filmov

tv

Bond Valuation | Exam FM | Financial Mathematics Lesson 21 - JK Math

Показать описание

How to Value the Price of Bonds (Financial Mathematics Lesson 21)

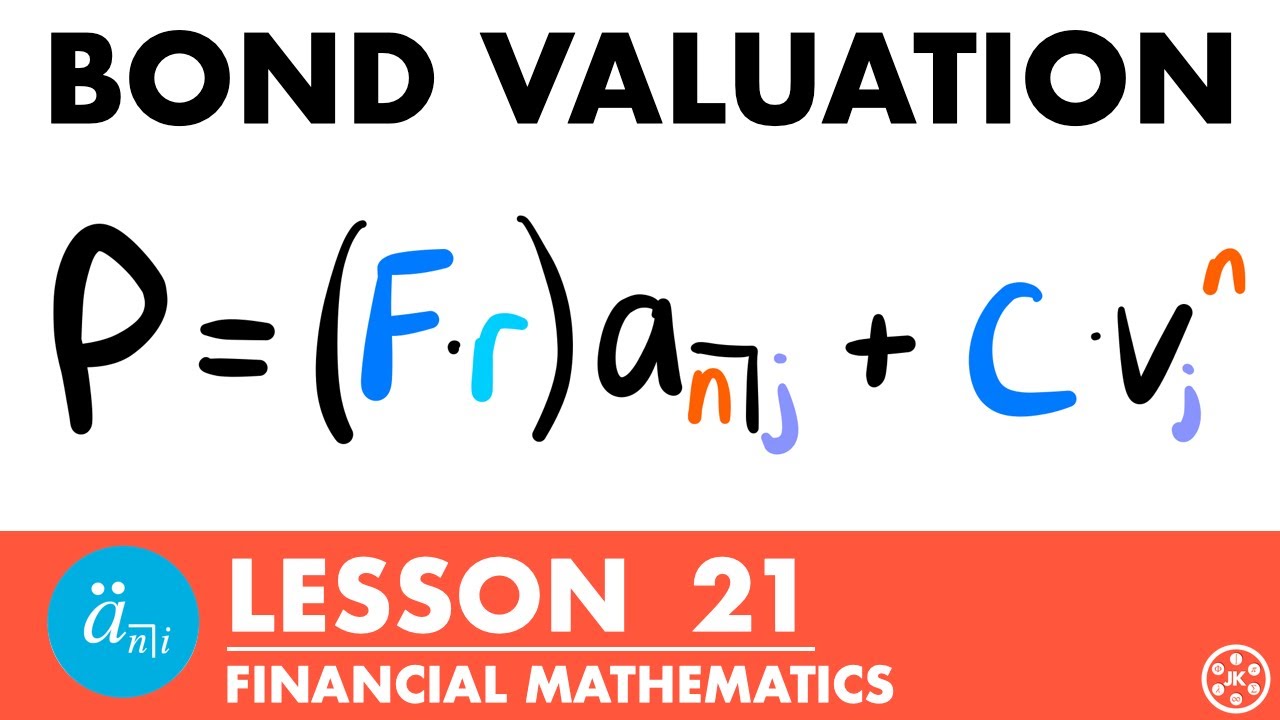

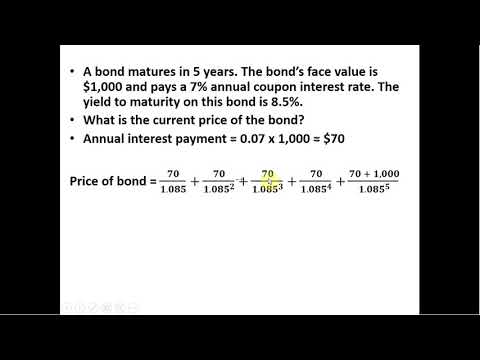

In this lesson we learn about bonds and how to calculate their price given its components of its face value, redemption value, coupon rate, and its yield rate. We discuss what each of these components are and their importance to the calculation of a bond’s price.

Bonds are similar to loans in that they are a way to borrow money. Essentially, a bond is a debt that typically requires periodic payments known as “coupons” for a stated term, as well as a one time payment of the amount borrowed at the end of the term issued. We use this definition of a bond to derive its price formula, which is the present value of the coupon payments plus the redemption value. We look at one example problem and discuss what it means to purchase a bond at either par value, at a discount, or at a premium.

This course is designed to help students understand the concepts of mathematics of investment and credit, as well as provide a starting point in preparation for the Actuarial Exam FM (Financial Mathematics).

Financial Mathematics requires a proficient understanding of Calculus concepts such as derivative and integration techniques. This implies that a solid understanding in various algebra skills, including manipulating equations, basic factoring methods, solving logarithmic equations, and more, are also required to fully comprehend and learn the concepts of the Financial Mathematics course.

Video Chapters:

0:00 What is a Bond?

0:49 Components of a Bond

5:02 Finding the Price Formula

8:51 Example Problem

15:48 Effects of Yield Rate & Coupon rate

18:32 Buying at Par, Discount, and Premium

⚡️Math Products I Recommend⚡️

⚡️Textbooks I Use⚡️

⚡️My Recording Equipment⚡️

(Commissions earned on qualifying purchases)

Find me on social media:

Instagram: @jk_mathematics

Found this video to be helpful? Consider giving this video a like and subscribing to the channel!

Thanks for watching! Any questions? Feedback? Leave a comment!

-Josh from JK Math

#math #finance #examfm

Disclaimer: Please note that some of the links associated with the videos on my channel may generate affiliate commissions on my behalf. As an amazon associate, I earn from qualifying purchases that you may make through such affiliate links.

In this lesson we learn about bonds and how to calculate their price given its components of its face value, redemption value, coupon rate, and its yield rate. We discuss what each of these components are and their importance to the calculation of a bond’s price.

Bonds are similar to loans in that they are a way to borrow money. Essentially, a bond is a debt that typically requires periodic payments known as “coupons” for a stated term, as well as a one time payment of the amount borrowed at the end of the term issued. We use this definition of a bond to derive its price formula, which is the present value of the coupon payments plus the redemption value. We look at one example problem and discuss what it means to purchase a bond at either par value, at a discount, or at a premium.

This course is designed to help students understand the concepts of mathematics of investment and credit, as well as provide a starting point in preparation for the Actuarial Exam FM (Financial Mathematics).

Financial Mathematics requires a proficient understanding of Calculus concepts such as derivative and integration techniques. This implies that a solid understanding in various algebra skills, including manipulating equations, basic factoring methods, solving logarithmic equations, and more, are also required to fully comprehend and learn the concepts of the Financial Mathematics course.

Video Chapters:

0:00 What is a Bond?

0:49 Components of a Bond

5:02 Finding the Price Formula

8:51 Example Problem

15:48 Effects of Yield Rate & Coupon rate

18:32 Buying at Par, Discount, and Premium

⚡️Math Products I Recommend⚡️

⚡️Textbooks I Use⚡️

⚡️My Recording Equipment⚡️

(Commissions earned on qualifying purchases)

Find me on social media:

Instagram: @jk_mathematics

Found this video to be helpful? Consider giving this video a like and subscribing to the channel!

Thanks for watching! Any questions? Feedback? Leave a comment!

-Josh from JK Math

#math #finance #examfm

Disclaimer: Please note that some of the links associated with the videos on my channel may generate affiliate commissions on my behalf. As an amazon associate, I earn from qualifying purchases that you may make through such affiliate links.

0:19:50

0:19:50

Bond Valuation | Exam FM | Financial Mathematics Lesson 21 - JK Math

1:39:50

1:39:50

Loan Repayment & Bond Valuation Unit Review | Exam FM | Financial Mathematics - JK Math

0:11:08

0:11:08

Bond Valuation - A Quick Review

0:19:48

0:19:48

Bond Valuation Examples | Exam FM | Financial Mathematics - JK Math

0:06:57

0:06:57

SOA/FM SAMPLE QUESTION #171

0:10:02

0:10:02

Basic Bond Facts (SOA Exam FM – Financial Mathematics – Module 3, Section 5)

0:06:44

0:06:44

SOA/FM SAMPLE QUESTION #117

0:06:02

0:06:02

SOA/FM SAMPLE QUESTION #57

0:09:25

0:09:25

Bond Pricing in CT 1 and Exam FM - Financial Mathematics

0:02:20

0:02:20

How to Calculate the Current Price of a Bond

0:14:47

0:14:47

Bond Valuation (Calculations for CFA® and FRM® Exams)

0:06:07

0:06:07

Actuarial Exam FM/2 Prep: Bond Redemption Value for a Given Price and Yield Rate

0:16:12

0:16:12

Unit 7.3-1 || Bond Valuation || How to calculate bond price?

0:03:39

0:03:39

SOA/FM SAMPLE QUESTION #10

0:18:24

0:18:24

Market Price of Bonds | Exam FM | Financial Mathematics Lesson 22 - JK Math

0:03:18

0:03:18

SOA/FM SAMPLE QUESTION #172

0:12:48

0:12:48

Bond Bought at Par Example (SOA Exam FM – Financial Mathematics – Module 3, Section 6, Part 3)

0:04:03

0:04:03

SOA/FM SAMPLE QUESTION #133

0:04:31

0:04:31

Actuarial Exam FM/2 Prep: Yield Rate for a Bond Investment with Reinvested Coupons

0:16:20

0:16:20

Price of Callable Bonds Examples | Exam FM | Financial Mathematics - JK Math

0:04:06

0:04:06

SOA/FM SAMPLE QUESTION #178

0:15:01

0:15:01

Actuarial Exam 2/FM Prep: Portfolio Value from Macaulay Duration of Bonds

0:06:35

0:06:35

Actuarial Exam 2/FM Prep: Base Amount Formula to Price a Bond from Doubling Term Fact

0:06:38

0:06:38

Actuarial Exam 2/FM Prep: Compare Makeham's and Basic Formula for Bond Prices

Комментарии