filmov

tv

Change of probability measure for Poisson process

Показать описание

Discusses the change of probability measure for the Poisson process, and related concepts such as Radon-Nikodym derivative, and change of drift.

0:26:34

0:26:34

Simplified: Girsanov Theorem for Brownian Motion (Change of Probability Measure)

0:27:25

0:27:25

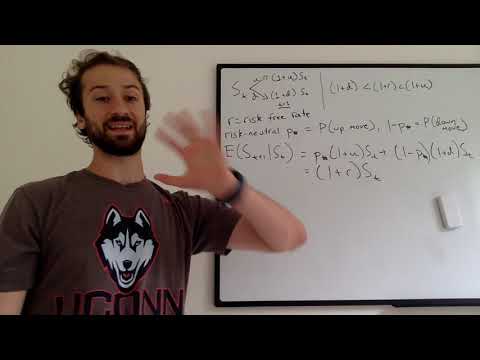

Simplified: Change of Probability Measure, and Risk Neutral Valuation

0:11:51

0:11:51

Probability Theory 14 | Expectation and Change-of-Variables

0:12:13

0:12:13

Change of probability measure for Poisson process

0:20:40

0:20:40

Change of Numeraire

0:15:40

0:15:40

3.1 change of measure, randon nikodym and state prices

0:09:03

0:09:03

Probability Change Of Variable: Theory (Part 1)

0:11:51

0:11:51

Probability Theory 14 | Expectation and Change-of-Variables [dark version]

1:07:08

1:07:08

Lec 25: General Probability Spaces, Expectations, Change of Measure

0:10:12

0:10:12

Risk neutral probability measure simplified

0:05:44

0:05:44

Measure change approach to the derivation of Black Scholes

0:00:57

0:00:57

Change of probability measure for Poisson process Quantpie

0:10:01

0:10:01

Why “probability of 0” does not mean “impossible” | Probabilities of probabilities, part 2

0:08:34

0:08:34

5. Risk Neutral Probability

0:10:07

0:10:07

Change of Variables & The Jacobian | Multi-variable Integration

0:00:35

0:00:35

How REAL Men Integrate Functions

0:03:01

0:03:01

Girsanov's Theorem for Dummies

0:07:29

0:07:29

Probability Density of a Function or Transform of a Random Variable: Change of random variables

0:30:27

0:30:27

Lecture 9 (Part 1): Change of measure for integrals

0:11:28

0:11:28

Math Antics - Basic Probability

0:12:24

0:12:24

Measure Theory 14 | Radon-Nikodym theorem and Lebesgue's decomposition theorem

0:27:21

0:27:21

Overview of Chapter 4 'Metrics on Probability Measures'

0:00:16

0:00:16

Probability Of Rolling Dice | How To Calculate Dice Probabilities #Shorts #NowWeKnow

0:16:42

0:16:42

10 11 Change of numeraire method Part 1

Комментарии