filmov

tv

How to Calculate Beta using Covariance and Variance

Показать описание

This video shows how to calculate the beta of a stock using the covariance of the stock with the market index.

Beta is equal to:

(1) the covariance of a company's stock returns with the returns of the market index (e.g., the returns of the S&P 500)

divided by

(2) the variance of the returns of the market index.

Covariance / variance = beta

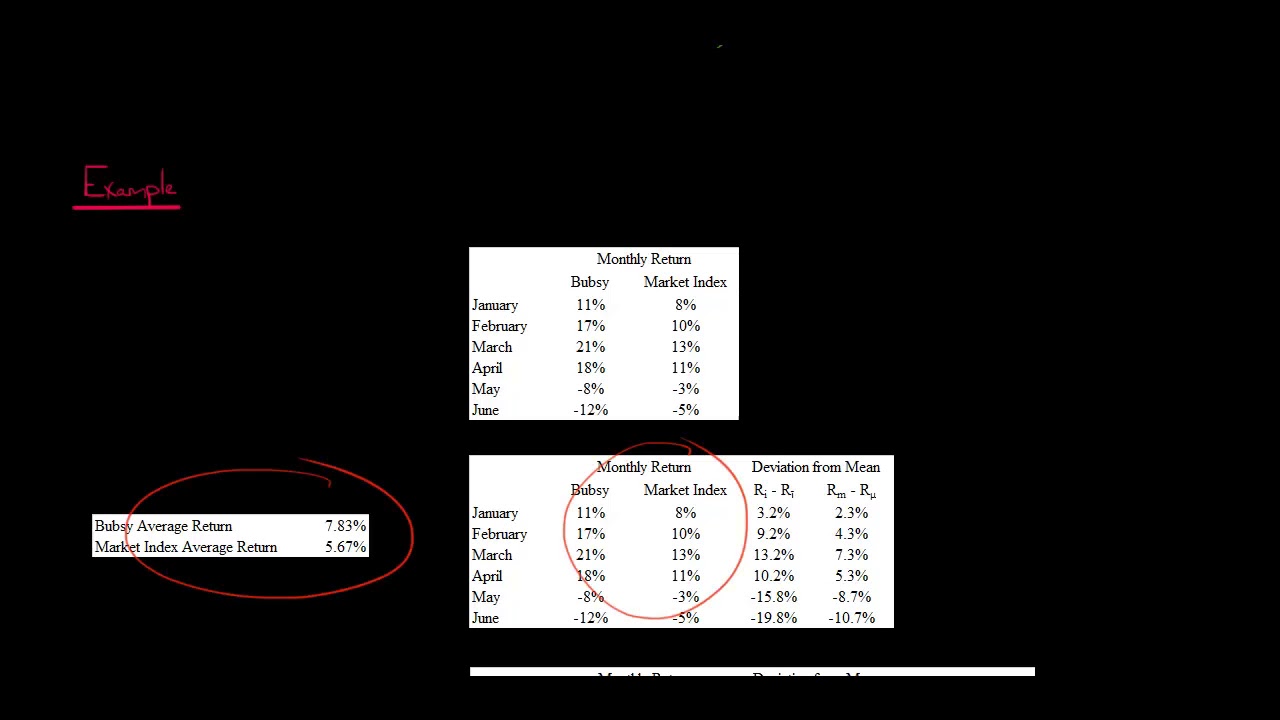

For example, if we are examining monthly stock returns for a company called Fluffy Love and the S&P 500 for the past five years, and we find that the covariance between the returns of Fluffy Love and the returns of the S&P 500 is 0.8, while the variance of the returns of the S&P 500 is 0.4, this means that Fluffy Love has a beta of 2.—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

Beta is equal to:

(1) the covariance of a company's stock returns with the returns of the market index (e.g., the returns of the S&P 500)

divided by

(2) the variance of the returns of the market index.

Covariance / variance = beta

For example, if we are examining monthly stock returns for a company called Fluffy Love and the S&P 500 for the past five years, and we find that the covariance between the returns of Fluffy Love and the returns of the S&P 500 is 0.8, while the variance of the returns of the S&P 500 is 0.4, this means that Fluffy Love has a beta of 2.—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

0:06:42

0:06:42

How To Calculate Beta on Excel - Linear Regression & Slope Tool

0:07:16

0:07:16

How to Calculate Beta using Covariance and Variance

0:05:08

0:05:08

How Does Beta Work? | Beta In Stocks Explained

0:04:01

0:04:01

Understanding Beta | Investopedia

0:04:57

0:04:57

How to Calculate Beta In Excel - All 3 Methods (Regression, Slope & Covariance)

0:04:11

0:04:11

ECONOMIST EXPLAINS: How To Calculate Beta Using Excel (Linear Regression & Slope Tool)

0:05:56

0:05:56

CAPM Beta Definition (Formula, Examples) CAPM Beta Calculation in Excel

0:02:43

0:02:43

How to Estimate the Beta of a Stock in Excel

1:00:21

1:00:21

#TaxmannWebinar | Terminal Value Calculation – Methods | Practical Application | Case Studies

0:16:46

0:16:46

How to Calculate Beta - formula in excel | CFA | FRM

0:09:24

0:09:24

How to Calculate Beta in Excel | Using Three Methods - Slope, Regression, Formula | By Dr. IOC

0:05:35

0:05:35

How to Calculate BETA on Excel - Slope Tool

0:07:54

0:07:54

How to Calculate Beta using Correlation and Volatility

0:08:41

0:08:41

Stock Beta Explained - Example With Excel

0:02:22

0:02:22

How to Calculate Beta on Bloomberg?

0:08:16

0:08:16

How to Calculate Beta

0:09:06

0:09:06

Calculating Stock Beta Using Python

0:11:58

0:11:58

Calculating beta using comparable firms: Pure play beta calculations

0:12:00

0:12:00

How To Calculate Stock Beta Using Excel - 2 Methods

0:02:16

0:02:16

CFA Level I - Calculation of Beta using STAT function of Texas Instruments BA II Calculator

![[Calculate Beta] -](https://i.ytimg.com/vi/tlciMKnL0M4/hqdefault.jpg) 0:12:25

0:12:25

[Calculate Beta] - How To Calculate Alpha And Beta

0:02:42

0:02:42

How to calculate beta in Excel

0:13:30

0:13:30

Easily Calculating Beta in Excel Using Regression

0:03:39

0:03:39

Py 90 Calculating the Beta of a Stock

Комментарии