:17 - Trade Shares to Hedge Weekly

9:33 - Calculate the Cost of the Hedge

*Disclosure: This is not financial advice and should not be taken as such. The information contained in this video is an opinion. Some of the information could be wrong. This channel is owned and operated by Portfolio Constructs LLC. Some of the links above are affiliate links, meaning, at no additional cost to you, I will earn a commission if you click through and make a purchase.

🎓 Tutor With Me: 1-On-1 Video Call Sessions Available

💾 Download Free Excel File:

📚 CFA Exam Prep Discount - AnalystPrep:

📘 FRM Exam Prep Discount - AnalystPrep:

Chapters:

0:00 - Dynamic Delta Hedging Problem Introduction

2:40 - Time to Maturity Calculations

3:19 - Calculate Delta Using Black Scholes

7:17 - Trade Shares to Hedge Weekly

9:33 - Calculate the Cost of the Hedge

*Disclosure: This is not financial advice and should not be taken as such. The information contained in this video is an opinion. Some of the information could be wrong. This channel is owned and operated by Portfolio Constructs LLC. Some of the links above are affiliate links, meaning, at no additional cost to you, I will earn a commission if you click through and make a purchase.

0:12:56

0:12:56

Dynamic Delta Hedging Explained In Excel

0:14:11

0:14:11

Delta Hedging Explained: Options Trading Strategies

0:10:32

0:10:32

What is Delta Hedging || Dynamic Delta Hedging like a Quant || Profit & Loss Options Trading

0:19:46

0:19:46

Dynamic option delta hedge (FRM T4-14)

0:14:32

0:14:32

Delta Hedging Explained | Options Trading Lesson

0:19:46

0:19:46

Dynamic Hedging Options - Make money if the stock moves either direction

0:06:55

0:06:55

AdvFinMod Topic 17 Section 6 Simulating Dynamic Delta Hedged Profits

0:06:00

0:06:00

Dynamic Hedging of Options - Option Trading Strategies

0:06:34

0:06:34

AdvFinMod Topic 17 Section 7 Dynamic Delta Hedged Profits for Long and Short, Calls and Puts

0:12:09

0:12:09

Hedging Deltas: Gamma, Vanna 101

0:03:56

0:03:56

Risk Management: Short Option - Delta Hedge - Simple

0:07:26

0:07:26

AdvFinMod Topic 17 Section 5 Dynamic Delta Hedged Profits

0:25:38

0:25:38

Delta Hedging Example

0:05:18

0:05:18

Delta Neutral Hedging - Neutral Options Strategies - Options Trading Strategies

0:09:36

0:09:36

Bill Explains Dynamic Hedging

0:10:28

0:10:28

How To Delta Hedge Your Options Portfolio? I Delta hedging

0:04:14

0:04:14

What is Delta Hedging | How to reduce risk in your portfolio using Optionlogy

0:14:44

0:14:44

Hedging (aka, neutralizing) option delta and gamma (FRM T4-19)

0:19:41

0:19:41

Advanced DELTA HEDGING Technique To SAVE Your Option Trades 💰

0:12:22

0:12:22

CFA Level 2 Mini-Lesson: Nathan Explains Delta Hedging (Dynamic Hedging) for Options

0:05:39

0:05:39

8.6 Delta hedging - Deribit Options Course Basics

0:08:03

0:08:03

Jedi Options - The Role of a Market Maker and Delta Hedging

0:21:24

0:21:24

Dynamic Delta Hedging Explained: Python computation included

0:10:29

0:10:29

Gamma? Delta Hedging? What Is It & Why Does It Matter?

Комментарии