filmov

tv

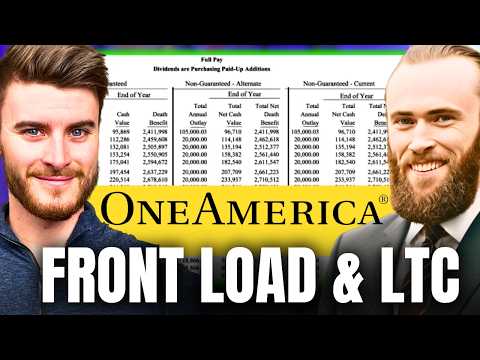

Front Loaded Whole Life Insurance Explained

Показать описание

This is my favorite strategy for entrepreneurs and investors who are sitting on capital and want all the benefits of life insurance without being obligated to large ongoing payments.

______________________________________________

=========================

*This video is for entertainment purposes only and is not financial or legal advice.

Financial Advice Disclaimer: All content on this channel is for education, discussion and illustrative purposes only and should not be construed as professional financial advice or recommendation. Should you need such advice, consult a licensed financial or tax advisor. No guarantee is given regarding the accuracy of information on this channel. Neither host or guests can be held responsible for any direct or incidental loss incurred by applying any of the information offered.

Affiliate Disclosure: Some of the links on this channel and in video descriptions are affiliate links. At no additional cost to you, we receive a commission if a purchase is made after clicking the link.

______________________________________________

=========================

*This video is for entertainment purposes only and is not financial or legal advice.

Financial Advice Disclaimer: All content on this channel is for education, discussion and illustrative purposes only and should not be construed as professional financial advice or recommendation. Should you need such advice, consult a licensed financial or tax advisor. No guarantee is given regarding the accuracy of information on this channel. Neither host or guests can be held responsible for any direct or incidental loss incurred by applying any of the information offered.

Affiliate Disclosure: Some of the links on this channel and in video descriptions are affiliate links. At no additional cost to you, we receive a commission if a purchase is made after clicking the link.

0:20:32

0:20:32

Front Loaded Whole Life Insurance Explained

0:17:58

0:17:58

Front Loading a Whole Life Policy — Examples From 30k to 1 MILLION!

0:17:39

0:17:39

How To Front load Your Whole Life Insurance Policy

0:15:30

0:15:30

Front Loading a Whole Life Policy — What is That?

0:17:34

0:17:34

Front Loading a Whole Life Policy — 50/Yr Male CASE STUDY

0:17:24

0:17:24

The TRUTH About Whole Life Insurance (What Salesman WON'T Tell You!) | Wealth Nation

0:00:30

0:00:30

The Smallest Front Loaded Whole Life Insurance Policy

0:09:03

0:09:03

Front Loading A Whole Life Policy For Maximum Cash Value | How it Works

0:00:00

0:00:00

Life Insurance Agent Reviews One America: Are They Worth Working With?

0:10:54

0:10:54

How to use Whole Life Insurance to Get Rich (Become your own Bank)

0:24:01

0:24:01

Front Loading a Whole Life Policy — Couple Who Want CASH Value!

0:08:03

0:08:03

Front Loading a Whole Life Policy — 50/Yr Old Wants to Know The Minimum

0:20:07

0:20:07

The Bugatti of Whole Life Insurance | The Front Load Policy Design

0:19:37

0:19:37

How To Design A Whole Life Policy for Maximum Cash Value Liquidity

0:07:24

0:07:24

Are There Benefits to a Front Load & Short Pay Design Life Insurance Policy?

0:09:23

0:09:23

Why Dave Ramsey HATES Whole Life Insurance!

0:22:09

0:22:09

The Best Whole Life Insurance Policy Design

0:08:06

0:08:06

How To Use Whole Life Insurance To GET RICH (Become Your Own Bank) | Wealth Nation

0:22:57

0:22:57

How The Wealthy Use Whole Life Insurance... For The Cash Value! | IBC Global

0:07:26

0:07:26

Keeping Life Insurance In A TRUST | GENERATIONAL WEALTH STRATEGY

0:33:12

0:33:12

How To Properly Structure A Whole Life Insurance Policy In 2023

0:05:29

0:05:29

Understanding Whole Life Insurance: Cash Value vs. Death Benefit Explained

0:15:07

0:15:07

How To Use Whole Life Insurance To Create CASH FLOW | Wealth Nation

0:00:25

0:00:25

FRONT LOADING AND OVER FUNDING WHOLE LIFE INSURANCE

Комментарии