filmov

tv

Revenue recognition explained

Показать описание

Due to its size, revenue is the single most important line item in the income statement of most companies. The way companies decide whether a transaction does or doesn’t qualify as revenue is called revenue recognition.

⏱️TIMESTAMPS⏱️

00:00 Revenue recognition introduction

00:16 Revenue recognition accounting standards

00:33 Revenue recognition steps

01:35 Revenue recognition example

03:47 Revenue recognition for software

06:19 Revenue recognition for services

06:59 Revenue recognition for search advertising

The principles and rules for recognizing revenue are laid down in the new global revenue recognition standard, effective in 2018, which is ASC 606 in US GAAP, and IFRS 15 in IFRS, “Revenue from Contracts with Customers”.

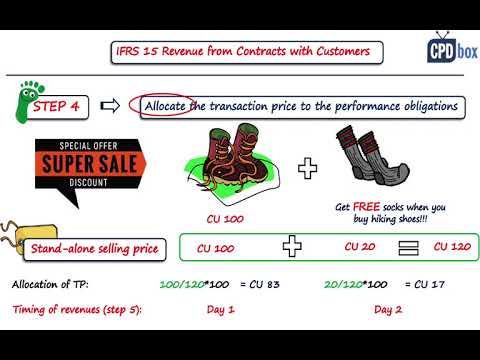

There is a five step approach for revenue recognition in both of these accounting standards. Step 1: identify the contract or contracts with the customer. Step 2: identify the performance obligations in the contract, in other words the promises to deliver goods or provide a service. Step 3: determine the transaction price. Step 4: link step two and step three by allocating the transaction price to the performance obligations. Step 5: recognize revenue when (or as) a performance obligation is satisfied. A performance obligation may be satisfied at a point in time (typically for promises to transfer goods to a customer) or over time (typically for promises to transfer services to a customer). That all sounds a bit cryptic, but fairly straightforward, right? Let’s review some revenue recognition examples to make revenue recognition come alive.

We will use revenue recognition in the financial statements of Microsoft as an example. You probably heard of Microsoft before, but might be surprised at just how many different types of products and services the company provides. For each of these products and services, Microsoft has to apply the revenue recognition accounting standard, and sometimes pass judgment as to how to apply the principles and rules. For example, regarding step 2, Microsoft remarks in the annual report “Our contracts with customers often include promises to transfer multiple products and services to a customer”. And regarding step 3: “Judgment is required to determine the stand-alone selling price for each distinct performance obligation.”

Let’s get a feeling for the size of the revenue at Microsoft, and then go through specific revenue recognition examples. In fiscal year 2019, Microsoft’s revenue was $126 billion. On top of that, Microsoft’s balance sheet holds $37 billion of unearned revenue, most of which is to be recognized in the upcoming quarters of the next financial year. Billing and payments for contracts often happens upfront, at the beginning of the contract period, while the revenue can only be recognized when the performance obligation is satisfied, hence the unearned revenue balance.

The description in Microsoft’s annual report of revenue recognition gives you the “when” and the “how much”. It starts off with the when: “revenue is recognized upon transfer of control of promised products or services to customers”. This links back to the term “performance obligation” that we just discussed: did you deliver the product, or perform the service. Then follows the how much: “In an amount that reflects the consideration we expect to receive in exchange for those products or services”, in other words: we book revenue for the amount we expect the customer to pay us. Let’s go through three specific examples of #revenuerecognition.

Philip de Vroe (The Finance Storyteller) aims to make #accounting, finance and investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

⏱️TIMESTAMPS⏱️

00:00 Revenue recognition introduction

00:16 Revenue recognition accounting standards

00:33 Revenue recognition steps

01:35 Revenue recognition example

03:47 Revenue recognition for software

06:19 Revenue recognition for services

06:59 Revenue recognition for search advertising

The principles and rules for recognizing revenue are laid down in the new global revenue recognition standard, effective in 2018, which is ASC 606 in US GAAP, and IFRS 15 in IFRS, “Revenue from Contracts with Customers”.

There is a five step approach for revenue recognition in both of these accounting standards. Step 1: identify the contract or contracts with the customer. Step 2: identify the performance obligations in the contract, in other words the promises to deliver goods or provide a service. Step 3: determine the transaction price. Step 4: link step two and step three by allocating the transaction price to the performance obligations. Step 5: recognize revenue when (or as) a performance obligation is satisfied. A performance obligation may be satisfied at a point in time (typically for promises to transfer goods to a customer) or over time (typically for promises to transfer services to a customer). That all sounds a bit cryptic, but fairly straightforward, right? Let’s review some revenue recognition examples to make revenue recognition come alive.

We will use revenue recognition in the financial statements of Microsoft as an example. You probably heard of Microsoft before, but might be surprised at just how many different types of products and services the company provides. For each of these products and services, Microsoft has to apply the revenue recognition accounting standard, and sometimes pass judgment as to how to apply the principles and rules. For example, regarding step 2, Microsoft remarks in the annual report “Our contracts with customers often include promises to transfer multiple products and services to a customer”. And regarding step 3: “Judgment is required to determine the stand-alone selling price for each distinct performance obligation.”

Let’s get a feeling for the size of the revenue at Microsoft, and then go through specific revenue recognition examples. In fiscal year 2019, Microsoft’s revenue was $126 billion. On top of that, Microsoft’s balance sheet holds $37 billion of unearned revenue, most of which is to be recognized in the upcoming quarters of the next financial year. Billing and payments for contracts often happens upfront, at the beginning of the contract period, while the revenue can only be recognized when the performance obligation is satisfied, hence the unearned revenue balance.

The description in Microsoft’s annual report of revenue recognition gives you the “when” and the “how much”. It starts off with the when: “revenue is recognized upon transfer of control of promised products or services to customers”. This links back to the term “performance obligation” that we just discussed: did you deliver the product, or perform the service. Then follows the how much: “In an amount that reflects the consideration we expect to receive in exchange for those products or services”, in other words: we book revenue for the amount we expect the customer to pay us. Let’s go through three specific examples of #revenuerecognition.

Philip de Vroe (The Finance Storyteller) aims to make #accounting, finance and investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

0:02:48

0:02:48

Revenue Recognition Principle in TWO MINUTES!

0:07:54

0:07:54

Revenue recognition explained

0:04:09

0:04:09

Financial Accounting 101: Revenue Recognition Principle - Accrual Accounting Basis

0:09:57

0:09:57

Revenue Recognition ASC 606 Explained via Example

0:08:39

0:08:39

CPA Explains Revenue Recognition Under GAAP Rule | With Examples

0:10:03

0:10:03

5-step Model for Revenue Recognition under IFRS 15 + Example + Journal entries

0:18:24

0:18:24

IFRS 15 Revenue from Contracts with Customers summary - applies in 2024

0:02:44

0:02:44

The fundamentals of IFRS 15

0:10:25

0:10:25

Deferred Revenue Explained | Adjusting Entries

0:04:34

0:04:34

Accrued revenue vs deferred revenue

0:02:25

0:02:25

Revenue recognition explained

0:02:31

0:02:31

Revenue Recognition Concept

0:07:21

0:07:21

Mastering IFRS 15: The 5-Step Model for Revenue Recognition Explained with Examples

0:09:29

0:09:29

Accrued Revenue MADE EASY | Adjusting Entries

0:02:35

0:02:35

ASC 606 Simplified: Understanding Revenue Recognition in 3 Minutes

0:23:05

0:23:05

IFRS 15 | Revenue Recognition| Revenue From Contract with Customers | IFRS Lectures

0:02:14

0:02:14

What is Revenue? - Financial Accounting

0:00:46

0:00:46

Revenue Recognition Definition

0:01:08

0:01:08

What is Revenue? - By Saheb Academy

0:08:49

0:08:49

Introduction to the New Revenue Recognition Standards

0:11:03

0:11:03

ASC 606 Overview - Revenue Recognition

0:01:51

0:01:51

Revenue Recognition

0:15:55

0:15:55

IFRS 15 Revenue Recognition - ACCA Financial Accounting (FA)

0:11:00

0:11:00

Cash vs Accrual Accounting Explained With A Story

Комментарии