filmov

tv

Key Rate Duration

Показать описание

A short video on how to use Key Rate Duration to assess the price change for a bond (portfolio) with respect to interest rate changes.

0:04:38

0:04:38

Key Rate Duration & Key Rate Shifts Explained

0:02:14

0:02:14

What is Key Rate Duration? How to Calculate and Use it

0:13:44

0:13:44

Key Rate Duration

0:20:24

0:20:24

Making Sense of Key Rate Duration | CFA Level 1 and Level 2

2:48:30

2:48:30

CFA/FRM - Key Rate Duration

0:10:19

0:10:19

Key Rate Duration - Understanding Fixed Income Risk and Return - Fixed Income

0:05:33

0:05:33

Key Rate Duration

0:23:20

0:23:20

Key Rate Durations (FRM Part 1, Book 4, Valuation and Risk Models, Multi-Factor Risk Metrics)

0:11:31

0:11:31

Fed Rate Cuts Explained // Buy Bonds Now?

0:09:18

0:09:18

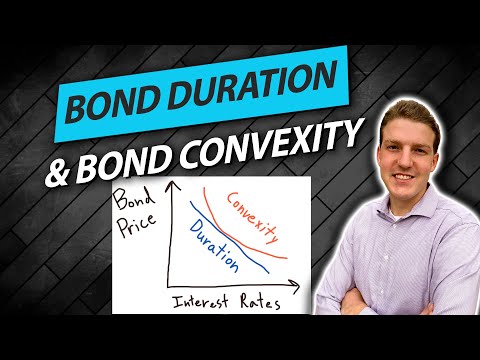

Bond Duration and Bond Convexity Explained

0:07:19

0:07:19

CFA Level 2 | Fixed Income: Par Bond and Maturity Matched Rate and Negative Key Rate Durations

0:30:28

0:30:28

Fixed Income: Key rate shift technique (FRM T4-43)

0:19:44

0:19:44

Fixed Income - Key Rate Duration (KRD)

0:12:27

0:12:27

Key Rate Duration: Macro (FICC Series)

0:05:07

0:05:07

Bond Duration Explained Simply In 5 Minutes

0:32:08

0:32:08

Lecture 22: Key Rate Duration

0:05:47

0:05:47

Understanding Key Rate Duration

0:15:38

0:15:38

Kaplanlearn Module 27 6 Key Rate Duration 2

0:29:45

0:29:45

Yield-Based Bond Convexity and Portfolio Properties (2024/25 CFA® Ll I Exam – Fixed Income – LM 12)...

0:11:03

0:11:03

Calculate Bond Convexity and Duration in Excel | Interest Rate Risk

![[CFA3] Module 13.3](https://i.ytimg.com/vi/WZo3P-wVQos/hqdefault.jpg) 0:34:01

0:34:01

[CFA3] Module 13.3 Yield Curve Volatility Strategies, Key Rate Duration

0:05:17

0:05:17

Why Bond Yields Are a Key Economic Barometer | WSJ

0:18:21

0:18:21

Introduction to Key Rate Shifts - Modelling non parallel term structures (FRM)

0:09:29

0:09:29

Key rate surations

Комментарии