filmov

tv

Goodwill explained

Показать описание

What is goodwill? How to calculate goodwill? We will discuss the definition of the finance and accounting term goodwill, and go through an example of goodwill by discussing one of the largest technology acquisitions in recent history: the acquisition of social network Linked In by Microsoft. We will review the calculation of goodwill for that headline-grabbing deal, which is a great example of how to record goodwill on the balance sheet.

⏱️TIMESTAMPS⏱️

0:00 Introduction to goodwill

0:37 Definition of goodwill

2:09 Goodwill example

3:12 Accounting for goodwill

5:13 Purchase price allocation

6:10 Goodwill and intangible assets

7:47 Goodwill impairment test

For some companies, goodwill is in the top 3 of largest categories of assets on their balance sheet. If you want to make sense of a company’s financial statements, then a basic understanding of the concept of goodwill is invaluable.

Goodwill is the excess of the purchase price paid for an acquired firm, over the fair value of its separately identifiable net assets.

A definition of goodwill in simpler terms: goodwill is the difference between what a company pays to buy an acquisition target, and what that acquired company is worth “on paper”.

Goodwill is recognized only in a business combination, and goodwill is not amortized.

Why would any acquiring company pay a premium for an acquisition target above what that company’s net assets are worth? Goodwill reflects the perceived superior earnings capacity of the business combination.

Companies have to perform an annual impairment test to both goodwill and intangible assets. What that impairment test does is basically to assess whether the carrying value of goodwill and intangible assets is recoverable. In simple terms: if the financial results and future prospects of the business you acquired are dramatically dropping, you need to write off all or part of the goodwill and intangible assets.

Philip de Vroe (The Finance Storyteller) aims to make strategy, finance and leadership enjoyable and easier to understand. Learn the business vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better stock market investment decisions. Philip delivers training in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

⏱️TIMESTAMPS⏱️

0:00 Introduction to goodwill

0:37 Definition of goodwill

2:09 Goodwill example

3:12 Accounting for goodwill

5:13 Purchase price allocation

6:10 Goodwill and intangible assets

7:47 Goodwill impairment test

For some companies, goodwill is in the top 3 of largest categories of assets on their balance sheet. If you want to make sense of a company’s financial statements, then a basic understanding of the concept of goodwill is invaluable.

Goodwill is the excess of the purchase price paid for an acquired firm, over the fair value of its separately identifiable net assets.

A definition of goodwill in simpler terms: goodwill is the difference between what a company pays to buy an acquisition target, and what that acquired company is worth “on paper”.

Goodwill is recognized only in a business combination, and goodwill is not amortized.

Why would any acquiring company pay a premium for an acquisition target above what that company’s net assets are worth? Goodwill reflects the perceived superior earnings capacity of the business combination.

Companies have to perform an annual impairment test to both goodwill and intangible assets. What that impairment test does is basically to assess whether the carrying value of goodwill and intangible assets is recoverable. In simple terms: if the financial results and future prospects of the business you acquired are dramatically dropping, you need to write off all or part of the goodwill and intangible assets.

Philip de Vroe (The Finance Storyteller) aims to make strategy, finance and leadership enjoyable and easier to understand. Learn the business vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better stock market investment decisions. Philip delivers training in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

0:09:11

0:09:11

Goodwill explained

0:06:24

0:06:24

What is Goodwill? | Understanding Intangible Assets

0:00:58

0:00:58

Goodwill Explained Simply

0:00:20

0:00:20

Goodwill Formula Explained #financialeducation #investing #stockmarket #stocks #investment #invest

0:04:52

0:04:52

What is Goodwill - Goodwill Accounting in Investments

0:02:31

0:02:31

what is Goodwill in Accounting? How It Works, How To Calculate, Accounting Goodwill Explained.

0:11:26

0:11:26

The TRUTH About Chain Thrift Stores

2:59:23

2:59:23

Final Paper 1: FR | Topic: Ind AS 110: Consolidated Financial Statements | Session 1 | 14 Jan, 2025

0:04:11

0:04:11

Full Goodwill Method | What Is Goodwill | Goodwill Explained BY Amir Shakoor

0:08:49

0:08:49

Goodwill explained

0:00:54

0:00:54

Goodwill in Accounting Explained: Simplifying Intangible Assets

0:00:56

0:00:56

Goodwill Meaning #Goodwill #tally #shorts #rulesofdebitandcredit #journalentry #account

0:03:13

0:03:13

Goodwill (Balance Sheet) | Finance and Accounting for Beginners

0:00:59

0:00:59

What is Goodwill? | Types of Goodwill |Goodwill kya hai? |Letstute Accountancy Hindi#shorts#ytshorts

0:02:00

0:02:00

Impairment: Goodwill

0:06:28

0:06:28

Goodwill and Business Value

0:01:03

0:01:03

GOODWILL MEANING VERY SIMPLE

0:02:31

0:02:31

Goodwill ki amount ko Premium for Goodwill kyu Kehte hai | Explained by Neeraj Sir

0:14:50

0:14:50

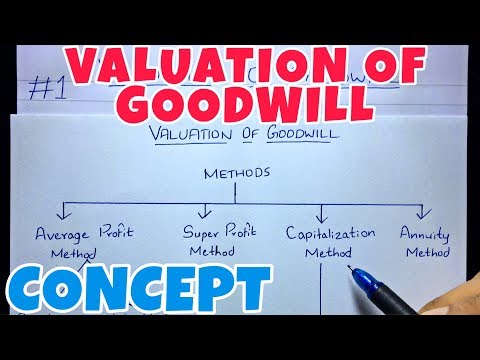

#1 Valuation of Goodwill - Concept -Corporate Accounting -By Saheb Academy ~ B.COM / BBA / CMA

0:07:17

0:07:17

Explained: How Do I Value Goodwill?

0:00:54

0:00:54

Goodwill in Accounting Explained: Simplifying Intangible Assets

0:06:50

0:06:50

Goodwill Shopping Secrets They Don't What * YOU * To Know !

0:04:33

0:04:33

Goodwill Explained - AMC

0:04:30

0:04:30

Goodwill - Business Combinations (CPA Financial Reporting)

Комментарии