filmov

tv

Easily Calculating Beta in Excel Using Regression

Показать описание

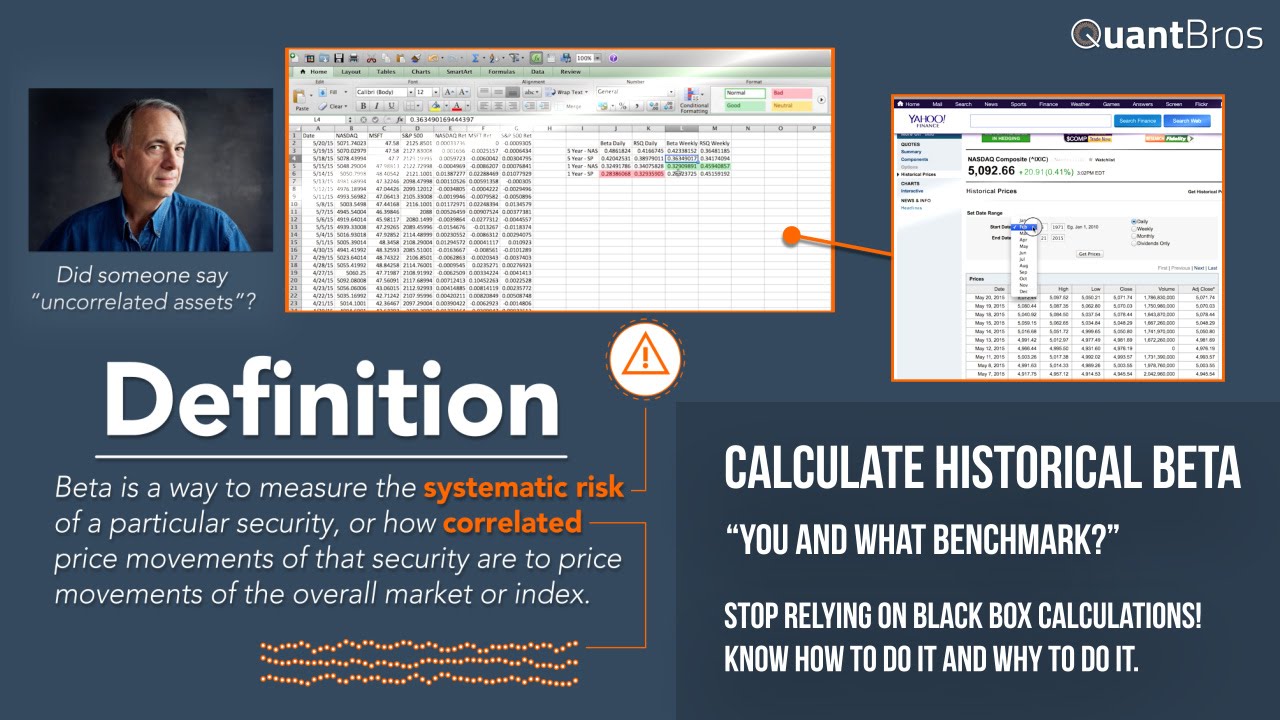

What is beta? Learn how and why to calculate historical beta for any security in Excel. We'll teach you how Yahoo Finance does it, too!

Not enough for you? Want to learn more R? Our friends over at DataCamp will whip you into shape real quick if you need help:

Or if you're more of a Python guy, we have an intro to finance for Python course live on DataCamp right now:

Not enough for you? Want to learn more R? Our friends over at DataCamp will whip you into shape real quick if you need help:

Or if you're more of a Python guy, we have an intro to finance for Python course live on DataCamp right now:

0:06:42

0:06:42

How To Calculate Beta on Excel - Linear Regression & Slope Tool

0:04:57

0:04:57

How to Calculate Beta In Excel - All 3 Methods (Regression, Slope & Covariance)

0:13:30

0:13:30

Easily Calculating Beta in Excel Using Regression

0:02:43

0:02:43

How to Estimate the Beta of a Stock in Excel

0:05:45

0:05:45

How to calculate Beta in Excel

0:04:34

0:04:34

Top three methods for calculating security's beta in excel

0:15:02

0:15:02

Calculating Beta in Excel

0:04:30

0:04:30

Calculating Beta using Excel

0:04:00

0:04:00

Calculate The Beta Of A Portfolio In Excel - The Excel Hub

0:14:13

0:14:13

Calculating beta in Excel / Analyzing stock returns / Episode 6

0:01:24

0:01:24

How Do You Calculate Beta In Excel?

0:11:24

0:11:24

Easily calculate Beta using historical stock data on Excel

0:03:40

0:03:40

How to calculate Beta Using Excel | Financial Statistics

0:14:30

0:14:30

Beta calculation in Excel – Tips and Tricks

0:00:07

0:00:07

Stock's beta in excel! 📉

0:05:35

0:05:35

How to Calculate BETA on Excel - Slope Tool

0:06:53

0:06:53

How To Calculate BETA Using Excel (Linear Regression)

0:12:00

0:12:00

How To Calculate Stock Beta Using Excel - 2 Methods

0:05:27

0:05:27

Three Ways to Calculate Beta in Excel

0:00:30

0:00:30

How to write beta symbol in excel

0:09:04

0:09:04

Estimate CAPM Beta in Excel

0:00:11

0:00:11

Add & Remove Border in Excel || Excel Tips & Tricks || @todfodeducation

0:10:08

0:10:08

Beta Interpretation and Calculation in Excel

0:03:34

0:03:34

How to calculate beta in excel

Комментарии