filmov

tv

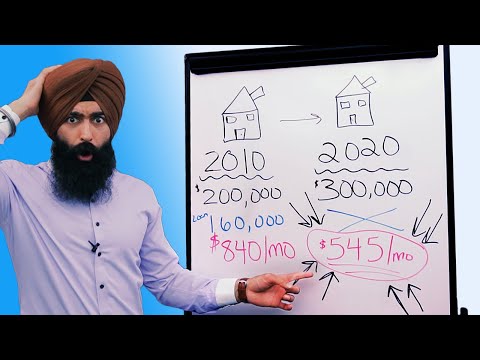

When Does Refinancing Your Mortgage Make Sense?

Показать описание

Explore More Shows from Ramsey Network:

Ramsey Solutions Privacy Policy

0:06:01

0:06:01

When Does Refinancing Your Mortgage Make Sense?

0:04:23

0:04:23

Mortgage 101: How to Refinance a Mortgage

0:13:51

0:13:51

Refinance 101 - Mortgage Refinance Explained

0:07:50

0:07:50

Property refinancing for beginners

0:03:07

0:03:07

When to refinance a mortgage

0:12:02

0:12:02

6 Times When Refinancing Makes Sense! When Should You Refinance Your Mortgage

0:04:45

0:04:45

When Does Refinancing Your Mortgage Make Sense?

0:04:35

0:04:35

When is it Worth Refinancing?

0:00:51

0:00:51

Looking to refinance your mortgage? 🏡❗Avoid these TOP 3 MISTAKES❗ #homefinancing #homefinance

0:03:13

0:03:13

Is Refinancing Your Mortgage Worth It?

0:13:40

0:13:40

Why You Should NOT WAIT To Refinance Your Mortgage - Refinance Home Mortgage

0:04:00

0:04:00

When Does Refinancing Make Sense?

0:02:27

0:02:27

Refinancing Explained: What to Know and Expect (Australia)

0:15:33

0:15:33

Mortgage Refinance Explained - When Should You REFINANCE?

0:12:55

0:12:55

Why You Should NOT Refinance Your Mortgage

0:04:36

0:04:36

Mortgage refinancing explained: What to know and when to do it

0:03:56

0:03:56

Is Refinancing a Mortgage 'Starting Over?'

0:06:44

0:06:44

When Does Refinancing Your Mortgage Make Sense?

0:13:02

0:13:02

Mortgage Refinance Explained - Refinance 101

0:08:08

0:08:08

REFINANCING BREAKDOWN Step-by-step guide | Property Investment UK

0:06:37

0:06:37

Is Refinancing Your Mortgage Worth It? Refinancing Your Home 101 🏠

0:01:40

0:01:40

Does Refinancing Your Mortgage Impact Your Credit Scores? | Intelligent Finance Guide

0:02:56

0:02:56

Why you should refinance your home loan 🏡

0:01:58

0:01:58

Paying extra on your mortgage VS refinancing

Комментарии