filmov

tv

All About Value at Risk(VaR) | FRM Part 1 2023| Historical Simulation, Delta Normal, Monte Carlo VaR

Показать описание

Hello candidates,

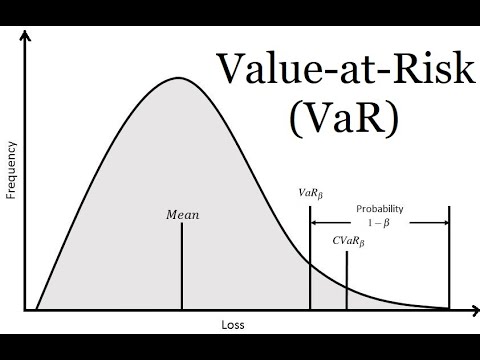

Welcome in All About Value at Risk(VaR) | FRM Part 1 2023| Historical Simulation, Delta Normal, Monte Carlo VaR.

In this video we are talking about all about value at risk which is important in FRM Part 1, 2023 curriculum. FRM is a difficult exam and here in this video, we will taking one concept of FRM Part 1 Exam, which is Value at Risk (VaR).

We have talked about the limitations and interpretations of value at risk. We are also talking about the historical simulation method. Delta normal method, and Monte Carlo approach to calculate the value at risk.

Please make sure to watch our other videos as well, and subscribe to our YouTube channel if you haven't subscribed yet.

Join our telegram channel as well.

Welcome in All About Value at Risk(VaR) | FRM Part 1 2023| Historical Simulation, Delta Normal, Monte Carlo VaR.

In this video we are talking about all about value at risk which is important in FRM Part 1, 2023 curriculum. FRM is a difficult exam and here in this video, we will taking one concept of FRM Part 1 Exam, which is Value at Risk (VaR).

We have talked about the limitations and interpretations of value at risk. We are also talking about the historical simulation method. Delta normal method, and Monte Carlo approach to calculate the value at risk.

Please make sure to watch our other videos as well, and subscribe to our YouTube channel if you haven't subscribed yet.

Join our telegram channel as well.

0:05:09

0:05:09

Value at Risk Explained in 5 Minutes

1:21:15

1:21:15

7. Value At Risk (VAR) Models

0:05:55

0:05:55

Value at Risk (VaR) Explained in 5 minutes

0:09:12

0:09:12

Value at Risk (VaR) Explained: A Comprehensive Overview

0:14:53

0:14:53

Value at Risk (VaR) Explained!

0:03:06

0:03:06

Value-at-Risk Explained

0:06:30

0:06:30

VaR (Value at Risk), explained

0:06:25

0:06:25

What is Value at Risk? VaR and Risk Management

0:25:51

0:25:51

How to Calculate Value at Risk VaR for an Investment Using Python

0:00:36

0:00:36

What is VaR (Value at Risk)? #frm #frmexam #VaR

0:02:53

0:02:53

Value at Risk (VaR): Monte Carlo Method Explained

0:05:01

0:05:01

Historical Method: Value at Risk (VaR) In Excel

0:12:53

0:12:53

Value at Risk (VAR) | Risk Management | CA Final SFM

0:06:54

0:06:54

Value at Risk - VaR (deutsch) - Berechnung und Formel für dein BWL-Studium

0:23:42

0:23:42

All About Value at Risk(VaR) | FRM Part 1 2023| Historical Simulation, Delta Normal, Monte Carlo VaR

0:03:12

0:03:12

Value at Risk (VaR) Demo

0:41:16

0:41:16

Value at Risk (VaR)

0:03:16

0:03:16

Evaluating Value-at-Risk (VaR)

0:09:36

0:09:36

How to Calculate Value at Risk (VaR) Using Excel || Value at Risk Explained

0:22:24

0:22:24

Value-at-risk (VaR) - variance-covariance and historical simulation methods (Excel) (SUB)

0:10:13

0:10:13

Monte Carlo Method: Value at Risk (VaR) In Excel

0:17:03

0:17:03

Value at Risk (VaR), Explanation and VaR Calculation Methods with Examples

0:00:24

0:00:24

Var - Value at Risk #var #marketrisk #riskmanagement #frm #frtb #creditrisk #ima #basel #finance

0:02:30

0:02:30

Il VaR - Value at Risk

Комментарии