filmov

tv

Все публикации

0:01:01

Understanding N(z) Vs N-Inverse(p) Vs N'(z) in Normal Distribution | FRM Part 1

0:01:00

Understanding the Vasicek Formula | FRM Part 1, FRM Part 2 | Valuation and Risk Models (Book 4)

0:00:59

FRM Part 2 | 8 Quick Tips for Tackling the Operational Risk Book (Book 3)

0:01:00

Exponential Variables are Memoryless | FRM Part 1 | Quantitative Analysis (Book 2)

0:01:00

Basis Risk | FRM Part 1 (Book 3, Financial Markets and Products)

0:15:04

Credit Valuation Adjustment (CVA) for a European Option | FRM Part 2 (Credit Risk) | Solved Example

0:13:38

Net Stable Funding Ratio (NSFR) Explained | FRM Part 2 | Liquidity Risk

0:11:37

Credit Value-at-Risk (VaR) | FRM Part 2 | Credit Risk

0:16:40

Positive Definite Correlation Matrices | FRM Part 1 (Quantitative Analysis)

0:23:05

Value at Risk (VaR) - Advantages & Disadvantages Explained | FRM Part 1 / FRM Part 2 | CFA Level 2

0:14:15

Expected Value and Variance of a Discrete Random Variable | FRM Part 1 | Quantitative Analysis

0:16:22

Index Credit Default Swaps Explained | FRM Part 2 | Credit Risk

0:15:29

Volatility Smile and Skew | FRM Part 2 | Market Risk

0:12:45

Overnight Index Swaps (OIS) Explained | Mechanics and Use (FRM Part 1)

0:05:49

Study Sequence for FRM Part 2 (2024)

0:20:38

Equity Swaps Explained: Pricing and Valuation | CFA Level 2

0:14:22

Liquidity Coverage Ratio (LCR) Explained | FRM Part 2 | Liquidity Risk | CFA Level 2

0:18:53

Bootstrapping | Bootstrap Resampling in Statistics | CFA Level 1 | FRM Part 1 | FRM Part 2

0:14:15

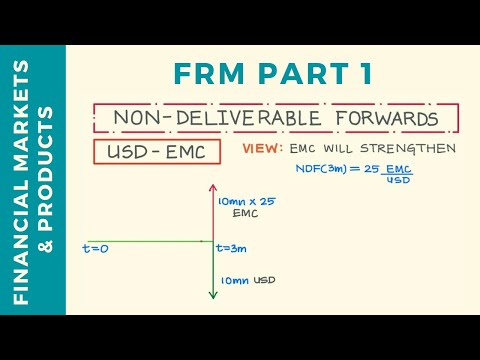

Non-Deliverable Forwards (NDFs) Explained | CFA Level 3

0:17:00

Equity Swaps Explained: Mechanics and Variations | FRM Part 1 | CFA Level 2

0:17:32

Moving Average (MA) Models | Time Series Analysis | FRM Part 1 | CFA Level 2

0:24:27

Credit Exposure Metrics (EFV, EE, PFE) for Interest Rate Swap | FRM Part 2

0:17:45

SOFR Futures Explained | FRM Part 1

0:15:44

Covered Vs Uncovered Interest Rate Parity | FRM Part 1 | CFA Level 2

Вперёд

0:01:01

0:01:01

0:01:00

0:01:00

0:00:59

0:00:59

0:01:00

0:01:00

0:01:00

0:01:00

0:15:04

0:15:04

0:13:38

0:13:38

0:11:37

0:11:37

0:16:40

0:16:40

0:23:05

0:23:05

0:14:15

0:14:15

0:16:22

0:16:22

0:15:29

0:15:29

0:12:45

0:12:45

0:05:49

0:05:49

0:20:38

0:20:38

0:14:22

0:14:22

0:18:53

0:18:53

0:14:15

0:14:15

0:17:00

0:17:00

0:17:32

0:17:32

0:24:27

0:24:27

0:17:45

0:17:45

0:15:44

0:15:44