filmov

tv

Learn About Loan Amortization Using QuickBooks Enterprise

Показать описание

Talk to the QuickBooks Enterprise experts at Fourlane today. Get the best pricing, a tailored demo and QuickBooks consulting services.

Call brief

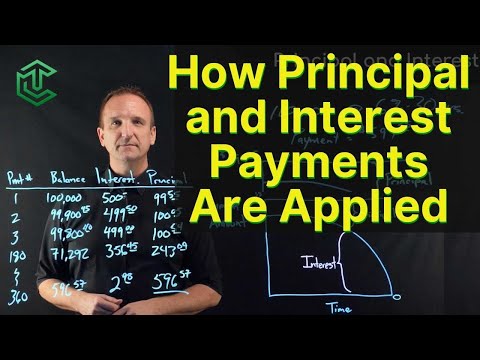

Kathryn from Fourlane discussed the importance of properly recording and reconciling loan transactions, including amortized loans, in QuickBooks. She demonstrated how to use online tools and Excel templates to create loan amortization schedules, allocate payments between principal and interest, and record the current and long-term portions of loan liabilities, emphasizing the need for accurate accounting to maintain a healthy balance sheet and cash flow management.

Key points

1. Loan amortization is the process of calculating and recording periodic loan payments that include both principal and interest.

2. Common mistakes include coding all loan payments to expense accounts, instead of separating principal and interest. This overstates expenses and understates net income.

3. Reconciling loan accounts monthly is important for accurate financial reporting. Loan statements or amortization schedules can be used for this.

5. When booking a new fixed asset loan, the purchase and loan should be recorded separately in the chart of accounts.

6. The "current portion of long-term debt" account is used to track the principal amount due in the current year. This is a journal entry made at the start of the year.

7. Ongoing loan payments should be split between principal and interest when recorded, rather than using a memorized transaction.

8. Attaching loan documentation to transactions is a best practice.

9. Reconciling loan accounts monthly is essential for accurate financial reporting.

10. These loan amortization principles apply to all types of loans, not just vehicle loans.

#QuickBooksTutorial #QuickBooksHelp #QuickBooksTraining #QuickBooksOnlineAdvanced #QuickBooksOnline #QuickBooksEnterprise #SmallBusiness #QuickBooksDesktop #QuickBooks #WomanOwned #Fourlane

Call brief

Kathryn from Fourlane discussed the importance of properly recording and reconciling loan transactions, including amortized loans, in QuickBooks. She demonstrated how to use online tools and Excel templates to create loan amortization schedules, allocate payments between principal and interest, and record the current and long-term portions of loan liabilities, emphasizing the need for accurate accounting to maintain a healthy balance sheet and cash flow management.

Key points

1. Loan amortization is the process of calculating and recording periodic loan payments that include both principal and interest.

2. Common mistakes include coding all loan payments to expense accounts, instead of separating principal and interest. This overstates expenses and understates net income.

3. Reconciling loan accounts monthly is important for accurate financial reporting. Loan statements or amortization schedules can be used for this.

5. When booking a new fixed asset loan, the purchase and loan should be recorded separately in the chart of accounts.

6. The "current portion of long-term debt" account is used to track the principal amount due in the current year. This is a journal entry made at the start of the year.

7. Ongoing loan payments should be split between principal and interest when recorded, rather than using a memorized transaction.

8. Attaching loan documentation to transactions is a best practice.

9. Reconciling loan accounts monthly is essential for accurate financial reporting.

10. These loan amortization principles apply to all types of loans, not just vehicle loans.

#QuickBooksTutorial #QuickBooksHelp #QuickBooksTraining #QuickBooksOnlineAdvanced #QuickBooksOnline #QuickBooksEnterprise #SmallBusiness #QuickBooksDesktop #QuickBooks #WomanOwned #Fourlane

0:02:14

0:02:14

0:05:19

0:05:19

0:03:35

0:03:35

0:05:21

0:05:21

0:11:01

0:11:01

0:29:49

0:29:49

0:03:56

0:03:56

0:22:11

0:22:11

0:07:14

0:07:14

0:03:49

0:03:49

0:06:45

0:06:45

0:03:50

0:03:50

0:04:50

0:04:50

0:05:10

0:05:10

0:15:45

0:15:45

0:18:11

0:18:11

0:07:31

0:07:31

0:12:42

0:12:42

0:05:12

0:05:12

0:04:46

0:04:46

0:08:04

0:08:04

0:00:36

0:00:36

0:00:13

0:00:13

0:01:00

0:01:00