filmov

tv

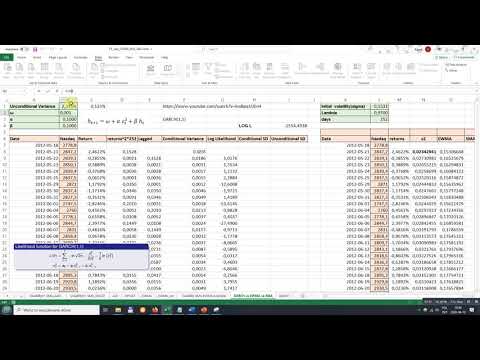

GARCH Modelling for Volatility in Eviews

Показать описание

This video provides some useful guides on how to generate the volatility series using the GARCH model framework.

For a better understanding of GARCH modelling, kindly refer to the following texts:

Campbell, et al (1996)

Chan (2010)

#garch #volatility #arch #bitcoin #btc

@ChekwubeMadichie @CrunchEconometrix @sayedhossain23 @harvard @mitocw @cambridgeuniversity @RuhrUniversitatBochum

For a better understanding of GARCH modelling, kindly refer to the following texts:

Campbell, et al (1996)

Chan (2010)

#garch #volatility #arch #bitcoin #btc

@ChekwubeMadichie @CrunchEconometrix @sayedhossain23 @harvard @mitocw @cambridgeuniversity @RuhrUniversitatBochum

0:11:34

0:11:34

GARCH Modelling for Volatility in Eviews

0:05:10

0:05:10

What are ARCH & GARCH Models

0:06:32

0:06:32

GARCH Volatility Model

0:07:26

0:07:26

Stock Forecasting with GARCH : Stock Trading Basics

0:10:25

0:10:25

GARCH Model : Time Series Talk

0:10:28

0:10:28

Volatility Modeling using GARCH Model

1:12:17

1:12:17

Volatility Modeling using GARCH Model

0:06:23

0:06:23

Time Varying Volatility and GARCH in Risk Management

0:22:22

0:22:22

GARCH model - volatility persistence in time series (Excel)

0:14:25

0:14:25

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlm

0:21:30

0:21:30

GARCH model - Eviews

0:02:11

0:02:11

11.4.2 Models of Volatility Clustering - GARCH

0:11:03

0:11:03

ARCH vs GARCH (The Background) #garch #arch #clustering #volatility #mgarch #tgarch #egarch #igarch

1:12:17

1:12:17

Volatility Modeling using GARCH Model

1:35:03

1:35:03

Lecture 6: Modelling Volatility and Economic Forecasting

0:10:08

0:10:08

Coding the GARCH Model : Time Series Talk

0:14:44

0:14:44

Volatility (FRM Part 1 2023 – Book 2 – Chapter 14)

0:08:13

0:08:13

(EViews10): Forecasting GARCH Volatility #forecast #garchforecasts #volatilityforecast

0:12:29

0:12:29

GARCH(1,1) in MS Excel

0:18:37

0:18:37

G#1 Introduction to ARCH/GARCH model

0:10:29

0:10:29

Time Series Talk : ARCH Model

0:09:27

0:09:27

Video 10 Estimating and interpreting a GARCH (1,1) model on Eviews

0:34:51

0:34:51

Garch Modelling in R

1:18:05

1:18:05

ARCH & GARCH Models | Arti Omar

Комментарии