filmov

tv

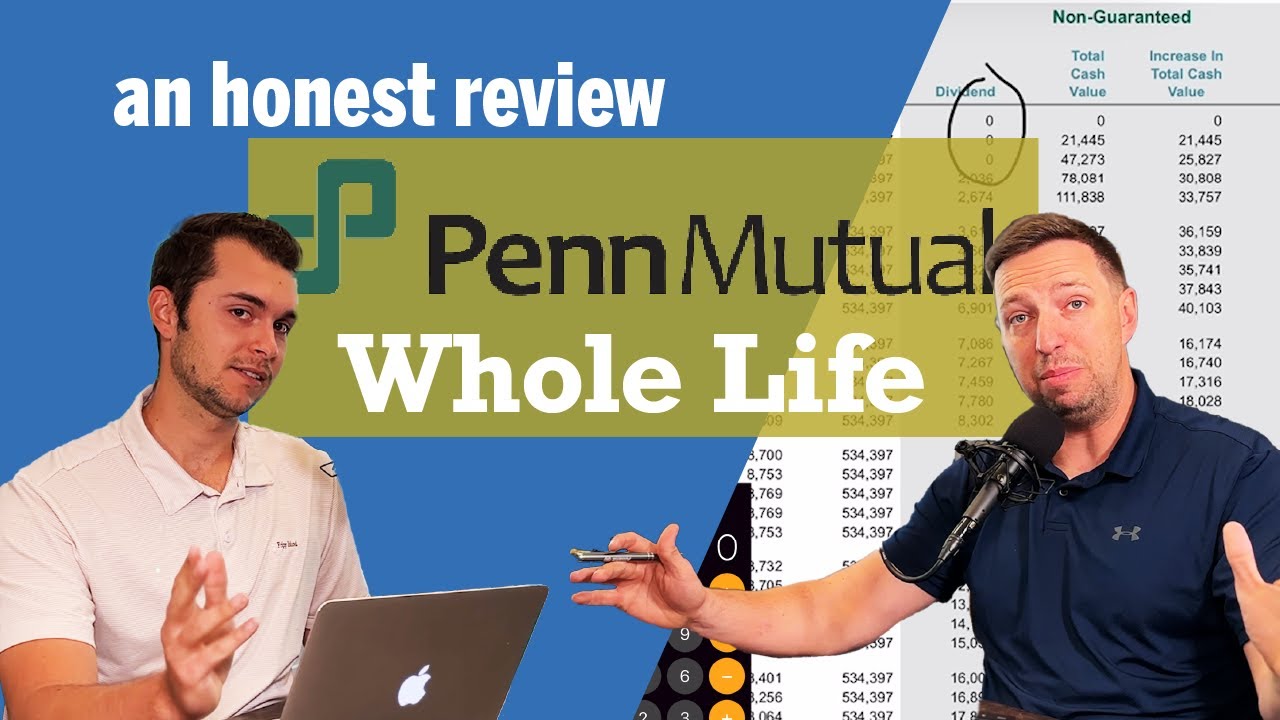

A Whole Life Insurance Review - Penn Mutual

Показать описание

We review IUL policies for over 700 people every year. This week we're looking at the Penn Mutual's Guaranteed Whole Life II. Let's look at the pros and cons of this policy and see if it's a good fit for you and your goals.

Book a Time to chat here:

OR

Send us your question here:

Already have a policy?

Send in your policy to be reviewed here:

Book a Time to chat here:

OR

Send us your question here:

Already have a policy?

Send in your policy to be reviewed here:

0:14:55

0:14:55

A Whole Life Insurance Review - Penn Mutual

0:07:08

0:07:08

Is Whole Life Insurance Ever A Good Idea?

0:21:56

0:21:56

I was wrong about Whole Life Insurance...

0:11:23

0:11:23

The Whole Life Insurance Scam - What Salesmen Won't Tell You

0:09:23

0:09:23

Why Dave Ramsey HATES Whole Life Insurance!

0:17:24

0:17:24

The TRUTH About Whole Life Insurance (What Salesman WON'T Tell You!) | Wealth Nation

0:16:15

0:16:15

Term Vs. Whole Life Insurance (Life Insurance Explained)

0:01:49

0:01:49

American Income Life Whole Life Insurance Review: A Good Choice?

0:12:33

0:12:33

Volvo EX30 Test Review - MotorMatters and CHANGECARS

0:11:15

0:11:15

Term Vs. Whole Life Insurance | The Best Option For The Sandwich Generation

0:10:54

0:10:54

How to use Whole Life Insurance to Get Rich (Become your own Bank)

0:03:45

0:03:45

I've Been Investing $1,000 A Month Into Whole Life Insurance

0:22:34

0:22:34

Life Insurance 101 (WATCH THIS BEFORE YOU BUY)

0:12:24

0:12:24

What Is Universal Life Vs. Whole Life?

0:12:57

0:12:57

Is Life Insurance A Good Way To Invest Your Money

0:04:44

0:04:44

When Does Whole Life Insurance Make Sense?

0:09:04

0:09:04

Why Is Term Insurance Better Than Whole Life Insurance?

0:05:38

0:05:38

Best Whole Life Insurance Companies in the USA! - insurance policy 2023

0:09:00

0:09:00

Understanding Whole Life Insurance for the Insurance Exam

0:08:06

0:08:06

How To Use Whole Life Insurance To GET RICH (Become Your Own Bank) | Wealth Nation

0:01:00

0:01:00

Is life insurance a good investment?! #money #investing #investment #lifehack #cash #rich #wealthy

0:09:47

0:09:47

Are There Any Situations Where Whole Life Insurance is a Good Idea?

0:09:32

0:09:32

Whole Life Insurance vs Indexed Universal Life which is better

0:04:32

0:04:32

Borrowing Against Your Life Insurance Policy : EXPLAINED!

Комментарии