filmov

tv

Volatility (FRM Part 1 2023 – Book 2 – Chapter 14)

Показать описание

*AnalystPrep is a GARP-Approved Exam Preparation Provider for FRM Exams*

After completing this reading you should be able to:

- Define and distinguish between volatility, variance rate, and implied volatility.

- Describe the power law.

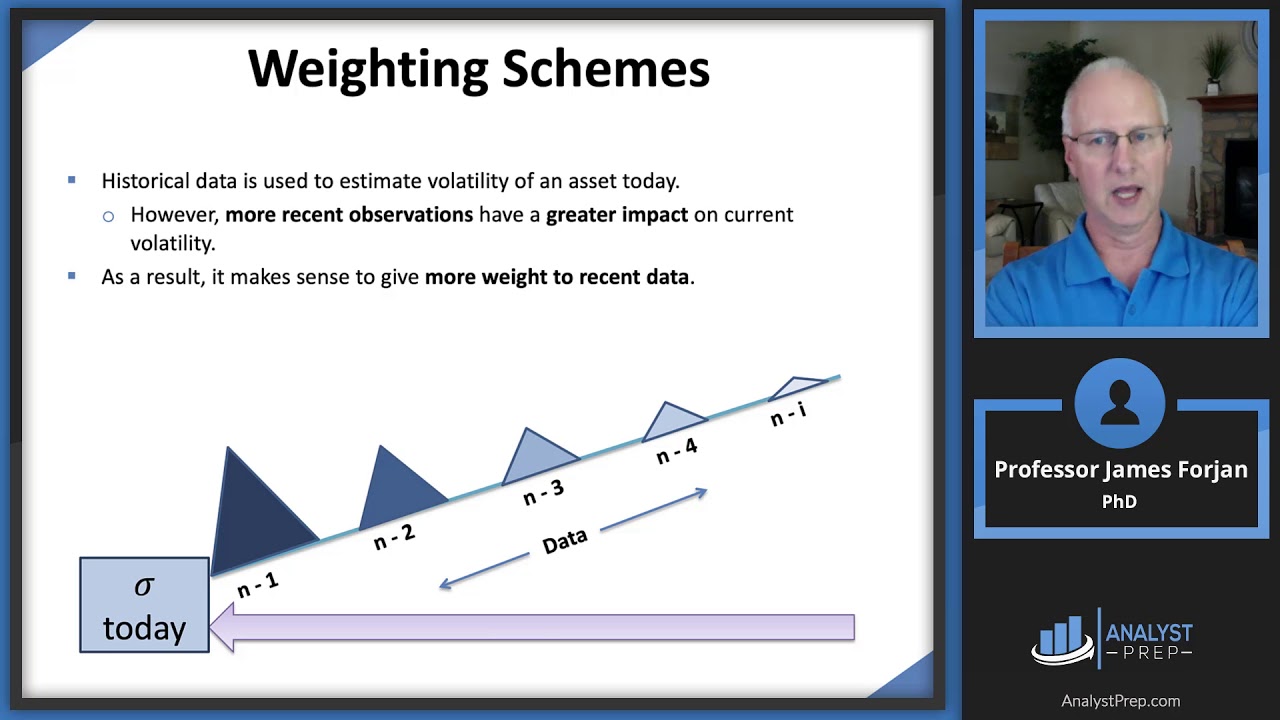

- Explain how various weighting schemes can be used in estimating volatility.

- Apply the exponentially weighted moving average (EWMA) model to estimate volatility.

- Describe the generalized autoregressive conditional heteroskedasticity (GARCH(p,q)) model for estimating volatility and its properties.

- Calculate volatility using the GARCH(1,1) model.

- Explain mean reversion and how it is captured in the GARCH(1,1) model.

- Explain the weights in the EWMA and GARCH(1,1) models.

- Explain how GARCH models perform in volatility forecasting.

- Describe the volatility term structure and the impact of volatility changes.

0:00 Introduction

0:46 Learning Objectives

1:16 What is Volatility?

4:35 The Power Law

7:46 Weighting Schemes

8:40 The Exponentially Weighted Moving Average (EWMA) Model

10:16 GARCH (1, 1) Model

12:43 Mean Reversion

13:21 Forecasting Performance

0:14:44

0:14:44

0:59:14

0:59:14

1:14:02

1:14:02

0:23:55

0:23:55

0:28:09

0:28:09

0:39:54

0:39:54

0:21:30

0:21:30

0:15:29

0:15:29

0:37:09

0:37:09

0:12:53

0:12:53

0:37:59

0:37:59

0:52:45

0:52:45

0:45:33

0:45:33

0:33:53

0:33:53

0:16:52

0:16:52

0:58:29

0:58:29

0:23:14

0:23:14

0:35:43

0:35:43

0:06:31

0:06:31

0:00:55

0:00:55

0:12:06

0:12:06

![FRM P1 [A]](https://i.ytimg.com/vi/6gZatTOfUfg/hqdefault.jpg) 0:39:45

0:39:45

0:48:53

0:48:53

1:21:26

1:21:26