filmov

tv

Life Insurance Products Explained | Guaranteed Universal Life vs Whole Life vs Term Insurance

Показать описание

In this video I’m going to talk about life insurance products, how they work and who they are and are not suitable for. A basic overview of Life insurance is that it comes in two forms. Term Insurance or permanent insurance. Term insurance is designed to provide protection for a limited time period. Permanent insurance is designed to provide lifetime protection along with a savings or cash value component.

Term Insurance:

• The lowest cost life insurance protection for a specified amount of time and coverage

• Term is significantly cheaper than permanent insurance until the guaranteed level premium period ends

o Term conversion allows the insured to keep their health status from the term policy without having to retake a medical exam or show evidence of insurability

o Term conversion must be converted to a permanent product within the portfolio of the same insurance company. Some conversion choices are limited depending on the term policy or rules set by the insurance company

• No cash value

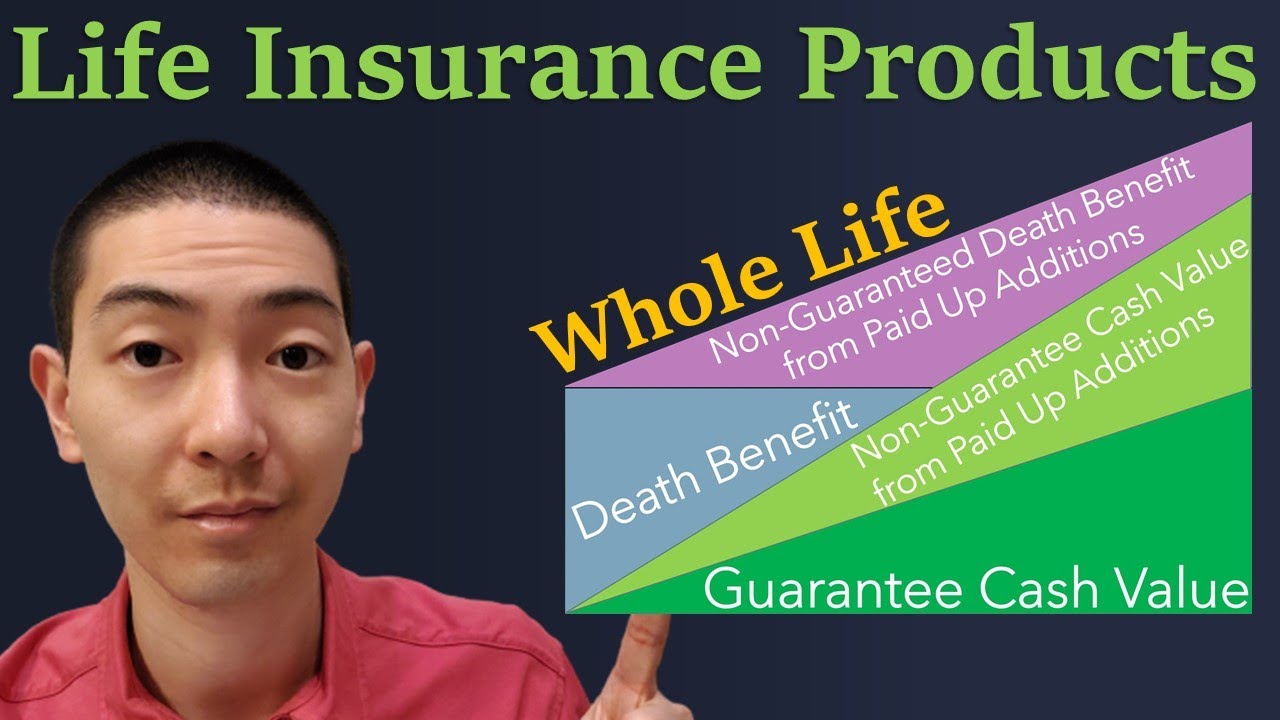

Whole Life Insurance:

• The highest cost life insurance protection, but offers guarantees under certain conditions

• Permanent life insurance that provides a guaranteed death benefit and builds cash value over time as long as premiums are paid on time and no loans or withdrawals are taken from the policy to impact cash value. Cash value is guaranteed to increase each year and will never decline in value due to market conditions.

• Paid up additions are additional whole life insurance coverage that is purchased with policy dividends instead of premiums paid into the policy.

• A whole life policy can be paid-up assuming that all premiums have been paid on time and there are no loans on the policy at the end of the payment period. If the policy is paid-up, it is guaranteed to remain in-force with no additional premiums due.

• Can earn policy dividends or additional interest which are not guaranteed. Dividends or additional interest are generally used to build additional cash value (paid-up additions). They can also be used to pay future premiums or be paid in cash to the policy owner

• Over time, especially when dividends or additional interest are untouched in the policy to grow, whole life insurance can build enough cash value to provide supplemental retirement income, fund education costs for children or left in the policy to increase the death benefit passed on to beneficiaries.

No Lapse Guarantee Universal Life Insurance:

• A medium cost for life insurance protection, but offers guarantees under certain conditions

• GUL is a Universal Life policy with a feature that can guarantee the policy’s death benefit, or other benefits like a long-term care rider or chronic illness rider regardless of if the policy’s cash value drops to 0 as long as certain premium requirements and payments are met. The duration of the guarantee period is determined at the time of purchase and may extend to a specific age or the policy’s maturity.

• The duration of the guarantee is correlated to premium payments being made on time and the structure of the premiums, but it has no correlation to the policy’s cash value or the crediting interest rate of the underlying universal life policy.

o Any changes to the payment structure, even a change from paying annually to monthly could impact the guarantee along with missing a payment or late payments. If severe enough, it could lapse the policy. Adjustments to the death benefit could impact the guarantee.

• A no-lapse guarantee can either be reinstated or a certain amount of it can be reinstated. It could be reinstated at a potentially significant increase in premium, depending on how quickly action is or is not taken.

• Can add on LTC Riders or Chronic Illness Riders to a GUL

• No cash value

• Often used for estate planning needs

• Request in-force illustrations on GUL policies from the insurance company at least annually to be aware of any potential impacts to what was purchased and to make sure the guarantee remains intact.

00:00 - Intro

00:44 - Term Life Insurance

07:03 - Whole Life

12:38 - Guaranteed Universal Life

15:50 - Summary

Disclaimer: This is not a sponsored video.

The ideas, contents and opinions presented in this video are for entertainment purposes only. Bryan does not give tax or investment advice. All information is being presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Bryan is not a Financial Advisor, Tax Advisor or CPA/Accountant. Only you are responsible for the financial decisions that YOU make.

Term Insurance:

• The lowest cost life insurance protection for a specified amount of time and coverage

• Term is significantly cheaper than permanent insurance until the guaranteed level premium period ends

o Term conversion allows the insured to keep their health status from the term policy without having to retake a medical exam or show evidence of insurability

o Term conversion must be converted to a permanent product within the portfolio of the same insurance company. Some conversion choices are limited depending on the term policy or rules set by the insurance company

• No cash value

Whole Life Insurance:

• The highest cost life insurance protection, but offers guarantees under certain conditions

• Permanent life insurance that provides a guaranteed death benefit and builds cash value over time as long as premiums are paid on time and no loans or withdrawals are taken from the policy to impact cash value. Cash value is guaranteed to increase each year and will never decline in value due to market conditions.

• Paid up additions are additional whole life insurance coverage that is purchased with policy dividends instead of premiums paid into the policy.

• A whole life policy can be paid-up assuming that all premiums have been paid on time and there are no loans on the policy at the end of the payment period. If the policy is paid-up, it is guaranteed to remain in-force with no additional premiums due.

• Can earn policy dividends or additional interest which are not guaranteed. Dividends or additional interest are generally used to build additional cash value (paid-up additions). They can also be used to pay future premiums or be paid in cash to the policy owner

• Over time, especially when dividends or additional interest are untouched in the policy to grow, whole life insurance can build enough cash value to provide supplemental retirement income, fund education costs for children or left in the policy to increase the death benefit passed on to beneficiaries.

No Lapse Guarantee Universal Life Insurance:

• A medium cost for life insurance protection, but offers guarantees under certain conditions

• GUL is a Universal Life policy with a feature that can guarantee the policy’s death benefit, or other benefits like a long-term care rider or chronic illness rider regardless of if the policy’s cash value drops to 0 as long as certain premium requirements and payments are met. The duration of the guarantee period is determined at the time of purchase and may extend to a specific age or the policy’s maturity.

• The duration of the guarantee is correlated to premium payments being made on time and the structure of the premiums, but it has no correlation to the policy’s cash value or the crediting interest rate of the underlying universal life policy.

o Any changes to the payment structure, even a change from paying annually to monthly could impact the guarantee along with missing a payment or late payments. If severe enough, it could lapse the policy. Adjustments to the death benefit could impact the guarantee.

• A no-lapse guarantee can either be reinstated or a certain amount of it can be reinstated. It could be reinstated at a potentially significant increase in premium, depending on how quickly action is or is not taken.

• Can add on LTC Riders or Chronic Illness Riders to a GUL

• No cash value

• Often used for estate planning needs

• Request in-force illustrations on GUL policies from the insurance company at least annually to be aware of any potential impacts to what was purchased and to make sure the guarantee remains intact.

00:00 - Intro

00:44 - Term Life Insurance

07:03 - Whole Life

12:38 - Guaranteed Universal Life

15:50 - Summary

Disclaimer: This is not a sponsored video.

The ideas, contents and opinions presented in this video are for entertainment purposes only. Bryan does not give tax or investment advice. All information is being presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Bryan is not a Financial Advisor, Tax Advisor or CPA/Accountant. Only you are responsible for the financial decisions that YOU make.

0:05:18

0:05:18

Types Of Life Insurance Explained

0:20:14

0:20:14

Different Types Of Life Insurance Explained | Term Life, Whole Life, Universal Life, Variable Life

0:03:36

0:03:36

How Does Life Insurance Work?

0:16:15

0:16:15

Term Vs. Whole Life Insurance (Life Insurance Explained)

0:36:14

0:36:14

Types Of Life Insurance Policies - Life Insurance Exam Prep

0:03:35

0:03:35

Types of Life Insurance Explained

0:01:01

0:01:01

Life Insurance Explained using a THIRD GRADE Drawing

0:10:54

0:10:54

How to use Whole Life Insurance to Get Rich (Become your own Bank)

0:00:30

0:00:30

What is Term Insurance | #shorts #terminsurance

0:01:00

0:01:00

Is life insurance a good investment?! #money #investing #investment #lifehack #cash #rich #wealthy

0:22:34

0:22:34

Life Insurance 101 (WATCH THIS BEFORE YOU BUY)

0:00:44

0:00:44

Warren Buffett: How Insurance works

0:02:37

0:02:37

Martin Lewis' Guide to Life Insurance - Different Types | This Morning

0:08:27

0:08:27

WHAT'S THE BEST TYPE OF LIFE INSURANCE?

0:09:04

0:09:04

Why Is Term Insurance Better Than Whole Life Insurance?

0:13:13

0:13:13

4 Life Insurance Policies Provisions, Options and Riders

0:02:02

0:02:02

What is Life Insurance?

0:29:59

0:29:59

Life Insurance study class TYPES OF INSURANCE

0:09:00

0:09:00

Understanding Whole Life Insurance for the Insurance Exam

0:11:15

0:11:15

Term Vs. Whole Life Insurance | The Best Option For The Sandwich Generation

0:09:01

0:09:01

Whole life Insurance Explained | Investment or Scam?

0:15:24

0:15:24

Life Insurance Policies - Different Types | Features | Premiums | How to buy? | ETMONEY

0:12:57

0:12:57

Is Life Insurance A Good Way To Invest Your Money

0:08:06

0:08:06

How To Use Whole Life Insurance To GET RICH (Become Your Own Bank) | Wealth Nation

Комментарии