filmov

tv

The Price/Value Feedback Loop: Revisiting AMC and GME!

Показать описание

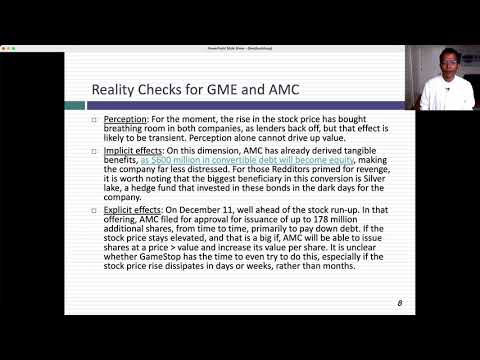

Value is driven by business models and fundamentals. Price is driven by mood and momentum. IN reasonably efficient market, they should converge, but what if they diverge? In this session, I look at how the price diverging from value (in either direction) can have a feedback effect on value. When a company's stock price soars past its value, the company benefits not just from perception, but also from fundamental changes that can occur to its business. Those changes can range from conversion of debt into equity and better employee retention (implicit) to new stock issuances at the higher price, to take advantage of the mis-pricing. Conversely, if a company's stock price drops below value, that not only negatively alters perception about the company, but it has fundamental consequences, increasing the debt load as a percent of value, and prompting employees to look for better places to work. For this company, buybacks can increase the value per share of the remaining shareholders. In this session, I look at the possibilities in both cases, and natural constraints on why they may not always deliver the results you expect them to deliver.

0:18:25

0:18:25

The Price/Value Feedback Loop: Revisiting AMC and GME!

0:11:25

0:11:25

The feedback loop of innovation | Patrick Scholl | TEDxTUDarmstadt

0:00:54

0:00:54

The Build Measure Learn Feedback Loop for Creating Real Value through Iteration #shorts

0:00:41

0:00:41

Growing your business faster with feedback loops.

0:00:47

0:00:47

Feedback loops in business.mp4

0:03:44

0:03:44

Feedback Loops - How to 100x your business

0:03:20

0:03:20

#WeBuildWednesdays 40: How to Use Feedback Loops in Your Marketing

0:05:53

0:05:53

Bombfell January 2017 Unboxing | Revisiting Service 2 years later

0:17:57

0:17:57

An Ode to Luck: Revisiting Tesla in January 2020

0:10:30

0:10:30

No Gold Standard? This instead? Irving Fisher's Chicago Plan Revisited

0:08:35

0:08:35

M8 4K Gamestick | Good Value for the Price

2:00:52

2:00:52

Karin Verelst: Science and Certainty Revisited

0:04:01

0:04:01

Implementing Feedback Loops

0:05:08

0:05:08

How To Use Feedback Loops To Increase Success

0:37:18

0:37:18

Positive feedback loops & building momentum: Triggering a game like obsession | Leon Angus

0:51:33

0:51:33

Rethinking Value During a Cost of Living Crisis - Global Webinar

0:42:52

0:42:52

'Revisiting the Case for Employee Participation in Corporate Governance' - Andreas Kokkini...

0:53:10

0:53:10

Xuviate eXpander Series - Episode 30. The Service-Delivery Review: The Missing Agile Feedback Loop

0:09:54

0:09:54

Revisiting the Bitcoin Supercycle

1:41:07

1:41:07

Seminar in Computer Architecture - S1: Revisiting RowHammer & MOESI-prime (Spring 2023)

0:05:38

0:05:38

iQOO 12 Revisited - The Misjudged Flagship!

0:36:45

0:36:45

Rich Harris - Rethinking reactivity

0:21:30

0:21:30

Uranium Stocks Revisited: Bannerman Resources

1:21:16

1:21:16

The Curse of Bigness Revisited | Tim Wu: Wesson Lecture 2018

Комментарии