filmov

tv

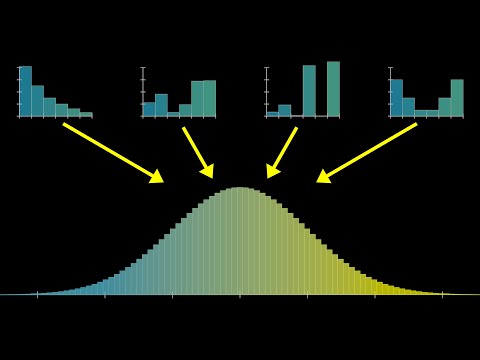

Why Sums And Averages Tend To Look Gaussian

Показать описание

We study the distribution of sums and averages of independent random variables. We show that for both discrete and continuous variables the distribution is obtained via convolution of the corresponding probability mass functions or probability density functions. These repeated convolutions smooth the pmfs and pds making them Gaussian-like, as we illustrate through two examples. In addition, we show that the convolution of two Gaussians is Gaussian (so sums of independent Gaussians are also Gaussian).

0:32:18

0:32:18

Why Sums And Averages Tend To Look Gaussian

0:37:40

0:37:40

11. Riemann Sums and Average Value

0:31:15

0:31:15

But what is the Central Limit Theorem?

0:01:47

0:01:47

The Standard Deviation (and Variance) Explained in One Minute: From Concept to Definition & Form...

0:00:14

0:00:14

NEWYES Calculator VS Casio calculator

0:13:09

0:13:09

How to use basic sums, average, count functions in LibreOffice Calc

0:10:57

0:10:57

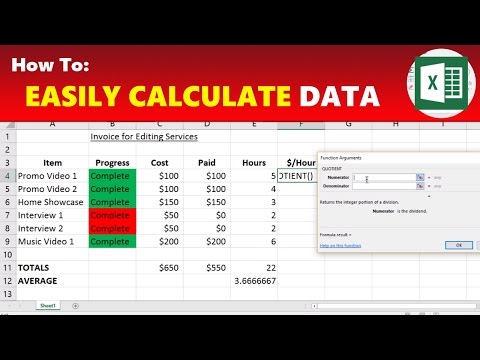

How To: Calculate Sums, Averages, Hourly Rates & Other Functions in Microsoft Excel

0:00:17

0:00:17

Arithmetic progression Formula #Maths #shorts #mathematics

0:07:50

0:07:50

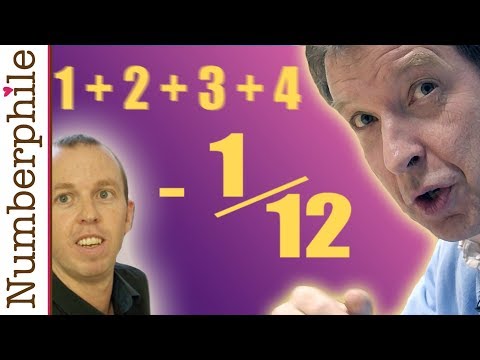

ASTOUNDING: 1 + 2 + 3 + 4 + 5 + ... = -1/12

0:08:15

0:08:15

SUM AND AVERAGES IN STATISTIC

0:10:25

0:10:25

Why the Strangest Sums in Math Are Actually Useful!

0:07:51

0:07:51

More on sums of independent random variables (Part 1)

0:11:10

0:11:10

One minus one plus one minus one - Numberphile

0:00:12

0:00:12

IIT Bombay Lecture Hall | IIT Bombay Motivation | #shorts #ytshorts #iit

0:29:16

0:29:16

Central Limit Theorem for Means and Sums

0:00:12

0:00:12

JEE Aspirants ka Sach 💔 #JEE #JEEMain #Shorts

0:00:47

0:00:47

😁 Playing 🐍Snake🐍 game on calculator 😜 [official video] #shorts #viral #casio

1:53:27

1:53:27

Statistical Mechanics Lecture 3

0:31:45

0:31:45

What is the Window function in Tableau? Part1 Tableau Functions

0:00:33

0:00:33

Can you find the 5th arrow? #shorts

0:12:39

0:12:39

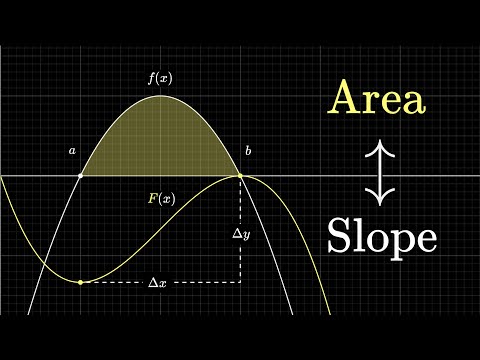

What does area have to do with slope? | Chapter 9, Essence of calculus

0:12:31

0:12:31

Warren Buffett: How to Invest Tiny Sums Of Money During Overvalued 2024 Market

0:04:14

0:04:14

CAT Preparation - Averages Question 3

0:40:29

0:40:29

What is the Ultraviolet Catastrophe?

Комментарии