filmov

tv

Understanding Whole Life Insurance: Cash Value vs. Death Benefit Explained

Показать описание

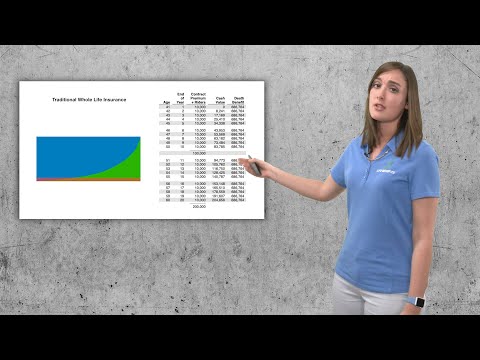

In this video, Tim and Olivia break down the intricate details of specially designed whole life insurance policies, shedding light on key aspects of living benefits and the death benefit. They clarify how these elements are intertwined in your insurance policy and what happens if there's a policy loan against your cash value at the time of your passing. Discover why you don't receive both the death benefit and cash value, and why it's essential to understand this concept when planning for your financial future.

Let us know what you think in the comments.

#Tier1Capital #WholeLifeInsurance #InfiniteBankingConcept #DeathBenefit #PolicyLoan

SUBSCRIBE FOR MORE FREE MONEY TIPS:

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

VISIT OUR WEBSITE:

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

CONNECT WITH US ON SOCIAL MEDIA:

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

DISCLAIMER

**Tier 1 Capital makes content available as a service to its customers and other visitors, to be used for informational purposes only. While our best intentions are to provide accurate and timely information, you should always consult with retirement, tax, and legal professionals prior to taking any action.

**The Infinite Banking Concept® is a registered trademark of Infinite Banking Concepts, LLC. Tier 1 Capital is not affiliated with, sponsored by, or endorsed by Infinite Banking Concepts, LLC.

Let us know what you think in the comments.

#Tier1Capital #WholeLifeInsurance #InfiniteBankingConcept #DeathBenefit #PolicyLoan

SUBSCRIBE FOR MORE FREE MONEY TIPS:

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

VISIT OUR WEBSITE:

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

CONNECT WITH US ON SOCIAL MEDIA:

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

DISCLAIMER

**Tier 1 Capital makes content available as a service to its customers and other visitors, to be used for informational purposes only. While our best intentions are to provide accurate and timely information, you should always consult with retirement, tax, and legal professionals prior to taking any action.

**The Infinite Banking Concept® is a registered trademark of Infinite Banking Concepts, LLC. Tier 1 Capital is not affiliated with, sponsored by, or endorsed by Infinite Banking Concepts, LLC.

0:10:54

0:10:54

How to use Whole Life Insurance to Get Rich (Become your own Bank)

0:08:06

0:08:06

How To Use Whole Life Insurance To GET RICH (Become Your Own Bank) | Wealth Nation

0:16:15

0:16:15

Term Vs. Whole Life Insurance (Life Insurance Explained)

0:09:01

0:09:01

Whole life Insurance Explained | Investment or Scam?

0:14:23

0:14:23

Understanding The Cash Value In A Whole Life Policy | IBC Global

0:11:23

0:11:23

The Whole Life Insurance Scam - What Salesmen Won't Tell You

0:17:24

0:17:24

The TRUTH About Whole Life Insurance (What Salesman WON'T Tell You!) | Wealth Nation

0:07:08

0:07:08

Is Whole Life Insurance Ever A Good Idea?

0:01:40

0:01:40

Should you get a whole life insurance policy? Are you extremely wealthy looking for a tax efficient

0:12:24

0:12:24

What Is Universal Life Vs. Whole Life?

0:18:40

0:18:40

How to Use Whole Life Insurance to Get Rich

0:21:56

0:21:56

I was wrong about Whole Life Insurance...

0:09:00

0:09:00

Understanding Whole Life Insurance for the Insurance Exam

0:12:57

0:12:57

Is Life Insurance A Good Way To Invest Your Money

0:22:57

0:22:57

How The Wealthy Use Whole Life Insurance... For The Cash Value! | IBC Global

0:04:28

0:04:28

What Exactly is the CASH VALUE in Your Life Insurance Policy?

0:09:07

0:09:07

Should You Use Cash Value Life Insurance as an Investment?

0:05:18

0:05:18

Types Of Life Insurance Explained

0:07:24

0:07:24

How Does Whole Life Insurance Work As An Investment?

0:14:18

0:14:18

Don't Borrow Against Your Whole Life Insurance Until Watching This Video

0:29:31

0:29:31

Whole Life Insurance Explained

0:18:36

0:18:36

This Is How Life Insurance Policy Loans Work

0:25:17

0:25:17

Whole Life Insurance | The COMPLETE Guide

0:20:14

0:20:14

Different Types Of Life Insurance Explained | Term Life, Whole Life, Universal Life, Variable Life

Комментарии