filmov

tv

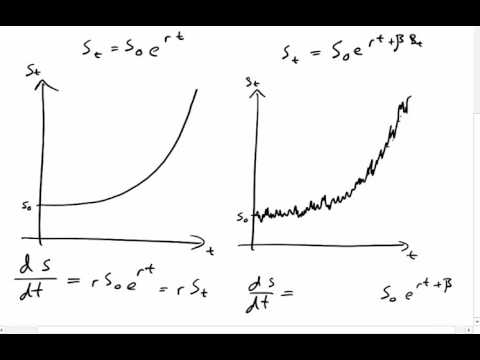

18. Itō Calculus

Показать описание

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013

Instructor: Choongbum Lee

This lecture explains the theory behind Itoíã calculus.

License: Creative Commons BY-NC-SA

Instructor: Choongbum Lee

This lecture explains the theory behind Itoíã calculus.

License: Creative Commons BY-NC-SA

1:18:03

1:18:03

18. Itō Calculus

0:22:20

0:22:20

Stochastic Calculus for Quants | Understanding Geometric Brownian Motion using Itô Calculus

0:01:58

0:01:58

Stochastic Calculus by Kamil Zajac

1:15:59

1:15:59

17. Stochastic Processes II

0:12:02

0:12:02

Outline of Stochastic Calculus

0:27:05

0:27:05

Ito Calculus-I

0:07:03

0:07:03

Introduction to Stochastic Calculus

0:16:24

0:16:24

Stochastic Calculus Simplified: Probability, Brownian Motion, and Ito Integrals - Part 1

1:17:41

1:17:41

5. Stochastic Processes I

0:56:05

0:56:05

21. Stochastic Differential Equations

0:28:38

0:28:38

Ito Calculus-II

0:24:44

0:24:44

Stochastic Calculus for Quants | Risk-Neutral Pricing for Derivatives | Option Pricing Explained

0:33:46

0:33:46

Ito Integral-I

0:19:05

0:19:05

Modifying the Ornstein-Uhlenbeck process | A practical application of stochastic calculus for Quants

0:01:50

0:01:50

Quiz 1: Stochastic Calculus

1:00:49

1:00:49

Introduction to Ito Calculus

0:22:35

0:22:35

Ito calculus part 2

1:07:07

1:07:07

Stochastic Calculus, lecture 18, part 1

0:25:43

0:25:43

Stochastic Calculus and Applications

0:20:38

0:20:38

Stochastic Calculus Simplified: Variation of Parameters

0:13:49

0:13:49

Ito calculus part 1

0:22:14

0:22:14

Itô calculus

0:27:50

0:27:50

Ito’s Integral: Why Riemann-Stieltjes approach does not work, and how does Ito’s approach work?

0:07:53

0:07:53

Statistics - Stochastic Calculus with Ito's Formula (Pre-part)

Комментарии