filmov

tv

Все публикации

0:20:40

Change of Numeraire

0:12:13

Change of probability measure for Poisson process

0:11:44

Ito's lemma for Poisson Process

0:10:42

Climate Modelling 3: General circulation of the atmosphere

0:12:55

Climate Modelling 2: The atmosphere and the radiation, a combination that makes the magic happen

0:09:14

Climate Modelling 1: Earth's energy budget and the Greenhouse gases' role in keeping us warm!

0:18:21

SABR Model - part 2B (Transformation of PDE)

0:08:13

Black Scholes Delta Simplified Derivation

0:06:23

the Shape of the Geometric Brownian Motion’s distribution

0:15:26

LIBOR Fallback = Adj RFR + Spread

0:16:56

SABR Model - part 2A (Valuation PDE)

0:33:58

SABR Model - part 1

0:14:54

Merton Jump Diffusion Model

0:35:34

Abstract Bayes' Formula and Conditional Expectation

0:25:40

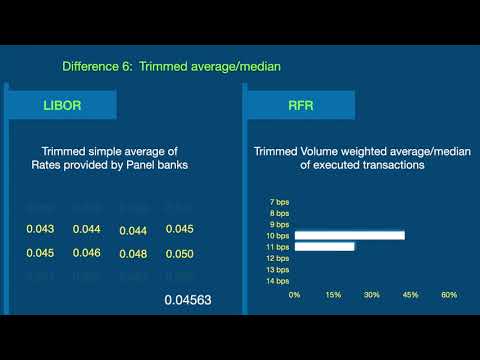

12 Differences between LIBOR and RFRs (alternative reference/risk free rates: SOFR, SONIA,€STR, …)

0:26:34

Simplified: Girsanov Theorem for Brownian Motion (Change of Probability Measure)

0:27:25

Simplified: Change of Probability Measure, and Risk Neutral Valuation

0:11:38

An illustration of Black Scholes’ Delta Hedging

0:04:54

Why is dW^2=dt?

0:05:08

Why is dt^2=0?

0:07:07

Why dWdt=0?

0:10:25

Chain Binomial Model for COVID-19 spread

0:07:39

Brownian motion - Physical intuition

0:30:47

Poisson: Marked, Compound, Compensated, ...

Вперёд

0:20:40

0:20:40

0:12:13

0:12:13

0:11:44

0:11:44

0:10:42

0:10:42

0:12:55

0:12:55

0:09:14

0:09:14

0:18:21

0:18:21

0:08:13

0:08:13

0:06:23

0:06:23

0:15:26

0:15:26

0:16:56

0:16:56

0:33:58

0:33:58

0:14:54

0:14:54

0:35:34

0:35:34

0:25:40

0:25:40

0:26:34

0:26:34

0:27:25

0:27:25

0:11:38

0:11:38

0:04:54

0:04:54

0:05:08

0:05:08

0:07:07

0:07:07

0:10:25

0:10:25

0:07:39

0:07:39

0:30:47

0:30:47