filmov

tv

Duration of Interest Rate Swap (FRM Part 1, Book 3, Financial Markets and Products)

Показать описание

0:11:54

0:11:54

Duration of Interest Rate Swap (FRM Part 1, Book 3, Financial Markets and Products)

0:03:51

0:03:51

Interest rate swap 1 | Finance & Capital Markets | Khan Academy

0:06:25

0:06:25

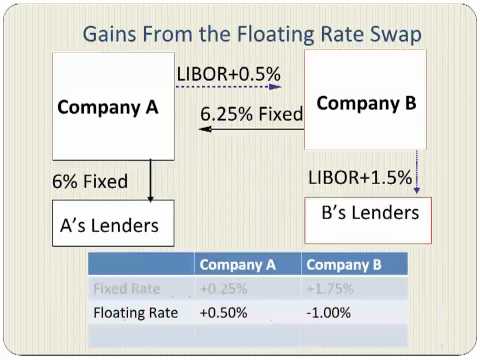

Interest Rate Swaps Explained | Example Calculation

0:14:54

0:14:54

What is a swap? - MoneyWeek Investment Tutorials

0:05:37

0:05:37

Bond Swaps

0:02:52

0:02:52

How swaps work - the basics

0:05:07

0:05:07

Bond Duration Explained Simply In 5 Minutes

0:15:31

0:15:31

Fixed Income 10 Duration fixed floating rate bonds 20210208

0:00:57

0:00:57

Rate Cuts this year #mortgage

0:19:54

0:19:54

Swap Spreads Are Making HUGE Moves Which Lead to...

0:08:42

0:08:42

Interest Rate Swaps With An Example

0:04:00

0:04:00

CFA Level 3 | Fixed Income: Derivatives Overlay with Interest Rate Swaps

0:58:05

0:58:05

FRM: You will never be scared of SWAPS after watching this!

0:02:50

0:02:50

Swaps Derivatives Explained in 3 Minutes 2024!

0:07:46

0:07:46

Free CFA Level 3 Lesson: Swap Duration and Pay vs. Receive

0:10:46

0:10:46

CORSO DERIVATI - Parte 14: Che cos'è l'Interest Rate Swap (IRS) e le tipologie di swaps

0:13:44

0:13:44

Key Rate Duration

0:08:51

0:08:51

Potential Interest Rate Swap use case in Cardano

0:13:16

0:13:16

CFA Level 2 | Derivatives: Interest Rate Options & Swaptions - Equivalences

0:02:48

0:02:48

Macro Minute -- Bond Prices and Interest Rates

0:00:50

0:00:50

What’s an interest rate swap in real estate? #shorts

0:00:56

0:00:56

Hedging Series: “Interest Rate Swap” [Chapter 5]

0:01:28

0:01:28

Interest Rate Swaps with Doug Carroll

0:00:26

0:00:26

What Are Swap Rates?

Комментарии