filmov

tv

Accrued revenue vs deferred revenue

Показать описание

Accrued revenue versus deferred revenue, also known as unbilled revenue versus unearned revenue. What are the similarities between accrued revenue and deferred revenue, and what are the differences?

To start off with, both terms contain the word revenue. One of the Big Questions in accounting is whether the delivery of goods or services has occurred, or in more technical revenue recognition terms, whether the performance obligations in the contract have been met. There’s not always a full match between the invoicing to customers in the accounting period and the revenue booked in the general ledger in the accounting period. That’s the first similarity between accrued revenue and deferred revenue, we’ll get into lots more detail on that.

Another similarity is that accrued revenue and deferred revenue are both balance sheet accounts. Accrued revenue is an asset, something that we as a company own, it goes on the left hand side of the balance sheet. Deferred revenue is a liability, it is something that we as a company owe, it goes on the right hand side of the balance sheet.

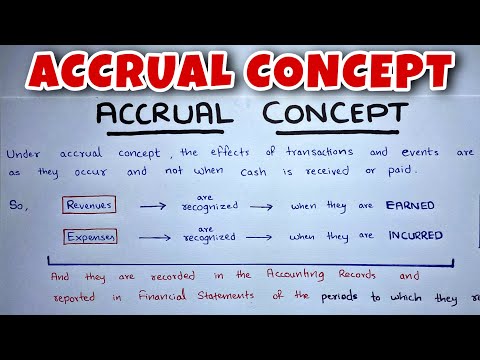

In addition, both accrued revenue and deferred revenue are #adjustingentries . Adjusting entries are accounting journal entries that convert a company's accounting records to the accrual basis of accounting.

We are basically dealing with the same subject matter, but approaching it from different directions. Accrued revenue is booked so we don’t understate revenue for the period. Deferred revenue is booked so we don’t overstate revenue for the period. Accrued revenue is sometimes called unbilled revenue, while deferred revenue is sometimes called unearned revenue. Let’s review accrued revenue and then deferred revenue in more detail.

The definition of #accruedrevenue is : revenue earned for goods or services delivered but not billed to the customer yet. An example is a service company that repairs and services heating systems in buildings, that works with timesheets. These timesheets are signed by the client for work performed in December, but the invoicing system for December is already closed, so we will record an accrued revenue journal entry directly into the general ledger to make sure we capture the revenue in the right period.

⏱️TIMESTAMPS⏱️

0:00 Introduction to accrued revenue and deferred revenue

1:17 Unbilled revenue vs unearned revenue

1:47 Accrued revenue definition and journal entries

2:56 Deferred revenue definition and journal entries

Here are the journal entries for accrued revenue. Step one is the adjusting entry at period-end. Debit accrued revenue on the balance sheet, credit revenue in the income statement. Step two is to issue the invoice in the new accounting period. Debit accounts receivable on the balance sheet, credit accrued revenue on the balance sheet. This brings the balance of the accrued revenue account on the balance sheet back to zero, it is cleared out. Step three is for the customer to pay the invoice. Debit cash, credit accounts receivable.

Deferred revenue deals with the exact opposite situation. The definition of deferred revenue is: the obligation to deliver goods or perform services in the future for which billing has already occurred and/or cash has been received. Deferred revenue is a liability, because if you fail to provide those goods or services in the future, you will have to pay the money back. An example of deferred revenue is an upfront payment by a customer for a gym membership, insurance, or a service contract, each of which could cover several months or even years. From the customer’s perspective, this is a prepaid expense. From the company’s perspective, this is treated as deferred revenue. The customer pays the full amount of the contract upfront: debit cash on the assets side of the balance sheet, credit deferred revenue on the liability side of the balance sheet. For each of the subsequent accounting periods, you determine how much of the upfront payment relates to that specific period, and record a debit to deferred revenue on the balance sheet and a credit to revenue in the income statement. At the end of the contract, the sum of the debits and the credits in the deferred revenue account should be equal, it is cleared out.

Philip de Vroe (The Finance Storyteller) aims to make accounting, finance and investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

To start off with, both terms contain the word revenue. One of the Big Questions in accounting is whether the delivery of goods or services has occurred, or in more technical revenue recognition terms, whether the performance obligations in the contract have been met. There’s not always a full match between the invoicing to customers in the accounting period and the revenue booked in the general ledger in the accounting period. That’s the first similarity between accrued revenue and deferred revenue, we’ll get into lots more detail on that.

Another similarity is that accrued revenue and deferred revenue are both balance sheet accounts. Accrued revenue is an asset, something that we as a company own, it goes on the left hand side of the balance sheet. Deferred revenue is a liability, it is something that we as a company owe, it goes on the right hand side of the balance sheet.

In addition, both accrued revenue and deferred revenue are #adjustingentries . Adjusting entries are accounting journal entries that convert a company's accounting records to the accrual basis of accounting.

We are basically dealing with the same subject matter, but approaching it from different directions. Accrued revenue is booked so we don’t understate revenue for the period. Deferred revenue is booked so we don’t overstate revenue for the period. Accrued revenue is sometimes called unbilled revenue, while deferred revenue is sometimes called unearned revenue. Let’s review accrued revenue and then deferred revenue in more detail.

The definition of #accruedrevenue is : revenue earned for goods or services delivered but not billed to the customer yet. An example is a service company that repairs and services heating systems in buildings, that works with timesheets. These timesheets are signed by the client for work performed in December, but the invoicing system for December is already closed, so we will record an accrued revenue journal entry directly into the general ledger to make sure we capture the revenue in the right period.

⏱️TIMESTAMPS⏱️

0:00 Introduction to accrued revenue and deferred revenue

1:17 Unbilled revenue vs unearned revenue

1:47 Accrued revenue definition and journal entries

2:56 Deferred revenue definition and journal entries

Here are the journal entries for accrued revenue. Step one is the adjusting entry at period-end. Debit accrued revenue on the balance sheet, credit revenue in the income statement. Step two is to issue the invoice in the new accounting period. Debit accounts receivable on the balance sheet, credit accrued revenue on the balance sheet. This brings the balance of the accrued revenue account on the balance sheet back to zero, it is cleared out. Step three is for the customer to pay the invoice. Debit cash, credit accounts receivable.

Deferred revenue deals with the exact opposite situation. The definition of deferred revenue is: the obligation to deliver goods or perform services in the future for which billing has already occurred and/or cash has been received. Deferred revenue is a liability, because if you fail to provide those goods or services in the future, you will have to pay the money back. An example of deferred revenue is an upfront payment by a customer for a gym membership, insurance, or a service contract, each of which could cover several months or even years. From the customer’s perspective, this is a prepaid expense. From the company’s perspective, this is treated as deferred revenue. The customer pays the full amount of the contract upfront: debit cash on the assets side of the balance sheet, credit deferred revenue on the liability side of the balance sheet. For each of the subsequent accounting periods, you determine how much of the upfront payment relates to that specific period, and record a debit to deferred revenue on the balance sheet and a credit to revenue in the income statement. At the end of the contract, the sum of the debits and the credits in the deferred revenue account should be equal, it is cleared out.

Philip de Vroe (The Finance Storyteller) aims to make accounting, finance and investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

0:04:34

0:04:34

Accrued revenue vs deferred revenue

0:07:31

0:07:31

Accrued Revenue vs Deferred Revenue

0:03:26

0:03:26

Financial Accounting 101: Accruals and Deferrals - Accrual Accounting - Made Easy

0:10:25

0:10:25

Deferred Revenue Explained | Adjusting Entries

0:09:29

0:09:29

Accrued Revenue MADE EASY | Adjusting Entries

0:16:02

0:16:02

Deferrals & Accruals | Deferred Revenue, Deferred Expense, Accrued Revenue & Accrued Expense

0:08:27

0:08:27

Deferred Revenue VS Accrued Revenue (How to Set Your SaaS Company Up for Success)

0:04:20

0:04:20

ACCRUED Revenue vs DEFERRED Revenue in Filipino

0:02:48

0:02:48

Revenue Recognition Principle in TWO MINUTES!

0:43:40

0:43:40

Deferred Income - Adjusting Entry - By Saheb Academy

0:10:01

0:10:01

Deferred Revenue Expenditure EXPLAINED - By Saheb Academy

0:05:55

0:05:55

Deferred Income and Accrued Income (AAT, ICB, ACCA, ACA, CIMA, IAB)

0:06:26

0:06:26

Accrual Concept EXPLAINED - By Saheb Academy

0:07:26

0:07:26

Accruals and Deferrals Concepts Examples and Top 10 Interview Questions | CorporateWala | Accenture

0:09:15

0:09:15

Chapter 3, Part 4 - Adjustments for Deferred Revenue & Accrued Revenue

0:01:40

0:01:40

What is Unbilled revenue and Deferred revenue(unearned revenue) #charteredaccountant #accounting

0:14:18

0:14:18

Deferred Revenue Expenditure | Basic Accounting Term | Meaning and Concept | Important Concept

0:09:57

0:09:57

Prepayments and Accruals | Adjusting Entries

0:09:00

0:09:00

Accruals explained

0:00:58

0:00:58

How well do you know Adjusting Entries?

0:08:24

0:08:24

Deferral and Accruals

0:12:55

0:12:55

Accrued Expenses Broken Down | Adjusting Entries

0:00:17

0:00:17

Deferred revenue vs Accrued Revenue #accounting #quiztime #accountingmadeeasy #financialaccounting

0:04:21

0:04:21

How to Record Adjusting Entries for Accrued Expenses and Accrued Revenue

Комментарии