filmov

tv

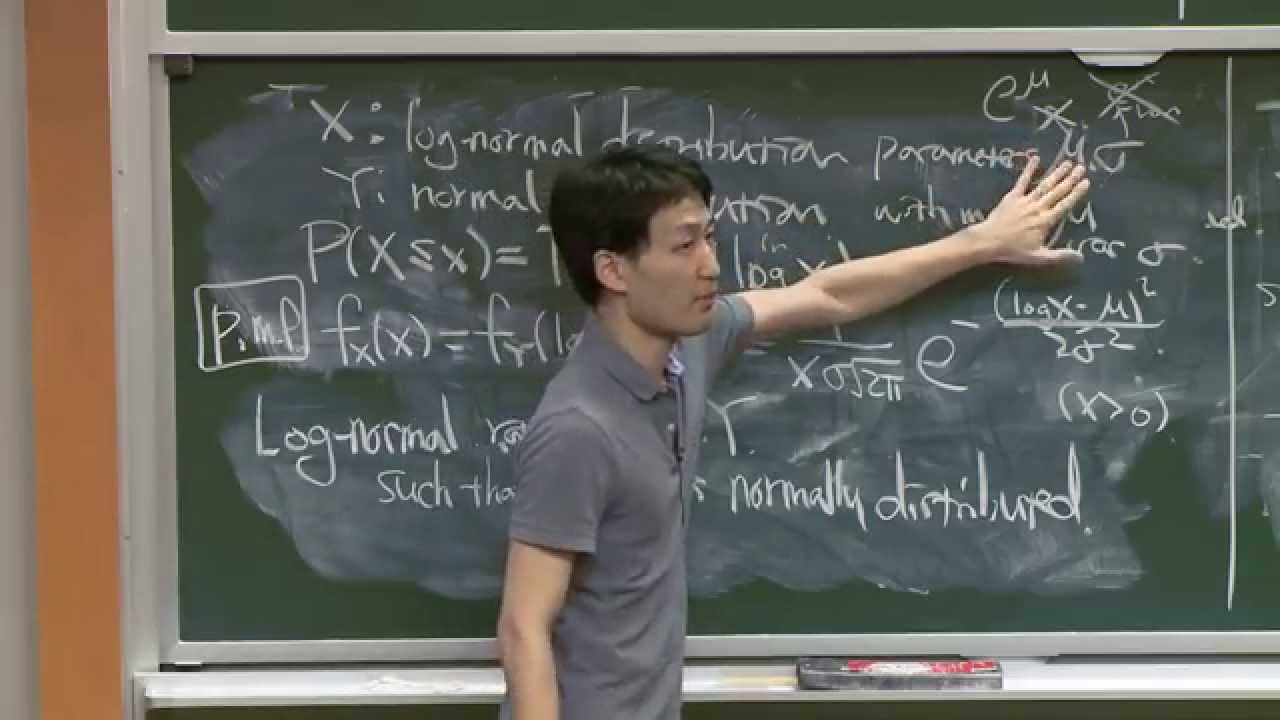

3. Probability Theory

Показать описание

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013

Instructor: Choongbum Lee

This lecture is a review of the probability theory needed for the course, including random variables, probability distributions, and the Central Limit Theorem.

*NOTE: Lecture 4 was not recorded.

License: Creative Commons BY-NC-SA

Instructor: Choongbum Lee

This lecture is a review of the probability theory needed for the course, including random variables, probability distributions, and the Central Limit Theorem.

*NOTE: Lecture 4 was not recorded.

License: Creative Commons BY-NC-SA

1:18:25

1:18:25

3. Probability Theory

0:11:27

0:11:27

Probability Theory 3 | Discrete vs. Continuous Case

0:16:59

0:16:59

Introduction to Probability, Basic Overview - Sample Space, & Tree Diagrams

0:11:28

0:11:28

Math Antics - Basic Probability

0:10:01

0:10:01

Why “probability of 0” does not mean “impossible” | Probabilities of probabilities, part 2

0:10:02

0:10:02

Multiplication & Addition Rule - Probability - Mutually Exclusive & Independent Events

0:05:48

0:05:48

Probability of Complementary Events & Sample Space

0:15:11

0:15:11

Bayes theorem, the geometry of changing beliefs

0:13:37

0:13:37

Master Linear Algebra & Probability for Machine Learning

0:12:34

0:12:34

Binomial distributions | Probabilities of probabilities, part 1

0:08:03

0:08:03

Bayes' Theorem EXPLAINED with Examples

0:31:15

0:31:15

But what is the Central Limit Theorem?

0:11:12

0:11:12

Probability Theory 3 | Discrete vs. Continuous Case [dark version]

0:07:11

0:07:11

3 game theory tactics, explained

0:19:01

0:19:01

Probability

0:08:18

0:08:18

Probability explained | Independent and dependent events | Probability and Statistics | Khan Academy

0:08:10

0:08:10

Types of Probability - Classical, Empirical, Subjective - Prob / Stat

0:06:13

0:06:13

Probability - Drawing Venn Diagrams

0:04:26

0:04:26

Experimental vs Theoretical Probability

0:03:13

0:03:13

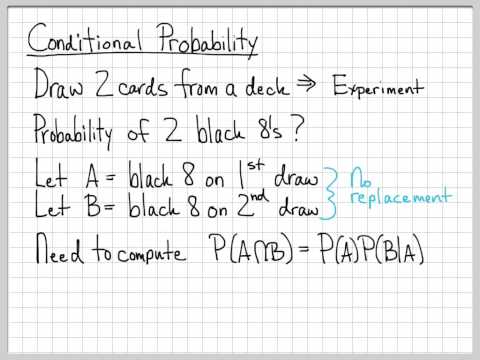

Fundamentals of Probability Theory (3/12): Conditional Probability Example

0:02:48

0:02:48

The Monty Hall Problem - Explained

0:02:44

0:02:44

Probability of Dice

0:18:26

0:18:26

3.1.3 Three Types of Probability (Classical-Theoretical, Empirical-Statistical & Subjective)

0:11:21

0:11:21

Basic Probability Part 1 Important Question Solution MBS, MBA, MPA, BBS, BBA Statistics Solution

Комментарии