filmov

tv

How Much Car Payment Can You Really Afford? (3 Simple Rules)

Показать описание

How much car payment can I afford?

(I may be compensated by LightStream through this link.)

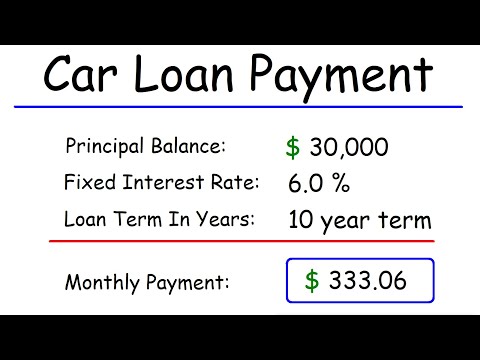

You might've heard of the 20/4/10 rule for car affordability, but this is my modified version (20/5/10). You don't have to take this advice, but I think it's a good start on how much your car payment should realistically be. Start with 20% down, don't exceed a 60 month loan and try to keep the monthly payment and car expenses below 10% of your net monthly income. So if you bring in $5,000 per month after taxes, then your car payment and added expenses should be about $500 per month (after 20% down). That's how I calculate car affordability.

---------------

Robinhood Free Stock (Up to $200) with Sign Up:

Webull Up to 12 Free Fracional Shares (Each $3-$3,000):

M1 Finance (perfect for IRA's):

Instagram:

Advertiser Disclosure: Honest Finance participates in affiliate sales networks and may receive compensation by clicking through the links (at no cost to you). This compensation may impact how and where links appear in this description. The content in this video is accurate as of the posting date. Some of the offers mentioned may no longer be available. This channel does not include all financial companies or all available financial offers.

---------------

Honest Finance covers a broad range of financial topics that'll give your life and finances more value. Subscribe today for future content and be sure to give this video a like!

Disclaimer: I am not a financial advisor. These videos are for education/entertainment purposes only. Investing of any kind involves risk, so please conduct your own research.

#honestfinance #carbuying

(I may be compensated by LightStream through this link.)

You might've heard of the 20/4/10 rule for car affordability, but this is my modified version (20/5/10). You don't have to take this advice, but I think it's a good start on how much your car payment should realistically be. Start with 20% down, don't exceed a 60 month loan and try to keep the monthly payment and car expenses below 10% of your net monthly income. So if you bring in $5,000 per month after taxes, then your car payment and added expenses should be about $500 per month (after 20% down). That's how I calculate car affordability.

---------------

Robinhood Free Stock (Up to $200) with Sign Up:

Webull Up to 12 Free Fracional Shares (Each $3-$3,000):

M1 Finance (perfect for IRA's):

Instagram:

Advertiser Disclosure: Honest Finance participates in affiliate sales networks and may receive compensation by clicking through the links (at no cost to you). This compensation may impact how and where links appear in this description. The content in this video is accurate as of the posting date. Some of the offers mentioned may no longer be available. This channel does not include all financial companies or all available financial offers.

---------------

Honest Finance covers a broad range of financial topics that'll give your life and finances more value. Subscribe today for future content and be sure to give this video a like!

Disclaimer: I am not a financial advisor. These videos are for education/entertainment purposes only. Investing of any kind involves risk, so please conduct your own research.

#honestfinance #carbuying

0:05:06

0:05:06

How Much Car Payment Can You Really Afford? (3 Simple Rules)

0:00:33

0:00:33

How much is your car payment?

0:00:50

0:00:50

$3,200/month in Car Payments? What Do You Drive?!

0:10:44

0:10:44

How To Calculate Your Car Loan Payment

0:00:15

0:00:15

How Much is your Car Payment? 🚘⁉️

0:00:49

0:00:49

What’s your Car Payment? #mercedes #shorts #cars

0:01:59

0:01:59

How to Calculate Car Payments

0:09:18

0:09:18

The Ramsey Show Reacts To These High Car Payments!

0:00:33

0:00:33

E-Z pass could be used soon to pay for gas

0:09:28

0:09:28

Paying Off Car Loan Early | Principal vs Extra Payment Explained

0:05:25

0:05:25

What Is The Math Of Car Loans Vs Buying At Full Payment?

0:11:55

0:11:55

HELP! I Make $2,000 And Have A $600 Car Payment

0:03:21

0:03:21

My Car Payment is $1,200/Month!

0:00:34

0:00:34

How Much is your Car Payment? Part 2 🤔🚙💸

0:02:57

0:02:57

How Many Car Payments Can You Miss Before Repo?

0:00:39

0:00:39

How much is a 40k car monthly payment?

0:10:46

0:10:46

“Families Are Going To Feel This!' - The Scary Math Behind Car Payments

0:00:57

0:00:57

How much is a monthly payment on a $30,000 car?

0:00:52

0:00:52

How Much is your Car Payment? 🤔🚙💸

0:00:12

0:00:12

Car payments are 2X higher in 2023! 🚙

0:01:33

0:01:33

What Percent of Salary Should Be Spent on a Car Payment? : Money Management

0:00:14

0:00:14

Comment your Car Payment?💰🚗 #fyp #viral #youtubeshorts #car #money #cars #finance #drivingfails...

0:05:42

0:05:42

🔥Ex Car Salesman Reveals How to Calculate Your Car Payment-How To Buy A Car

0:20:56

0:20:56

The Car Payment Epidemic ..... The Saga Continues

Комментарии