filmov

tv

Efficient vs Inefficient Portfolios

Показать описание

This video discusses the difference between an efficient portfolio and an inefficient portfolio.

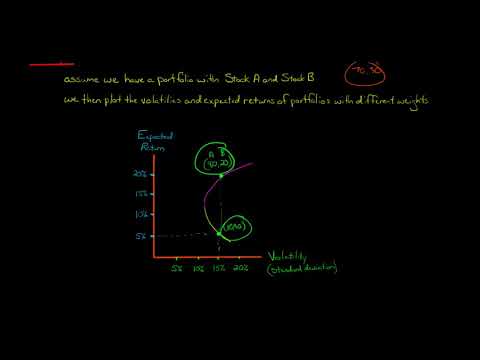

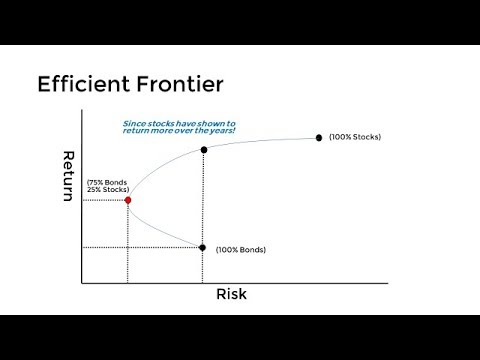

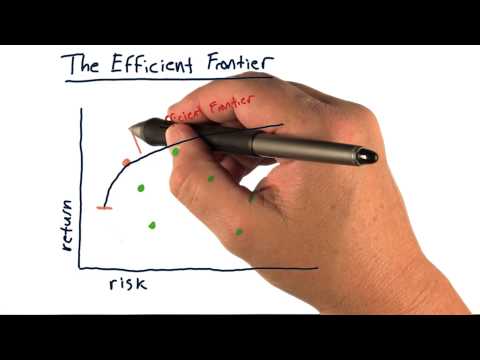

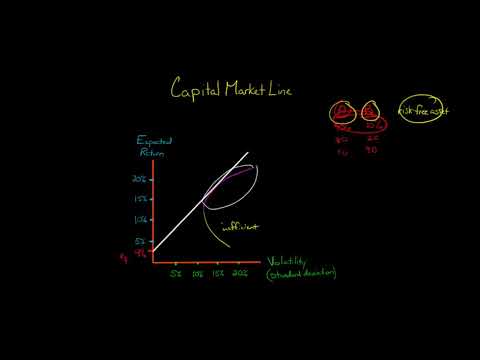

A portfolio is inefficient if there is another portfolio that has a higher expected return without having higher risk (volatility). For example, let's say Portfolio A has an expected return of 29% and Portfolio B has an expected return of 27%, and that both Portfolio A and Portfolio B have a volatility of 20%. In this example, Portfolio B is inefficient because there is another portfolio with a higher expected return that does not have higher risk (Portfolio A).

If a portfolio is efficient, this means you could not find another portfolio with a higher expected return and the same or lower volatility.

A rational investor would always rule out inefficient portfolios; if they can earn a higher return without bearing additional risk, they will do so.—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

A portfolio is inefficient if there is another portfolio that has a higher expected return without having higher risk (volatility). For example, let's say Portfolio A has an expected return of 29% and Portfolio B has an expected return of 27%, and that both Portfolio A and Portfolio B have a volatility of 20%. In this example, Portfolio B is inefficient because there is another portfolio with a higher expected return that does not have higher risk (Portfolio A).

If a portfolio is efficient, this means you could not find another portfolio with a higher expected return and the same or lower volatility.

A rational investor would always rule out inefficient portfolios; if they can earn a higher return without bearing additional risk, they will do so.—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

0:06:20

0:06:20

Efficient vs Inefficient Portfolios

0:03:39

0:03:39

Efficient and inefficient portfolios

0:03:05

0:03:05

The Efficient Frontier - Explained in 3 Minutes

0:02:54

0:02:54

The efficient frontier

0:04:50

0:04:50

Efficient vs. Inefficient Markets: Why is it harder to value some things versus others?

0:05:45

0:05:45

The Capital Market Line

0:03:49

0:03:49

Modern Portfolio Theory and the Efficient Frontier Explained

0:18:53

0:18:53

Portfolio Theory 7: The Efficient and Inefficient Frontiers of Mean Variance Optimization

0:21:35

0:21:35

Evolution of Portfolio Theory – From Efficient Frontier to CAL to SML (For CFA® and FRM® Exams)

0:09:01

0:09:01

Efficient Market Hypothesis - EMH Explained Simply

0:00:40

0:00:40

Efficient vs Inefficient Assets Strategy

0:03:06

0:03:06

Gary Shilling explains the only way to beat the market and win

0:00:12

0:00:12

Efficient vs inefficient price action 😈 spectral_smt on Instagram for in depth trading guides 📊...

0:02:35

0:02:35

What Is the Efficient Market Hypothesis?

0:09:30

0:09:30

Warren Buffett: Own Small Companies To Get Rich

0:01:40

0:01:40

Efficient vs Inefficient Structure

0:11:16

0:11:16

The Index Fund 'Tipping Point'

0:04:51

0:04:51

Warren Buffett: Why Real Estate Is a LOUSY Investment?

0:08:36

0:08:36

Efficiently Inefficient by Lasse Heje Pedersen: 8 Minute Summary

0:11:57

0:11:57

Market Operations: Efficient vs Inefficient

0:07:02

0:07:02

Is The Market Efficient?

0:05:11

0:05:11

Efficient Market Theory (AND WHAT ARE THE 3 DIFFERENT FORMS?)

0:08:50

0:08:50

Determining inefficient portfolio based on expected return and standard deviation.

0:08:47

0:08:47

Graph The Efficient Frontier And Capital Allocation Line In Excel

Комментарии