filmov

tv

Genesis of GARCH - Why you have been measuring volatility wrong all your life

Показать описание

An introduction to GARCH, and why it can be a superior tool to sample standard deviation in measuring volatility.

Download the notebook in my GitHub page:

Download the notebook in my GitHub page:

Genesis of GARCH - Why you have been measuring volatility wrong all your life

What are ARCH & GARCH Models

Stock Forecasting with GARCH : Stock Trading Basics

Basics of GARCH Modeling #garch #garchmodeling #financialeconometrics #garch-m #tgarch #egarch

ARCH vs GARCH (The Background) #garch #arch #clustering #volatility #mgarch #tgarch #egarch #igarch

Jean-Michel Zakoïan: Testing the existence of moments for GARCH-type processes

GARCH A First (and Closer) Look (FRM Part 1, Book 4, Valuation and Risk Models)

MG#1 Introduction to multivariate GARCH model

(EViews10): Forecasting GARCH Volatility #forecast #garchforecasts #volatilityforecast

Coding the GARCH Model : Time Series Talk

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlm

(EViews10): How to Estimate GARCH-in-Mean Models #garchmodels #garchm #tgarch #volatility #egarch

(EViews10): ARCH vs. GARCH Models (Estimations) #garch #arch #parsimony #volatility

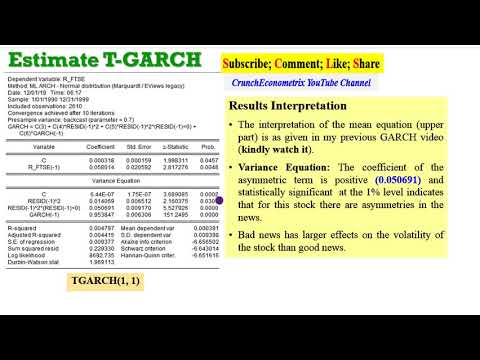

(EViews10): How to Estimate Threshold GARCH (GJR-GARCH) #garchm #tgarch #egarch #gjr-garch

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch #egarch #igarch #cgarch #arch

Unit Root, ARCH and GARCH | Time Series Analysis | Variance Forecasting

18. General Auto Regressive Conditional Heteroskedasticity (GARCH) Model || Dr. Dhaval Maheta

ECO 4051 - ARCH, GARCH, stylized facts about volatility, Risk measurement LEC

(EViews10): How to Perform GARCH Diagnostics #garch #diagnostics #garchdiagnostics #archdiagnostics

15. Generalized Auto Regressive Conditional Heteroskedasticity (GARCH) in R || Dr. Dhaval Maheta

Short Video Analyzing Islamic Stock index using ARCH GARCH method with EVIEWS 10

FINA 3322 EWMA and GARCH (1, 1) Volatility

Lecture 6: Modelling Volatility and Economic Forecasting

ARCH GARCH Video4

Комментарии