filmov

tv

The Capital Market Line

Показать описание

This video discusses the Capital Market Line.

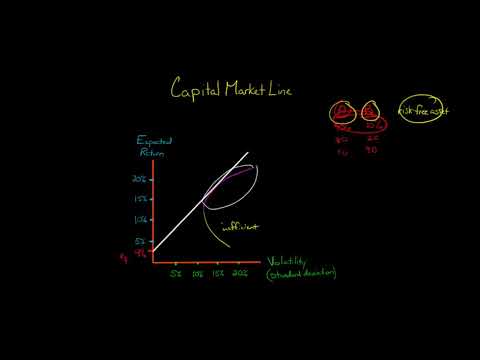

When the volatility and expected return of different portfolios weights is graphed, the line drawn from the risk-free rate such that it is tangent to the efficient frontier is called the Capital Market Line.

Along the Capital Market Line lies a series of efficient portfolios that are combinations of the risky securities with the risk-free investment.

If the assumptions of the Capital Asset Pricing Model hold, then all investors would choose the portfolio on the Capital Market Line that is tangent to the efficient frontier; this is called the tangent portfolio. The tangent portfolio is the market portfolio and it is the portfolio with the highest Sharpe Ratio. This means it provides the highest reward (expected return) per unit of risk (volatility).—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

When the volatility and expected return of different portfolios weights is graphed, the line drawn from the risk-free rate such that it is tangent to the efficient frontier is called the Capital Market Line.

Along the Capital Market Line lies a series of efficient portfolios that are combinations of the risky securities with the risk-free investment.

If the assumptions of the Capital Asset Pricing Model hold, then all investors would choose the portfolio on the Capital Market Line that is tangent to the efficient frontier; this is called the tangent portfolio. The tangent portfolio is the market portfolio and it is the portfolio with the highest Sharpe Ratio. This means it provides the highest reward (expected return) per unit of risk (volatility).—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

0:05:45

0:05:45

The Capital Market Line

0:11:33

0:11:33

Capital Market Line (CML) vs Security Market Line (SML)

0:02:21

0:02:21

markowitz portfolio theory capital market line cfa-course.com

0:06:54

0:06:54

Capital Market Line

0:16:05

0:16:05

Efficient Frontier, Sharpe Ratio and Capital Market Line (CML)

0:08:01

0:08:01

Explaining the Capital Asset Pricing Model (CAPM) & Security Market Line (SML)

0:05:18

0:05:18

Capital Market Line definition for investment modeling

0:03:44

0:03:44

The Security Market Line

0:20:02

0:20:02

Is This the END of the Stock Market?

0:08:21

0:08:21

CFA Level I: Portfolio Management - CAL, CML, SML Explained

0:10:55

0:10:55

capital market line ( CML ) | security market line ( SML ) | capm model | portfolio management mcom

0:09:22

0:09:22

Capital Market Line Explained in Detail | With Graph | Equation of CML

0:05:20

0:05:20

CAPM - What is the Capital Asset Pricing Model

0:08:29

0:08:29

capital market line&Security Market Line

0:24:03

0:24:03

Capital market line explained: Tangency and CAPM derivation (Excel)

0:02:54

0:02:54

The efficient frontier

0:00:15

0:00:15

Capital Market Line

0:05:36

0:05:36

Capital Asset Pricing Model - Capital Market Line

0:04:01

0:04:01

Understanding Capital Market Line (CML) and How to Calculate It

0:05:23

0:05:23

Difference between Security Market line and Capital Market Line | Notes of CAPM

0:21:35

0:21:35

Evolution of Portfolio Theory – From Efficient Frontier to CAL to SML (For CFA® and FRM® Exams)

0:20:53

0:20:53

Capital market line Concept - CA Final AFM

0:08:47

0:08:47

Graph The Efficient Frontier And Capital Allocation Line In Excel

0:10:06

0:10:06

Video 26 - Capital Market Line

Комментарии