filmov

tv

Whole life Insurance Explained | Investment or Scam?

Показать описание

Since the end of World War 2, whole life insurance was the most popular insurance product out there. Families using whole life insurance policies found financial stability and sufficient retirement funding when losing their loved ones. People even used whole life insurance as an investment method at that time since it would secure annual dividends.

Nonetheless, in 1982, the Tax Equity and Fiscal Responsibility Act (TEFRA) passed in the US was the biggest tax increase in U.S. history. This made people turn their attention to the stock market which accounted for inflation on an annual basis. For instance, the S&P 500 was adjusted for inflation with an amount of 14.76% in 1982 and 17.27% in 1983. Unlike the insurance companies which provided rather fluctuating interest rates that did not account for inflation.

Today, 59% of people living in the US pay for life insurance. It is seen as a contemporary investment tool that is protected from the potential collapse of the stock market. We will be discussing this a bit more later in this video and will run the numbers to measure the effectiveness of using whole life insurance as an investment tool.

Whole life insurance provides the insured party with some peace of mind when it comes to the continuity of their families' financial stability and overall well-being in exchange for level, regularly paid premium payments.

It spans over the entire lifetime of the insured party and does not have an expiry date.

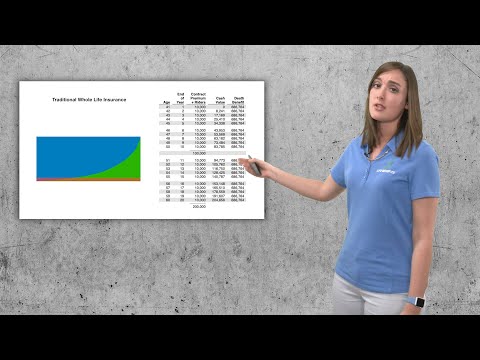

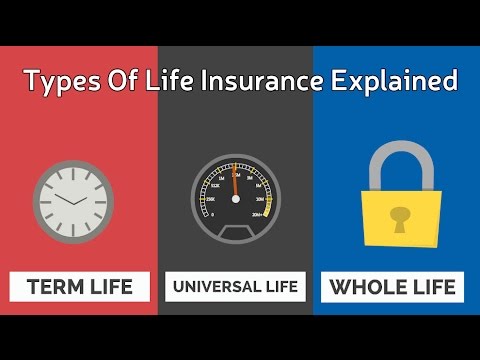

Whole life insurance is made of three components. These are premiums, death benefit, and cash value. So premiums are what you pay every month for whole life insurance. This is amount is flat and it does not change throughout the lifetime of the insured party in exchange for what is known as the death benefit. The death benefit is received by the insurance beneficiaries which are typically the family members of the insured party. Yes, it's called death benefit because the policy beneficiaries receive this amount when you are dead. For instance, this can amount to $500,000, or some people even opt-in for bigger amounts based on their financial capabilities.

When premiums paid into your whole life policy matches the death benefit, it is considered to have reached its maturity date. Typically, insurance companies design policies to mature when you turn 100, but some recent policies even extend the maturity date to age 120.

The third component is the cash value which is sometimes referred to as a living benefit. Part of the premiums you pay goes to building up the cash value which you receive dividends on. This is what makes whole life insurance different from other types of life insurance such as the term life. During the first 10 to 20 years of coverage, a whole life insurance policy's cash value is quite small, due to fees and the cost of coverage. The insured party should receive around 10% dividends on the cash value only but when deducting all the insurance companies administrative fees and commissions, the insured end up with dividends around 2.2% as reported by the consumer reports organization.

The cash value of your whole life insurance policy will not be taxed while it's growing. This is known as “tax deferred,” and it means that your money grows faster because it's not being reduced by taxes each year.

Nonetheless, the cash value can be accessed by the insured party in case of canceling or surrendering the policy and losing the death benefit. Many insurance policies feature a withdrawal clause that would allow the insured party to cancel the policy. A cheque will be given with the amount of the accumulated cash value.

The policyholders can also take a loan from this cash value without taxation instead of taking it from a bank which is known as Infinite Banking. It is not a loan from the cash value though.

Cash withdrawals are also considered an option to access the built-up cash value of the whole life insurance policy but are limited to the amount specified in the terms of the insurance policy. When exceeding the set amount, these cash withdrawals may end up reducing the death benefit that is received by the policy beneficiaries.

So, what do you think? Would you go for whole life insurance? Please let us know in the comments below.

------- Contents of This Video -------

00:00 - Introduction

00:54 - Whole Life Insurance History

01:20 - Tax Equity & Fiscal Responsibility Act (TEFRA)

02:10 - What is Whole Life Insurance?

02:44 - Whole Life Insurance Premiums

02:57 - Whole Life Insurance Death Benefit

03:36 - Whole Life Insurance Cash Value

04:05 - Investment and Dividends

04:51 - Withdrawal

05:09 - Loan and Interest Rate

05:57 - Example

06:37 - Scam / Rip off

07:25 - Family and Business

Websites:

Nonetheless, in 1982, the Tax Equity and Fiscal Responsibility Act (TEFRA) passed in the US was the biggest tax increase in U.S. history. This made people turn their attention to the stock market which accounted for inflation on an annual basis. For instance, the S&P 500 was adjusted for inflation with an amount of 14.76% in 1982 and 17.27% in 1983. Unlike the insurance companies which provided rather fluctuating interest rates that did not account for inflation.

Today, 59% of people living in the US pay for life insurance. It is seen as a contemporary investment tool that is protected from the potential collapse of the stock market. We will be discussing this a bit more later in this video and will run the numbers to measure the effectiveness of using whole life insurance as an investment tool.

Whole life insurance provides the insured party with some peace of mind when it comes to the continuity of their families' financial stability and overall well-being in exchange for level, regularly paid premium payments.

It spans over the entire lifetime of the insured party and does not have an expiry date.

Whole life insurance is made of three components. These are premiums, death benefit, and cash value. So premiums are what you pay every month for whole life insurance. This is amount is flat and it does not change throughout the lifetime of the insured party in exchange for what is known as the death benefit. The death benefit is received by the insurance beneficiaries which are typically the family members of the insured party. Yes, it's called death benefit because the policy beneficiaries receive this amount when you are dead. For instance, this can amount to $500,000, or some people even opt-in for bigger amounts based on their financial capabilities.

When premiums paid into your whole life policy matches the death benefit, it is considered to have reached its maturity date. Typically, insurance companies design policies to mature when you turn 100, but some recent policies even extend the maturity date to age 120.

The third component is the cash value which is sometimes referred to as a living benefit. Part of the premiums you pay goes to building up the cash value which you receive dividends on. This is what makes whole life insurance different from other types of life insurance such as the term life. During the first 10 to 20 years of coverage, a whole life insurance policy's cash value is quite small, due to fees and the cost of coverage. The insured party should receive around 10% dividends on the cash value only but when deducting all the insurance companies administrative fees and commissions, the insured end up with dividends around 2.2% as reported by the consumer reports organization.

The cash value of your whole life insurance policy will not be taxed while it's growing. This is known as “tax deferred,” and it means that your money grows faster because it's not being reduced by taxes each year.

Nonetheless, the cash value can be accessed by the insured party in case of canceling or surrendering the policy and losing the death benefit. Many insurance policies feature a withdrawal clause that would allow the insured party to cancel the policy. A cheque will be given with the amount of the accumulated cash value.

The policyholders can also take a loan from this cash value without taxation instead of taking it from a bank which is known as Infinite Banking. It is not a loan from the cash value though.

Cash withdrawals are also considered an option to access the built-up cash value of the whole life insurance policy but are limited to the amount specified in the terms of the insurance policy. When exceeding the set amount, these cash withdrawals may end up reducing the death benefit that is received by the policy beneficiaries.

So, what do you think? Would you go for whole life insurance? Please let us know in the comments below.

------- Contents of This Video -------

00:00 - Introduction

00:54 - Whole Life Insurance History

01:20 - Tax Equity & Fiscal Responsibility Act (TEFRA)

02:10 - What is Whole Life Insurance?

02:44 - Whole Life Insurance Premiums

02:57 - Whole Life Insurance Death Benefit

03:36 - Whole Life Insurance Cash Value

04:05 - Investment and Dividends

04:51 - Withdrawal

05:09 - Loan and Interest Rate

05:57 - Example

06:37 - Scam / Rip off

07:25 - Family and Business

Websites:

Whole life Insurance Explained | Investment or Scam?

0:16:15

0:16:15

Term Vs. Whole Life Insurance (Life Insurance Explained)

0:07:08

0:07:08

Is Whole Life Insurance Ever A Good Idea?

0:29:31

0:29:31

Whole Life Insurance Explained

0:10:54

0:10:54

How to use Whole Life Insurance to Get Rich (Become your own Bank)

0:09:23

0:09:23

Why Dave Ramsey HATES Whole Life Insurance!

0:08:06

0:08:06

How To Use Whole Life Insurance To GET RICH (Become Your Own Bank) | Wealth Nation

0:13:12

0:13:12

Learn The Basics of Whole Life Insurance in 12 Minutes

0:01:36

0:01:36

See if you qualify: IUL-Index Universal Life-Compound Interest -TFRA-Tax-Free Retirement Account

0:17:24

0:17:24

The TRUTH About Whole Life Insurance (What Salesman WON'T Tell You!) | Wealth Nation

0:11:23

0:11:23

The Whole Life Insurance Scam - What Salesmen Won't Tell You

0:11:15

0:11:15

Term Vs. Whole Life Insurance | The Best Option For The Sandwich Generation

0:11:35

0:11:35

Term vs Whole Life Insurance (Life Insurance Explained)

0:12:24

0:12:24

What Is Universal Life Vs. Whole Life?

0:00:57

0:00:57

Overfunding A Whole Life Insurance Policy

0:12:01

0:12:01

Whole Life Insurance Explained (Canada)

0:05:18

0:05:18

Types Of Life Insurance Explained

0:16:30

0:16:30

Term vs Whole Life Insurance Explained - Is it a SCAM?

0:25:17

0:25:17

Whole Life Insurance | The COMPLETE Guide

0:21:56

0:21:56

I was wrong about Whole Life Insurance...

0:09:00

0:09:00

Understanding Whole Life Insurance for the Insurance Exam

0:14:21

0:14:21

Life Insurance, Explained - Term Life Insurance vs Whole Life Insurance

0:07:51

0:07:51

Cash Out My Whole Life Policy?

0:20:32

0:20:32

Front Loaded Whole Life Insurance Explained

Комментарии