filmov

tv

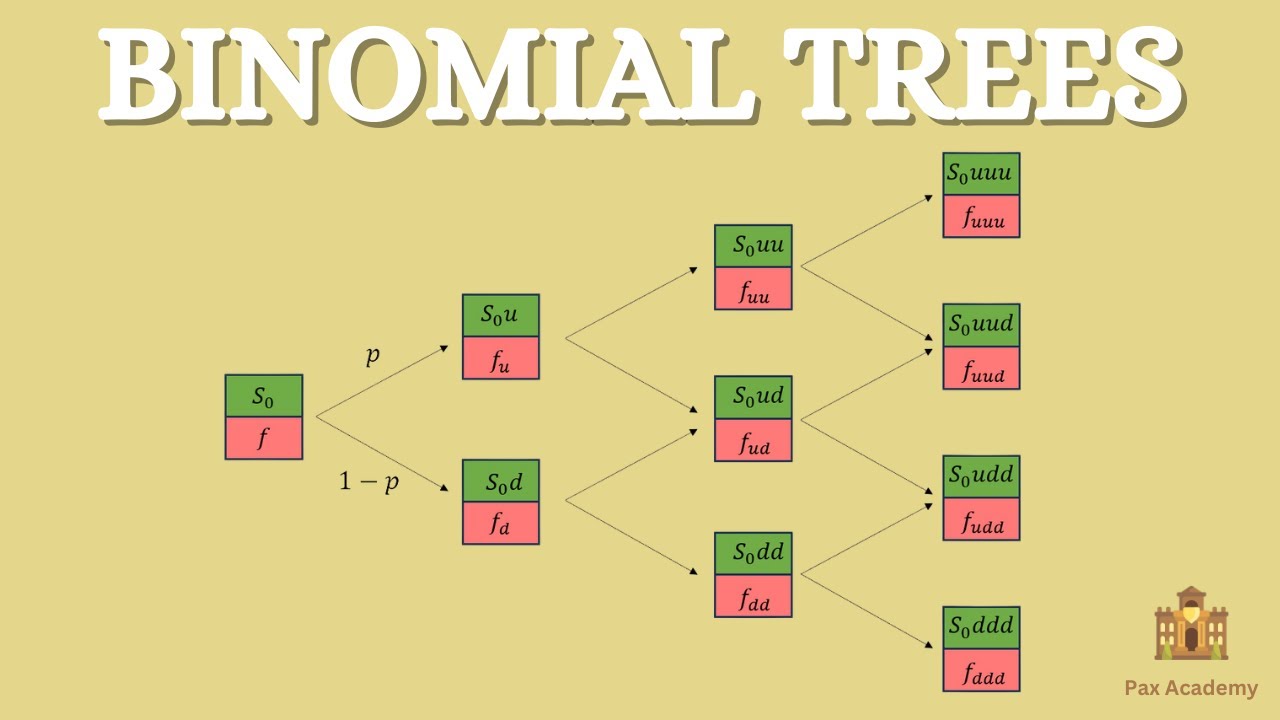

Binomial Tree (Three-Step) Simplified

Показать описание

In this video about the Binomial Option Pricing Model we solve a three-period binomial tree for a European call option. Here we don't go into detail about what a European option is, and we also simplify things by using the risk-free rate and assuming that the time periods are one year.

Let me know down in the comments if you succeeded in doing this exercise for a put option instead!

Let me know down in the comments if you succeeded in doing this exercise for a put option instead!

0:14:34

0:14:34

Binomial Tree (Three-Step) Simplified

0:16:51

0:16:51

Binomial Options Pricing Model Explained

0:18:53

0:18:53

American Put (Three) 3 Step | Binomial Method | European Price - EXAMPLE

0:11:48

0:11:48

Binomial Tree (Two-Step) Simplified

0:11:21

0:11:21

One-Step Binomial Tree made EASY

0:05:31

0:05:31

CFA Level I Derivatives - Binomial Model for Pricing Options

0:03:48

0:03:48

Logistic Regression in 3 Minutes

0:00:16

0:00:16

🤔How to simplify algebraic expressions??? Algebraic Expressions/Short Tricks #shorts #shortsfeed

0:08:21

0:08:21

Options pricing video 3 - Binomial method - Two-step - European put option price

0:00:23

0:00:23

Square Root Math Hack

0:00:34

0:00:34

Human Calculator Solves World’s Longest Math Problem #shorts

0:00:24

0:00:24

Isaac Newton's INSANE Sleep Habits 😬

0:00:20

0:00:20

1st yr. Vs Final yr. MBBS student 🔥🤯#shorts #neet

0:00:33

0:00:33

Can you find the 5th arrow? #shorts

0:00:40

0:00:40

Easy Way to Write Binary Numbers 1 to 15 #shorts

0:00:23

0:00:23

HOW CHINESE STUDENTS SO FAST IN SOLVING MATH OVER AMERICAN STUDENTS

0:00:12

0:00:12

IIT Bombay Lecture Hall | IIT Bombay Motivation | #shorts #ytshorts #iit

0:00:20

0:00:20

Bro’s hacking life 😭🤣

0:06:33

0:06:33

Two Step Binomial Tree - European Call

0:00:14

0:00:14

NEWYES Calculator VS Casio calculator

0:00:14

0:00:14

Salsa Night in IIT Bombay #shorts #salsa #dance #iit #iitbombay #motivation #trending #viral #jee

0:21:40

0:21:40

Binomial Option Pricing Model (Calculations for CFA® and FRM® Exams)

0:00:16

0:00:16

Addition Machine working model 6369550475

0:00:15

0:00:15

Trying transition video for the first time 💙😂 || #transformation #transition #shorts #viralvideo...

Комментарии