filmov

tv

Property Coverage vs. Liability Coverage | Home Insurance 101

Показать описание

If you have standard home insurance, then you likely have both property coverage and liability coverage. What are they, and how do they protect you when the unexpected happens? Dom from Jerry has the answers you're looking for.

------

------

-------

“I paid $205 for insurance with GEICO, and really was unhappy with them. I stayed with them so long because I couldn’t find it in me to go through the agony of comparing companies. The Penny Hoarder gave Jerry a great review and I am so happy I gave them a try!” — M. Swatt

“Jerry took care of everything, even canceling my old policy and getting me a refund!” — S.C.

“Saved $600 a year. Every 6 months Jerry automatically checks rates again.” — B.D.

“It has better pricing than going directly to the Insurance Company. I have used Jerry for two policies now.” — Dave M.

“I downloaded 3 insurance searching apps and Jerry was the best one by far. Easy. Accurate. Great customer service!” — Kyerra S.

-------

Personal property coverage and liability coverage are typical components of home insurance policies. While they cover different things, both coverage types prevent you from having to pay out of pocket should disaster strike.

Let’s go over personal property coverage first. Property encompasses what you own — things like your ...

— Clothes

— Furniture

— Appliances

— Artwork

— And dishes

Personal property coverage pays to fix or replace your belongings that are damaged or stolen in a covered loss.

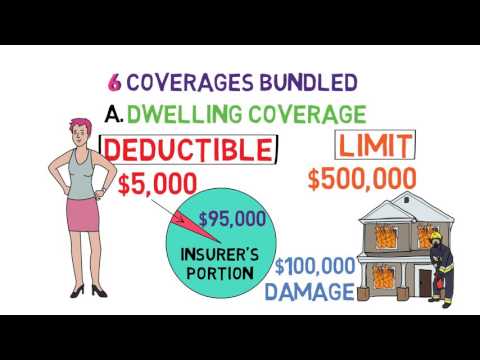

There are two types of personal property coverage: Actual cash value and replacement cost.

Actual cash value provides reimbursement based on the current value of your property by factoring in depreciation, which is the loss in value over time. This means your property often isn’t covered for its full purchase price.

In contrast, replacement cost provides more protection. It reimburses you the amount required to buy new items at the time of your claim, with no deduction for depreciation.

Now, let’s move on to liability coverage. It provides protection in the event that visitors are injured at your home unintentionally or through neglect. It covers the medical bills of injured visitors, as well as legal expenses resulting from lawsuits. Liability coverage can also cover the cost of damage you accidentally inflict on someone else's property.

Some examples of claims that are covered by liability insurance include:

— Dog bites

— Slips and falls

— Food poisoning

— And damage to a neighbor’s home

This coverage type usually protects anyone who’s considered a family member and lives in your home.

If you’re buying a new home insurance policy, consult an agent to choose the right coverage options and limits so you’re properly protected.

------

------

-------

“I paid $205 for insurance with GEICO, and really was unhappy with them. I stayed with them so long because I couldn’t find it in me to go through the agony of comparing companies. The Penny Hoarder gave Jerry a great review and I am so happy I gave them a try!” — M. Swatt

“Jerry took care of everything, even canceling my old policy and getting me a refund!” — S.C.

“Saved $600 a year. Every 6 months Jerry automatically checks rates again.” — B.D.

“It has better pricing than going directly to the Insurance Company. I have used Jerry for two policies now.” — Dave M.

“I downloaded 3 insurance searching apps and Jerry was the best one by far. Easy. Accurate. Great customer service!” — Kyerra S.

-------

Personal property coverage and liability coverage are typical components of home insurance policies. While they cover different things, both coverage types prevent you from having to pay out of pocket should disaster strike.

Let’s go over personal property coverage first. Property encompasses what you own — things like your ...

— Clothes

— Furniture

— Appliances

— Artwork

— And dishes

Personal property coverage pays to fix or replace your belongings that are damaged or stolen in a covered loss.

There are two types of personal property coverage: Actual cash value and replacement cost.

Actual cash value provides reimbursement based on the current value of your property by factoring in depreciation, which is the loss in value over time. This means your property often isn’t covered for its full purchase price.

In contrast, replacement cost provides more protection. It reimburses you the amount required to buy new items at the time of your claim, with no deduction for depreciation.

Now, let’s move on to liability coverage. It provides protection in the event that visitors are injured at your home unintentionally or through neglect. It covers the medical bills of injured visitors, as well as legal expenses resulting from lawsuits. Liability coverage can also cover the cost of damage you accidentally inflict on someone else's property.

Some examples of claims that are covered by liability insurance include:

— Dog bites

— Slips and falls

— Food poisoning

— And damage to a neighbor’s home

This coverage type usually protects anyone who’s considered a family member and lives in your home.

If you’re buying a new home insurance policy, consult an agent to choose the right coverage options and limits so you’re properly protected.

0:02:04

0:02:04

0:19:55

0:19:55

0:01:28

0:01:28

0:00:50

0:00:50

0:10:14

0:10:14

0:00:33

0:00:33

0:02:02

0:02:02

0:01:38

0:01:38

0:00:57

0:00:57

0:01:09

0:01:09

0:00:41

0:00:41

0:15:24

0:15:24

0:25:48

0:25:48

0:05:17

0:05:17

0:11:49

0:11:49

0:02:16

0:02:16

0:01:26

0:01:26

0:04:49

0:04:49

0:00:40

0:00:40

0:02:31

0:02:31

0:02:57

0:02:57

0:01:43

0:01:43

0:05:51

0:05:51

0:22:03

0:22:03