filmov

tv

Fixed Indexed Annuities Explained

Показать описание

Are you thinking of getting a fixed annuity? Watch this video first! You'll get fixed indexed annuities explained in an easily understandable way, so you know exactly what you're getting into!

Watch and Enjoy!

Stan The Annuity Man

Request Free Owner’s Manual Here

========================

Key Moments in this Episode

========================

00:00 Intro & Summary

00:41 What Is A Fixed Indexed Annuity

01:56 What Are The Upsides & Downsides Of Fixed Indexed Annuities

04:33 What Is The Differences Of Fixed Index Annuities And Fixed Annuities

05:24 Is Fixed Index Annuity An Insurance Or A Contract

08:24 Book A Call!

What To Watch Next:

========================

How To Get Out Of A Fixed Annuity

Other Resources

========================

Visit Stan The Annuity Man’s website

Learn more about Stan The Annuity Man

Get your annuity quote here

========================

Video by Nate Woodbury

#StanTheAnnuityMan

#Annuity

#TheAnnuityMan

Watch and Enjoy!

Stan The Annuity Man

Request Free Owner’s Manual Here

========================

Key Moments in this Episode

========================

00:00 Intro & Summary

00:41 What Is A Fixed Indexed Annuity

01:56 What Are The Upsides & Downsides Of Fixed Indexed Annuities

04:33 What Is The Differences Of Fixed Index Annuities And Fixed Annuities

05:24 Is Fixed Index Annuity An Insurance Or A Contract

08:24 Book A Call!

What To Watch Next:

========================

How To Get Out Of A Fixed Annuity

Other Resources

========================

Visit Stan The Annuity Man’s website

Learn more about Stan The Annuity Man

Get your annuity quote here

========================

Video by Nate Woodbury

#StanTheAnnuityMan

#Annuity

#TheAnnuityMan

0:08:45

0:08:45

Fixed Indexed Annuities Explained

0:02:24

0:02:24

Basics of Fixed Indexed Annuities

0:03:35

0:03:35

Dave, Can You Clarify What A Fixed Index Annuity Is?

0:02:47

0:02:47

Indexed Annuities - EXPLAINED!

0:09:35

0:09:35

What Is An Index Annuity And How Does It Work?

0:02:00

0:02:00

What Is a Fixed Indexed Annuity (FIA)?

0:22:39

0:22:39

Index Annuities Explained

0:19:17

0:19:17

Fixed Indexed Annuity ***MUST SEE*** Fixed Index Annuity Explained

0:21:05

0:21:05

Equity Indexed Annuities Explained

0:10:12

0:10:12

Fixed Indexed Annuity: Index Crediting Options Explained

0:02:26

0:02:26

Understanding Fixed Index Annuities – How Does a Fixed Index Annuity Work?

0:04:08

0:04:08

What is a Fixed Index Annuity?

0:04:32

0:04:32

How Fixed Index Annuities Work - How Do Fixed Indexed Annuities Work?

0:03:21

0:03:21

Get the Basics on Indexed Annuities

0:25:31

0:25:31

5 PROS & CONS of a Fixed Indexed Annuity

0:04:45

0:04:45

Is It Time to Reconsider Fixed Indexed Annuities?

0:05:01

0:05:01

Learn The Basics: Fixed Index Annuities

0:05:54

0:05:54

What Is An Annuity And How Does It Work?

0:18:36

0:18:36

Annuities Explained & Is There A Better Option?

0:25:47

0:25:47

What is an Indexed Annuity?

0:33:32

0:33:32

Fixed Indexed Annuities Explained | Record-Breaking Growth in 2023

0:12:50

0:12:50

Why You May Consider Purchasing an Indexed Annuity Right Now with Aaron Andrew

1:30:34

1:30:34

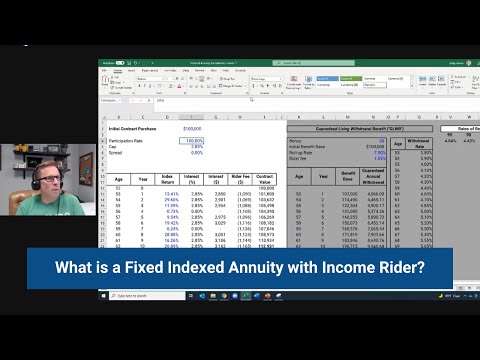

What is a Fixed Indexed Annuity with Income Rider?

0:14:30

0:14:30

Best Fixed Indexed Annuities (FIAs) For Retirement

Комментарии